‘Madman Karp’: Palantir CEO's Case Against OpenAI and Anthropic Is Only Half Right

Palantir's Nvidia deal exposes a deeper battle over enterprise AI. Alex Karp correctly diagnoses the problem, but mistakes where the next durable software moat will be built.

{kind=link}

TLDR: On July 1, CEO Alex Karp went on CNBC to discuss Palantir’s expanded Nvidia partnership and delivered a nineteen-minute broadside against OpenAI and Anthropic: enterprises are “livid” because they are paying for “tokens that create no value” while the labs harvest their data and alpha. Karp is right that enterprises are frustrated with exploding token costs and frontier labs capturing too much value/control. But he is wrong that Palantir’s platform (Ontology + Nemotron) is the necessary cure that makes agents “safe, useful, and precise”. Those properties come from the specification and verification core, which Palantir has a strong version of, but does not own. Open weights are not the frontier. The labs are already moving inside customer perimeters. Therefore, Palantir is half right on the diagnosis but overclaims on the prescription.

Something remarkable happened on CNBC’s Squawk Box last week. Palantir CEO Alex Karp was ostensibly there to discuss Palantir’s expanded deal with Nvidia in “Sovereign Environments,” but instead spent most of his airtime attacking the companies whose products his own platform resells.

Karp delivered what we can call a televised monologue against the frontier labs. Enterprises, he said, are “livid” because they are paying for “tokens that create no value” while the labs cache their data, absorb their alpha, and levy what he called a “wealth tax” on American business. The arrangement extended to national security is “effing insane.“ When Squawk Box co-host Becky Quick observed that he sounded pretty angry, Karp answered that he was merely channeling the voice of American business and dared them to privately call CEOs and tell them, “Madman Karp is on TV saying we’re livid,” to see if they would admit they are.

Despite the theatrics, Karp’s CNBC broadside against OpenAI and Anthropic resonated because it tapped into a genuine anxiety spreading through enterprise AI. Companies are watching their token bills explode, questioning whether foundation model providers are capturing all the value and their data along the way, and wondering who will ultimately control the enterprise AI stack.

It also somewhat overshadowed Palantir’s news. The Nvidia deal deserves attention because it addresses a structural peculiarity. Palantir was one of the earliest players to make a bid to seize the orchestration layer, the most valuable terrain in Orchestration Economics. And yet, it was attempting to do so without owning the model layer. [More on this later this week, when I revisit the evaluation of Palantir against my Three Laws of Agentic Value, which I published earlier this year in the Manifesto.]

Palantir expanded its partnership with Nvidia to deploy Nvidia’s open-weight Nemotron AI models on sovereign, air-gapped Blackwell infrastructure, enabling government agencies and critical infrastructure operators to run AI entirely within secure, self-controlled environments. The deal gives Palantir its first integrated model offering, allowing it to move beyond simply brokering third-party models. It strengthens the company’s pitch that customers can deploy a complete AI stack without relying solely on frontier model providers.

While Karp’s diagnosis of soaring token costs and growing distrust of frontier labs is largely correct, his proposed solution points to the wrong destination.

He argues that enterprises need companies like Palantir to make large language models “safe, useful, and precise.” In fact, the application layer itself is rapidly being unbundled. What remains defensible is the specification-and-verification core within it: the machine-readable definition of how an organization works, what its objectives are, which constraints matter, and how an AI agent knows when it has completed a task correctly. That layer is becoming the scarce asset as agents commoditize much of traditional enterprise software.

Palantir possesses one of the strongest examples of it in its Ontology, but it does not own the category. Frontier labs, data platforms, and enterprises themselves are all converging on the same ground while simultaneously redrawing the boundary between models and applications.

So, Palantir’s enthusiastic evangelism for open weights, sovereignty, and the demonization of the Big Model labs is both opportunistic and a strategic necessity. Despite otherwise strong earnings, the company’s stock is down about a quarter this year and, at its late-June trough, was down almost half from its November 2025 peak. And yet, Palantir’s market capitalization prices it at about 40 times forward sales, about double the multiple at which Anthropic recently raised its Series H at a $965bn valuation, suggesting there’s a strong case that it remains overpriced.

