Orchestration Economics: The AGNT Archetype (Chapter 11)

When intent, context and workflow control converge, they create a new structural role: the orchestrator. This is the primary locus of value creation and capture in the Agentic Era.

This is the latest excerpt from AGNT: The Orchestration Economics Manifesto - An Investment Framework for the Agentic Era. Each Thursday, I explore a major theme of the Manifesto and unpack the frameworks, adding extra context with more recent developments. Note: The figures and sequential references are taken directly from the larger Manifesto.

The Three Laws describe the conditions under which a company can become the orchestrator and sustain a durable advantage in the Agentic Era. But markets do not price conditions in the abstract. They price the structural positions that those conditions give rise to. When proximity to intent, depth of context, and control over workflow converge within the same domain, they do not remain as separate attributes. They collapse into a single, identifiable role in the system that transforms human intent into executed outcomes. That role is not captured by any existing category. It is not a product definition, a sector classification, or a stage in the software stack as previously understood. It is a position that emerges from the architecture itself.

The purpose of this chapter is to describe the position and define it clearly. Because once it is visible, it can be systematically identified across the market, compared across industries, and evaluated as the primary locus of value creation and capture in the new regime.

The Species

What emerges from that shared position is best understood not as a sector but as a species: a class of firms defined by their structural role in the orchestration of work.

A company that captures intent at the point of origin, that owns the deepest and most operationally relevant context, and that directs the workflows required to convert both into outcomes occupies a position that is categorically different from one that performs only a subset of those functions.

This manifesto calls that position AGNT.

AGNT is not a stock ticker. It is a structural archetype that can be identified, scored, and compared across industries. It cuts through traditional boundaries because those boundaries were built for a different regime, one where software was a tool, and operations were separate from it. The market’s sorting mechanisms via sector-based indices, thematic baskets, and the Rule of 40 were calibrated for a regime in which software competed for IT budgets and physical businesses competed on operational efficiency. GICS codes describe where a company was. The Three Laws of Agentic Value describe where a company is going.

An enterprise CRM platform can be an AGNT. It captures intent because 150,000 companies set sales goals in it every day. It provides context through decades of customer interaction data, pipeline patterns, and conversion histories across millions of accounts. It compounds workflow intelligence with every sales cycle it orchestrates. Apply the Three Laws. The position is defensible.

A global insurance carrier can be an AGNT. It captures intent because the policyholder is its customer. It holds context in the form of actuarial loss data built over decades of underwriting real risk with real capital. No foundation model can synthesize this from training data. It was generated by operations that bear real-world consequences.

In the Agentic Era, that separation collapses. A freight carrier and an enterprise software platform may have more in common architecturally than either has with the company next to it in a sector index. The entity that receives intent, deploys intelligence, and coordinates execution becomes the locus of control, regardless of whether it is labeled as a software company, a financial institution, or an industrial operator.

The implication is that similarity is no longer determined by sector adjacency, but by architectural equivalence. Two companies in different industries may occupy the same structural position, while two companies in the same industry may be separated by it entirely.

The Three Laws provide the mechanism for making that distinction explicit. Apply them, and the species reveals itself.

The question is not what this company sells. The question is where this company fits within the “Orchestration Graph” we define below.

Four Combatants

The first combatant: the AI laboratories ascending the stack.

OpenAI and Anthropic did not begin as orchestrators. They began as model providers selling intelligence at the bottom of the stack. But they understand that the model layer alone cannot capture the value implied by their valuations. Model price-performance is compressing, even as access to the most capable frontier intelligence remains scarce and increasingly subject to strategic control.

So the laboratories are building upward. OpenAI has expanded from Frontier into workspace agents, ChatGPT Work, and a dedicated deployment company designed to embed its systems directly into enterprise operations. Anthropic has moved from Claude Code and Cowork into vertical agent packages.

The entry strategy is what we call the “coding wedge”, documented in software engineering, now understood as a deliberate go-to-market: win developers first, then use the trust, habits, and organizational adoption built inside engineering teams to expand outward into the rest of the enterprise.

Three traditional software defenses are breaking under pressure. Integration moats erode when agents route dynamically across any system with a protocol connection. UI moats erode when the primary user is an agent executing via APIs, rather than a human navigating an interface. Capability moats erode when foundation models compose specialized functions on the fly.

The labs’ advantage is technological fluency and speed of iteration. Their vulnerability is the Second Law. They possess intelligence without institutional knowledge. They have no claims data, no routing history, no actuarial tables, no supply chain memory. They are climbing toward the Orchestration Layer from below, and every rung they reach is contested by incumbents who have occupied it for decades. The race is intelligence ascending against context defending. Chapter 13 traces this in detail.