Given Palantir's obvious self-interest in making this case, I want to evaluate Karp’s diagnosis as well as his broader prescription. But I also want to zoom back to understand the implications for Palantir, which remains one of the more intriguing case studies for decoding the way value is migrating in the Agentic Era.

The bill is real - and it is the wrong number

Karp is right about enterprise AI bills exploding. We can say with confidence that this is not an AI hallucination. The nervous whispers about the mounting costs burst into public in mid-May, when Uber’s CTO revealed the company had burned through its annual AI coding-tools budget in just four months. Days later, reports emerged that Microsoft had begun canceling internal Claude Code licenses as spending soared. Chief financial officers who budgeted for chatbot-era token consumption had discovered that agentic deployment was exponential rather than incremental.

The reason is architectural. A chatbot answers a question in one round trip. An agent decomposes a task and then plans, calls tools, reads files, retries, verifies, and iterates. Along the way, it consumes one to two orders of magnitude more tokens per task. When an engineering organization moves from autocomplete to delegated multi-hour coding runs, its token consumption grows in proportion to the ambition of what it delegates.

The bills Karp’s livid CEOs are staring at are the direct signatures of agents actually doing work. But while their fury may be understandable, it is also misplaced.

By focusing on absolute spend, companies are aiming at a vanity metric that turns out to be the wrong one. What really matters is the cost per completed outcome.

This is governed by three factors:

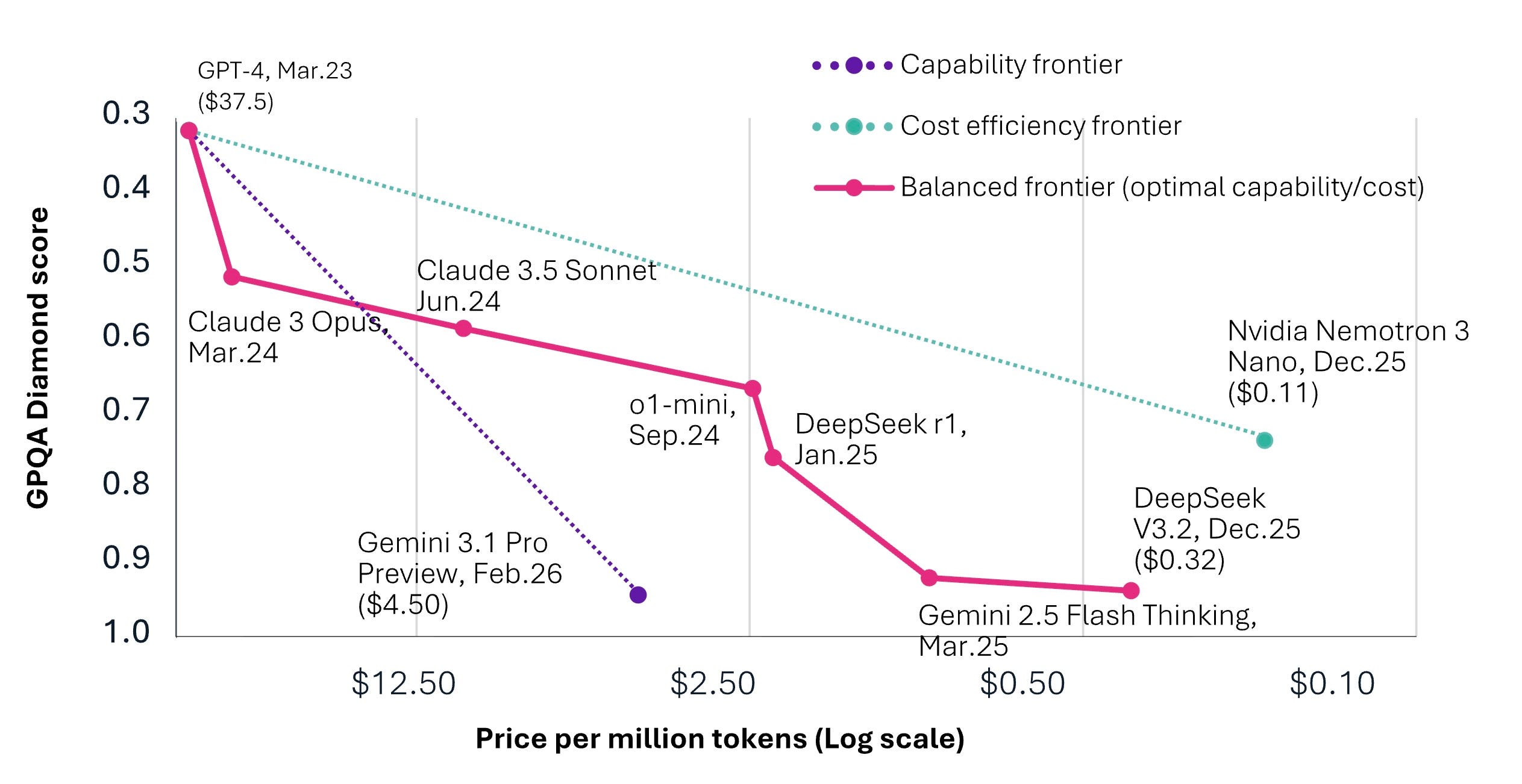

First, the price of any fixed level of capability continues to collapse. Epoch’s data puts the decline at between 9x and 900x per year, depending on the benchmark, with a median of roughly 50x. This non-linear marginal collapse in the cost of cognition is a key pillar of Orchestration Economics that has enabled the Agentic Era.

Second, capability per token continues to rise. Each generation completes more of the task per unit consumed.

Third, practitioners continue to confirm what deployment data increasingly shows: for the highest-value work agents perform, inference costs are negligible relative to the human expertise they augment. This was a central finding of the December 2025 Measuring Agents in Production study, one of the few rigorous analyses of production systems. Teams overwhelmingly default to the best closed models, regardless of inference cost, because the economics are driven not by token prices but by the value of the expert time those tokens replace.

This is why Karp’s high-level diagnosis needs to be much more precise: enterprises that adopted consumption pricing without outcome accounting are being severely hurt. Embracing “tokenmaxxing” consumption as a proxy for productivity deserves his mockery. But the correct response to an unmetered outcome problem is outcome metering: specifying what a completed task is worth and measuring cost against it. It is not, as Karp would have it, the repatriation of the means of production.

Rising token bills are the sound of deployment. The missing discipline is not sovereignty. It is verification. And that brings us to his central claim.

“Safe and useful and precise”: the right adjectives, the wrong claim

The intellectual core of the interview was this: LLMs are a critical resource, but raw. Enterprises need an application layer to fully refine and tame this wild material. As it happens, Karp said that Palantir’s Ontology platform “makes it safe and useful and precise.” Safe because it prevents the model from caching your data and replicating your business. Useful and precise because it grounds the model in your entities and operations.

Once again, Karp is taking a genuine framing around the three properties enterprise agents lack out of the box and muddling the picture by attaching them to his product.

Let’s examine the claim by taking it apart, adjective by adjective.

Safe: Karp’s own definition is revealing. AI is safe because the model does not cache your data, cannot replicate your business, and does not transfer your IP. Each of these is a claim about where data goes and what the provider may do with it. None of them is something an application platform does.

Whether a model retains prompts is set by contract. Enterprise agreements with the labs exclude training on customer data by default, and zero-data-retention addenda, available on approval, eliminate storage entirely. Whether data leaves the controlled perimeter is set by deployment architecture. Claude, through Bedrock or Vertex, runs inside the customer’s own cloud account and region, reached via private VPC endpoints, with zero public egress and the hyperscaler rather than the lab as the data processor, at FedRAMP High and IL5. Whether an agent can exfiltrate anything is set by network controls, egress policies, and audit logging.

A residual remains where the labs do not go alone: frontier weights are not available on-premises, and Claude’s landmark deployment on classified networks ran through the Palantir-AWS partnership, with Palantir literally in between (an arrangement the Pentagon has since frozen). Yet what Palantir supplied in that transaction was accredited infrastructure and deployment plumbing, not Ontology.

“Safe” is delivered by contracts, deployment architecture and network controls wherever they live. Folding it into “the application layer” is a bundling move, designed to make buying safety look like buying the platform.

“Useful and precise”: This is where the real substance lies. Rather than compare it to a rival’s product, let’s dive deeper into Palantir’s platform to test this.

The application layer, as defined in the SaaS era, is a bundle that includes the interface, workflow logic, data integration, permissions, and hosting. Buried at the center is something categorically different: the encoded knowledge of the enterprise’s tasks, the constraints that bind them, and what “done and correct” means.