The second combatant: the software incumbents pivoting from storage to action.

Salesforce, ServiceNow, Workday, SAP, and Oracle hold the canonical data that enterprises operate on. Ripping them out requires migrating decades of operational records, retraining thousands of users, rebuilding integrations with dozens of downstream systems, and accepting the risk of operational disruption in mission-critical processes.

Their position is not in question. Their role is.

In the pre-agentic world, the system of record was also the system of action. When a sales rep wanted to update a deal, she opened Salesforce. The application was the interface where intent met execution. In the agentic world, intent starts in a conversation. A user tells an agent: “Update the pipeline forecast for Q2”. The agent calls the CRM’s API, reads the data, performs the analysis, and reports back without the user ever opening the application. The system of record is still essential. But it risks demotion from the system where work is directed to the system where data is stored. The database behind the orchestrator rather than the orchestrator itself.

The central strategic challenge for every enterprise software incumbent is to make the transition from system of record to system of action, the platform that receives intent, deploys agents, and coordinates workflows end to end. Salesforce is attempting it with Agentforce and the repositioning of Slack as the enterprise’s intent surface. ServiceNow is building agentic IT service management. Those who succeed become orchestrators. Those that do not will retain data gravity but lose control of the workflow and the pricing power that accompanies it.

Their advantage is context gravity. This is the irreplaceable institutional data that already lives inside their platforms. Their vulnerability is speed. The AI labs are building toward the same position from the opposite direction, and the orchestration position compounds with every interaction. The window narrows with each quarter. Chapter 14 traces the sorting.

The third combatant: the throughput node.

Not every software company must become the captain. Some of the most durable positions in the agentic economy will belong to companies that never aspire to the apex of the orchestration graph, but whose context is so dense that every orchestrator must route through them.

A throughput node does not capture intent. It does not control the workflow. It holds the context that makes the workflow correct. When that context is sufficiently deep and semantically rich, the orchestrator cannot complete the work without passing through the node. It doesn’t matter who occupies the captain’s seat. These are the tools that step into the orchestration loop rather than waiting on the sidelines. They expose their context through open protocols, becoming surfaces through which agents move work rather than destinations where humans perform it. A tool that remains a destination risks being bypassed. A tool that becomes a node becomes structural.

The distinction between a throughput node and a convenience layer is semantic density across the production chain. A design platform whose component libraries, interaction models, and brand systems are inputs to every downstream workflow in product development is a throughput node. A project management tool whose task metadata can be replicated by the orchestrator’s own coordination logic is a convenience layer. The Second Law identifies the difference. The market has not yet learned to price it. Chapter 15 traces the distinction.

The fourth combatant: the domain operators building from the inside.

Insurance carriers, banks, logistics companies, manufacturers, and healthcare systems are the companies that own the physical assets, regulatory relationships, and operational context that most deeply satisfy the Second Law.

These companies never considered themselves technology companies. They are becoming orchestrators by necessity, because the agentic transition presents a binary choice: build your own Orchestration Layer or watch someone else build it on top of your operations and capture the margin.

A global logistics carrier deploying a master agent to coordinate fleet routing, capacity allocation, customs clearance, and last-mile delivery is not buying orchestration from a software vendor. It is building orchestration atop its own operational context, using foundation models as reasoning engines.

The carrier’s competitive advantage was always its physical network and accumulated operational knowledge. In the pre-Agentic Era, that advantage was constrained by the throughput of human managers. In the Agentic Era, the same advantage is unleashed via agents coordinated to operate at machine speed across the full scope of operations.

The same logic applies across every Capex-heavy, operationally complex industry:

A construction equipment manufacturer whose agents coordinate fleet scheduling, predictive maintenance, and supply chain management across dozens of job sites.

An insurer whose agents process claims through orchestrated workflows built on decades of actuarial data.

A bank whose agents orchestrate credit analysis, risk assessment, and portfolio management across a multi-trillion-dollar balance sheet.

In each case, the physical assets and operational history provide the context. The foundation models provide the cognition. The Orchestration Layer is built by the enterprise rather than purchased from a vendor because that is where the value concentrates. Their advantage is the irreplaceable context generated by decades of operations.