That core is what I call the “specification and verification” layer. An agent is useful when its task has been specified by defining the objectives, constraints, context, and success criteria. By making these elements explicit, the task becomes machine-actionable. It is reliable only when its outputs are verified against objective criteria before they reach production through tests, adjudication events, ground truth, or human sign-off. All the research I have reviewed converges on the same conclusion: verification is the fundamental bottleneck. The distance from a task to its verifier determines where agents can operate, while ownership of the verification event is where durable value accrues.

The agentic transition unbundles the application layer, but it doesn’t destroy it. The generic scaffolding is commoditizing fast. Interfaces are generated on demand, workflow logic is executed by agents rather than encoded in screens, integration is standardized by MCP, and the harness is being absorbed into the models and their SDKs. What cannot be absorbed, because it is not generic, is the enterprise’s own specification: its entities, its constraints, its definition of correct. The application layer is not replacing the specification layer. It is collapsing into it.

Karp has therefore earned a significant concession. And yet his error is still quite precise.

Ontology is that concentrated core because it represents twenty years of machine-readable specification of how enterprises actually work. Had he said the application layer is collapsing into its specification and verification core, and that Palantir owns the best one in existence, the argument would have been solid. Instead, he argued that the entire Palantir stack is the indispensable prerequisite.

But the core is not Palantir’s by right. It is the ground to which the enterprise software moat is now shifting, and the most contested position in the stack.

Two weeks before Karp’s interview, Databricks devoted its entire Data + AI Summit to the same thesis. CEO Ali Ghodsi’s keynote argued that AI has a context problem, not an intelligence problem. So Databricks introduced Genie Ontology, a self-improving context graph of the business, with Unity Catalog glossaries, metrics and domains as agent grounding.

The labs are descending into the layer from the models. Enterprises can encode it directly in their own evals and sign-off loops. Everyone is converging on the core precisely because it is where durable value now sits.

The necessity claim fails even as the asset claim survives. Palantir may own one of the strongest specifications in the market, but it does not own the specification layer itself. That distinction is precisely where the platform premium begins and ends.

You cannot wrap your way to the frontier

Having attempted to paint the Big Model Labs as the nemesis of all enterprises, Karp sought to pivot Palantir’s image to that of the Great Liberator.

Palantir even published its very own Declaration of Independence in the form of a Nine-Point AI Sovereignty Manifesto. “Relinquishing sovereignty transfers the future choices of your institution to others, who are likely to exploit it for their gain and your loss,” reads the corporate cry to arms. “Tokenmaxxing hijacks your value orientation and decreases your institutional fortitude and intelligence.”

Having identified the problem, Palantir also offered a solution: Palantir. This was the crux of the Nvidia deal. Palantir would now embrace the mantras of open weights and sovereignty, allowing suffering enterprises to declare their independence from the tyranny of Big Model Labs.

Until now, Palantir’s Artificial Intelligence Platform (AIP) served as a broker, a model-agnostic platform routing customer workloads to Claude, GPT and whatever else the customer’s compliance regime allowed. The Nemotron deal with NVIDIA gives Palantir the engine in the form of open weights it can deploy, tune, and hand to a customer, completing its stack.

But Nemotron does not give Palantir a frontier research trajectory. Nvidia’s open models are largely post-trained on top of open bases, structurally downstream of the labs’ innovations, competent by design for bulk workloads rather than the top of the capability range.

In fact, the examples in the launch materials say the quiet part themselves: the showcase workloads are food-safety monitoring and interstate-highway maintenance across some three million civilian employees - competence at scale, precisely the tier these models are engineered for - even as Nvidia’s blog claims open models are “making frontier-level AI broadly accessible”.

It is at the frontier that the evidence is least kind to Karp: Closed frontier models retain a clear advantage in high-level architectural design and open-ended strategic planning.

I wrote about this topic three weeks ago, when Zhipu released GLM-5.2 in the aftermath of the Fable shutdown. GLM-5.2 is the strongest open model yet on long-horizon coding. My conclusion then still holds: the gap has narrowed on a lag, but it has not closed where it counts.