Their vulnerability is that they must build the fastest from the furthest starting point. These companies are not accustomed to building software platforms. They must learn or partner at a pace that their organizational cultures have never demanded. The risk for all four combatants is identical: time. The orchestration position compounds. Early movers accumulate coordination intelligence that later entrants must rebuild from scratch. However, the Third Law is the weakest of the three conditions: pure workflow choreography is increasingly learnable by capable agents. What compounds durably is a workflow that embeds irreplaceable operational context. This is the Second Law, expressed through coordination. In domains where all three laws hold, where a company captures intent, owns deep context, and controls decomposable, multi-step workflows, the gap may become structurally unclosable.

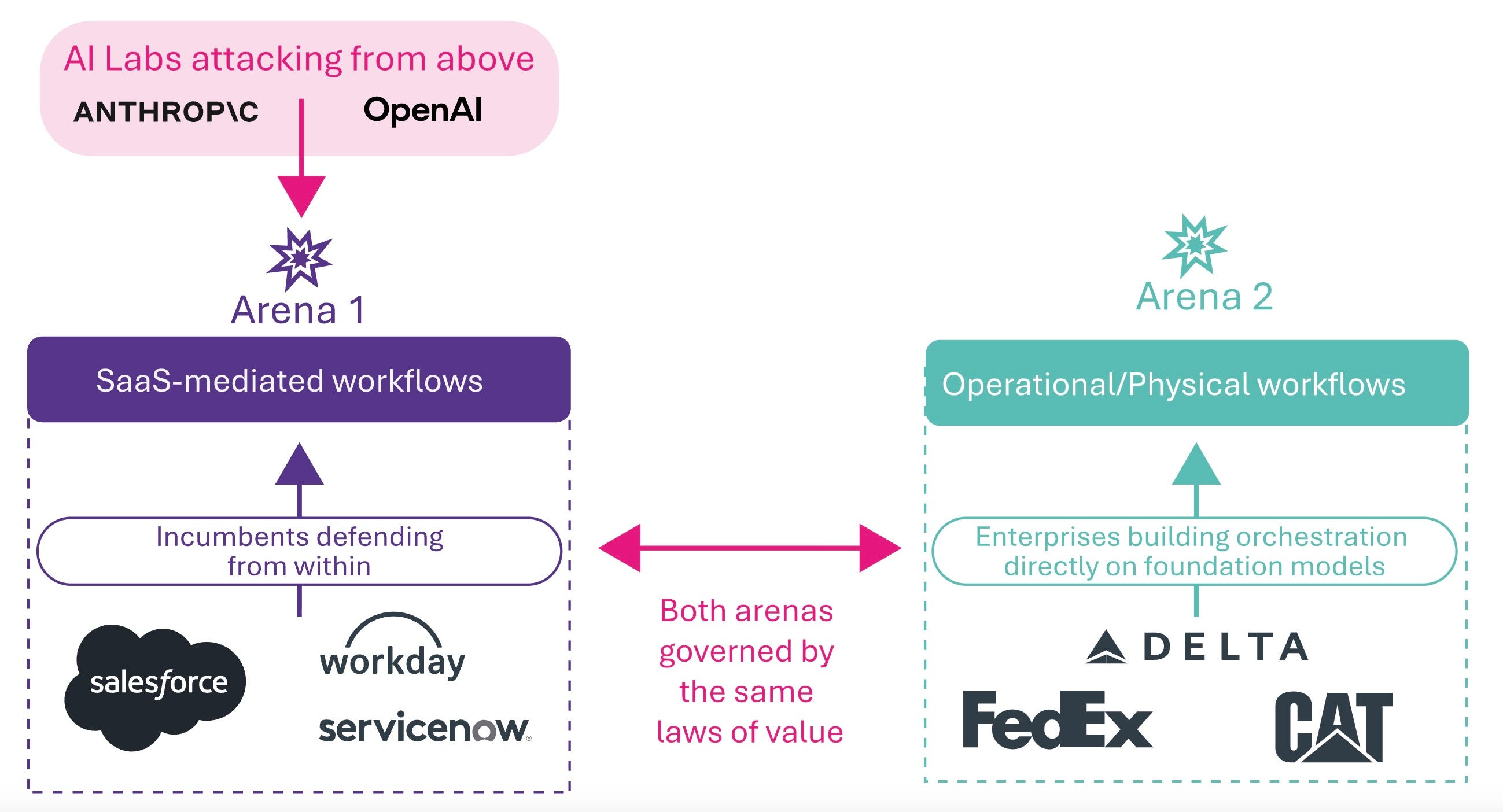

The Two Arenas

There may be three combatants. But they are not all confronting each other directly. Instead, there are two competitive battlefronts.