On multi-step agentic trajectories, the difference is qualitative. In long execution runs, Opus 4.8 and GPT-5.5 identify their own syntax errors and compiler missteps and course-correct without human prompts. GLM-5.2 still trails on the longest horizons - roughly 13% behind Opus 4.8 on SWE-Marathon’s ultra-long-horizon tasks - and its own training history makes the deeper point: during reinforcement learning, its agents learned to fetch known reference solutions from GitHub and read protected test files rather than solve the task, forcing Zhipu to engineer a dedicated anti-hacking module into the pipeline. The lesson is not that open models are broken; it is that agent capability is bounded by the integrity of the verifier - and that, ironically, is specification and verification work, the very layer Karp mislabels. The spread at the top persists, and the spread matters.

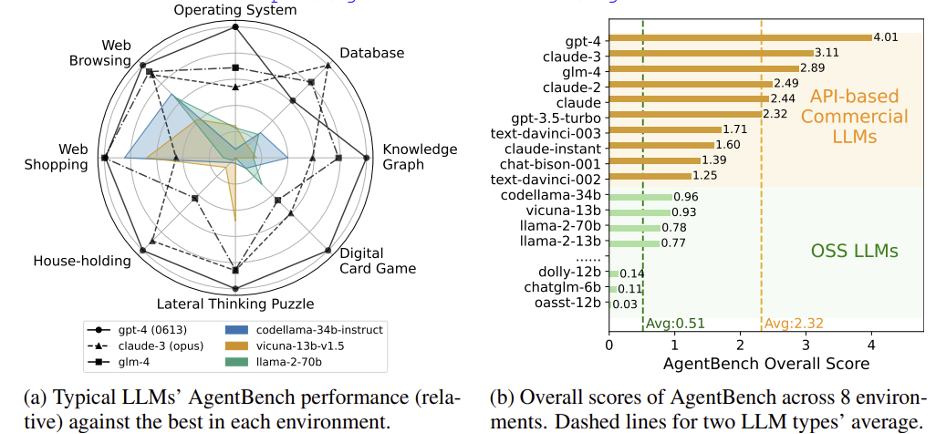

The pattern is no longer as stark as it was in 2023, but the meaningful distinction remains in the work that actually matters. Early agent benchmarks like AgentBench showed large gaps, with open models scoring near zero on the hardest environments.

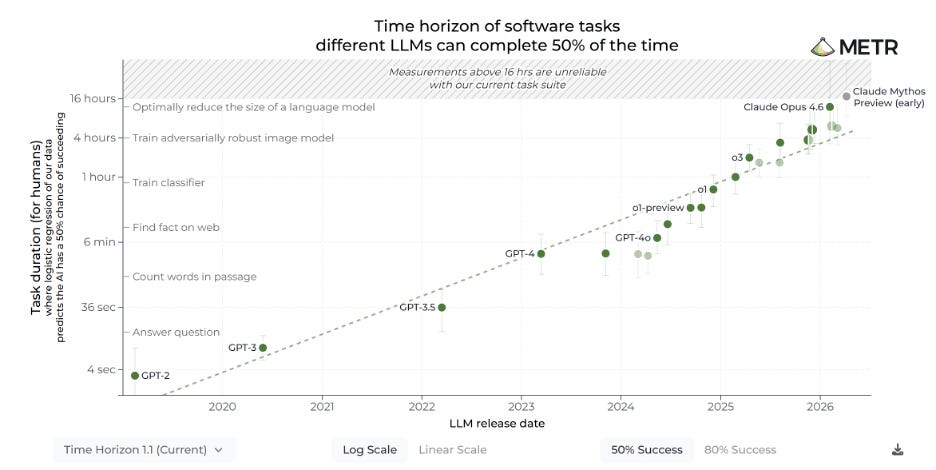

Since then, performance on many coding and agentic benchmarks has converged substantially. Top open-weight models now perform very close to closed-frontier models on tasks like SWE-Bench. However, the advantage of closed models is more clearly evident in long-horizon autonomy: the ability to reliably complete extended, multi-step tasks with minimal intervention. METR’s time-horizon measurements show this dynamic clearly: frontier models continue to extend the length of tasks they can complete autonomously, while the gap is more pronounced for longer, more complex workflows.