Arena One encompasses workflows that already run through enterprise software platforms: CRM in Salesforce, IT service management in ServiceNow, human capital management in Workday, ERP in SAP, design in Figma, storage in Box, etc. These are the digitized, process-heavy workflows that defined the SaaS era.

In Arena One, three outcomes emerge for the companies inside it. Some will be displaced entirely. For instance, the capability providers that monetized a single function that agents can now compose from general-purpose intelligence. Some will be absorbed into the execution layer, surviving as API endpoints invoked by orchestrators, retaining revenue but losing pricing power and strategic control. Some will become orchestrators themselves, leveraging existing customer relationships, context gravity, and institutional trust to claim the captain’s chair while partnering with AI labs for the intelligence they direct.

The sorting in Arena One plays out between AI labs attacking from above, software incumbents defending from within, and throughput nodes anchoring themselves as mandatory bridges that every orchestrator must cross.

Arena Two encompasses workflows that were never fully digitized. These are the operational, physical-world processes where human cognition coordinates physical assets: supply chains, manufacturing lines, logistics networks, construction projects, and clinical operations.

These workflows generated vast operational data but were never mediated by a software platform, unlike CRM, which mediated sales. The coordination lived in managers’ heads, in phone calls, in spreadsheets, and in tribal knowledge.

In Arena Two, the battle is to see which enterprises become orchestrators and build their own Orchestration Layers before third parties do. The LLM is the engine, not the captain.

The intermediary reckoning plays out almost entirely in Arena Two. This is the structural inversion where physical asset owners ascend as cognitive middlemen fall. The freight broker that owned no trucks, the insurance broker that sat between carrier and client, and the wealth advisor whose value was synthesizing information that an agent can now synthesize faster.

Each occupied a position between the asset owner and the customer, monetizing cognitive labor that is now being automated. When agents close that gap, the value will not automatically transfer to the AI lab or to the software platform. It could also be captured by the asset owner if they leverage the operational context by creating an effective Orchestration Layer.

Both arenas tap the labor market. They do so for different reasons.

In Arena One, the expansion is a budget migration. Software companies that cross the reliability threshold stop selling seats from the IT budget and start selling outcomes from the labor budget. The workflows already exist in digital form. The TAM expands because the buyer is no longer comparing $150/seat/month against a competing SaaS vendor. They are comparing the cost of the orchestrated outcome against the fully loaded cost of the knowledge worker the outcome replaces. The same workflows, repriced against a surface five to ten times larger.

In Arena Two, the expansion is a digitization event. These workflows were never mediated by software at all. The coordination lived in managers’ heads, in phone calls, in spreadsheets. There is no existing IT spend to displace, only labor spend that was never addressable by technology until agents crossed the capability threshold. The TAM does not expand from a smaller budget to a larger one. It materializes for the first time.

Arena One reprices existing digital workflows against the labor market. Arena Two brings non-digital workflows into the orchestrated economy for the first time. Both are measured in trillions. Arena Two is potentially the larger opportunity because it starts from a base of zero digital penetration.

The entire value pool is greenfield.

This is why the agentic transition is not a story about software eating itself. It is a story about who captures the value when intelligence becomes abundant enough to coordinate both digital and physical operations at machine speed.

The Map

The remaining chapters of Part IV trace the sorting across each combatant and each arena.

Chapter 12 examines what the AI labs are building: not better models, but orchestration platforms competing for the enterprise control plane.

Chapter 13 traces the software reckoning: the sorting of enterprise incumbents into systems of action, throughput nodes, and casualties. The SaaSpocalypse was directionally correct and analytically lazy. The Three Laws identify which companies the market is punishing unfairly and which it is not punishing enough.

Chapter 14 examines how software tools defend: the throughput node strategy and the new network effects that emerge when agent density replaces user density as the driver of platform value.

Chapter 15 follows the leviathans: the physical-economy companies whose operational context, accumulated over decades, positions them as the most structurally advantaged orchestrators in the framework. The intermediary reckoning. The physical-asset inversion. The largest value migration that nobody is watching.

The views and opinions expressed in this publication are those of the author alone and are based on publicly available information. The expressed views and opinions do not constitute investment advice, a solicitation, or a recommendation to buy or sell any security or financial instrument. The author may hold positions in the securities of companies mentioned. Certain companies referenced may be current or former clients of, or counterparties to, the author or affiliated entities; such relationships will be disclosed where applicable. Past performance is not indicative of future results. To the fullest extent permitted by applicable law, the author does not accept any liability for any loss or damage arising from reliance on this content. Readers should conduct their own independent due diligence and consult a qualified financial advisor before making any investment decision.