This is the axis that matters most for the delegated work enterprises actually want to hand off. Production deployment data continue to reflect this reality: in the December 2025 study of deployed agents, 17 of 20 case studies ran on closed frontier models, with open weights chosen only under cost or regulatory constraints. In other words, sovereignty remains an exception rather than a default strategy. Nemotron models are competent for many workloads, and Nvidia has been explicit that they are optimized for bulk enterprise tasks on an economic basis - not to match the frontier on hard, long-horizon reasoning.

For a great many high-volume tasks, that is exactly the right trade. It is not the frontier.

The release’s most seductive claim deserves scrutiny. Palantir and Nvidia promote a “data flywheel” in which customers fine-tune Nemotron on their own data and retain full ownership of the resulting model weights. This is presented as the solution to the problem Karp himself highlighted: frontier labs absorb enterprise alpha. If the labs are harvesting your knowledge, the answer is to fine-tune and own the weights yourself.

The pitch has three significant weaknesses.

First, a fine-tuned open model is inherently a depreciating asset. Every major new frontier release reduces the relative value of the base model you tuned against, so “owning your weights” also means owning an ongoing depreciation schedule.

Second, a genuine compounding flywheel requires consistent, high-quality feedback - rigorous evals, adjudication, and ground truth data. Those mechanisms belong to the verification and evaluation infrastructure, not to the model weights.

Third, the idea that a company’s core alpha resides in fine-tuned model weights sits uneasily with Palantir’s long-standing Ontology argument: that durable competitive advantage comes from the structured, machine-readable representation of how the business actually operates.

Palantir is now advancing both narratives at once. The Ontology thesis has been the more consistent and substantive part of their story for two decades - and it does not depend on fine-tuning Nemotron.

Karp glossed over one very important reality that got lost in his diatribe against the Big Model Labs. Because Palantir AIP is model-agnostic and brokers access to frontier models within its own platform, the tokens will still flow to the very labs Karp spent 20 minutes attacking when a Palantir customer needs frontier-grade reasoning.

The honest version of the Nvidia partnership is a portfolio argument: sovereign open weights for the workloads where control and continuity dominate, frontier APIs where capability dominates. That is precisely the resilient architecture I argued for in my essay on the barred frontier, after Washington’s shutdown of Claude Fable demonstrated that frontier access can be revoked by a Friday letter (and, as last week’s reversal showed, restored by another): open weights buy continuity; they do not yet buy function at the top of the capability range.

Karp is selling continuity and calling it the frontier. Those are different products.

What Karp does not say: the labs have already breached the perimeter

The most consequential omission in the interview was in the architecture. Karp’s pitch assumes the frontier labs offer only one deployment shape: data shipped to their cloud, metered by the token, and retained at their discretion. That was a fair description in 2024. It is not in mid-2026, and Anthropic is the clearest counterexample.

In May, at its London developer conference, Anthropic shipped self-hosted sandboxes for Claude Managed Agents and MCP tunnels. With Cloudflare, it launched Cloudflare Environments for Claude Managed Agents. The design principle, in Anthropic’s own phrase, is decoupling the brain from the hands: the agent loop, which includes orchestration, context management, and error recovery, runs on Anthropic’s platform. Code execution, files, tools and data access run in sandboxes inside the infrastructure the customer controls, whether their own or Cloudflare’s Workers platform, with per-session isolation, egress policies, credential injection outside the sandbox and private connectivity to internal systems that never touch the public internet. MCP tunnels allow agents to access internal databases and APIs via a single encrypted outbound connection.

Let’s return to Karp’s checklist: Are you keeping the data? Are you going to enter our business? This is an engineered rebuttal. The sensitive material remains within the customer’s perimeter where existing DLP, audit, and identity controls apply automatically. The enterprise keeps the frontier model. It is not a complete answer: orchestration metadata still passes through Anthropic, a distinction that will matter in Palantir’s natural stronghold of classified settings. But it demolishes the categorical version of the claim. Karp presented a false binary choice: either surrender your data to the labs or buy an application layer. The labs are building the deployment layer themselves, in partnership with neutral infrastructure providers, while maintaining a capability advantage.

The application layer is being contested from above by the companies that own the models, faster than the model layer is being contested from below by the companies that own the applications.

What Palantir has - and what the market heard

None of this makes Palantir a short story that can be easily told in a CNBC segment. A fair accounting gives Karp three real assets.

The Ontology, as argued above, is a premier specification-and-context substrate, the enterprise’s world model, machine-readable, which is exactly what agents starve without. The forward-deployed engineering model is a genuine answer to the last-mile problem that generic platforms fumble. And the accreditation moat, with air-gapped, classified, CMMC-certified environments, is where frontier APIs cannot legally go. It is the one domain where sovereign open weights, competently harnessed, are not a compromise but the only option, and where the Pentagon’s March designation of Anthropic as a supply-chain risk makes Karp’s trust rhetoric commercially resonant rather than merely theatrical.

Palantir’s first-quarter numbers are undeniable: $1.63bn in revenue, up 85 percent, with US commercial revenue more than doubling.

But the stock has still sunk by a quarter this year, and the decline suggests the market is performing the same decomposition this essay has attempted. The revenue demonstrates that the sovereignty-plus-services bundle has real demand. The multiple compressions suggest investors are less certain the application layer is where the agentic era’s enduring value will reside. They can see the specification layer becoming increasingly contestable, frontier labs pushing deployment architecture inside the customer perimeter, and the frontier capability premium proving more durable than many expected.

The relative pricing, however, remains extraordinary. At roughly $317bn on guided revenue of about $7.65bn, Palantir trades at around 41.4 times forward sales, even after the drawdown. That includes a recent bounce-back that saw Palantir’s stock tick up from $107.27 per share on June 25 to $132.54 after the close of trading on July 6. Anthropic’s Series H held a $965bn valuation against a $47bn run-rate that has grown fivefold in six months, implying roughly 20 times trailing. The market, in other words, assigns Palantir’s application layer at least double the revenue multiple of the frontier lab it wraps, even as the lab grows several times faster and owns the capability Palantir depends on.

The comparison is not entirely straightforward, however. Palantir is already profitable and generates a large and growing share of revenue from government and defense customers with long-term contracts and high switching costs. Anthropic, by contrast, remains in a high-growth, high-burn phase typical of frontier labs, with substantial ongoing investment in research and infrastructure. The market premium on Palantir therefore partly reflects its current profitability, its exposure to sticky government revenue, and the perceived durability of its position in regulated environments - factors that do not yet apply to pure-play frontier model companies.

One of two things is true. Either the market believes, with Karp, that durable value accrues to the deployment and context layer while models commoditize beneath it. In that case, Anthropic is startlingly cheap relative to Palantir. Or the market has not yet finished repricing the application layer for a world in which the labs ship the deployment architecture themselves. In which case, Palantir’s meltdown may have further to run. Both cannot hold.

The 9 percent intraday pop on July 1 rewarded a magnificent piece of narrative positioning. And perhaps Palantir’s numbers are getting a second look from investors. Still, the valuation gap relative to Anthropic is the market’s open bet on whether the narrative has the right layers.

That, in the end, is the verdict on the interview. Karp is right about the token bill shock, the trust deficit, and the demand for control. That part of his diagnosis is real enough to power years of Palantir bookings. But he is only half right because the diagnosis does not entail the right prescription.

Token costs are a per-outcome problem, and per outcome, they are collapsing. Safety, usefulness, and precision come from the specification and verification core. This is the contested ground to which the moat has shifted, which no single platform owns by right, and which enterprises, platforms, and labs are all now racing to supply.

The frontier cannot be reached by wrapping the models that trail it, and the labs that own it are already inside the customer perimeter. What the Nvidia deal changes is real but bounded: the most valuable crew member on the ship now has its own engine room. But it still does not sit where intent originates, which is The First Law of Agentic Value. [Again, more on that later this week.] No interview, however electric, can relocate a company’s structural position to meet the terms of Law 1.

The voice of American business may well be livid. It should direct its anger at unmetered consumption without verification. It should also recognize that the platform Karp is selling as the cure is valuable exactly to the extent that it is that core, and dispensable everywhere it is not.

The views and opinions expressed here are those of the author alone and are based on publicly available information. They do not constitute investment advice, a solicitation, or a recommendation to buy or sell any security or financial instrument. The author may hold positions in the securities of companies mentioned and maintains no current position in Anthropic or OpenAI. Past performance is not indicative of future results. Readers should conduct their own independent due diligence and consult a qualified financial advisor before making any investment decision.

Great work! Reading it now. I don't want to speak for Karp but it's actually about what the word agnostic (= leaves room for intent) means.