'Non-AI'? Why Alan May Be One of Insurtech’s Most Deeply AI-Integrated Companies

The Financial Times' mislabeling of the French insurtech reveals a deeper market blind spot: the biggest winners of the Agentic Era will be firms that own intent, context, workflows, and verification.

TLDR: French insurtech Alan raised €480 million in a round that the Financial Times first called one of the largest by a “non-AI” company. That mislabeling of Alan points to a more fundamental error: how markets keep misjudging which companies are making the transition to the Agentic Era. In the Orchestration Economics framework, Alan serves as a case study of a company making the crossing. Alan is a disruptor that owns its context, workflow, and the verifier that decides whether its agents are right. That last asset is the most decisive and least-watched test of who crosses the agentic threshold and who is displaced. In Alan's case, the binding constraint may ultimately come from capital rather than technology.

When the Financial Times described French insurtech Alan’s latest funding round as Europe’s biggest “non-AI” fundraising of the year, it mislabeled the company in an interesting way. In this case, the miscategorization of the unicorn is not just about marketing buzzwords.

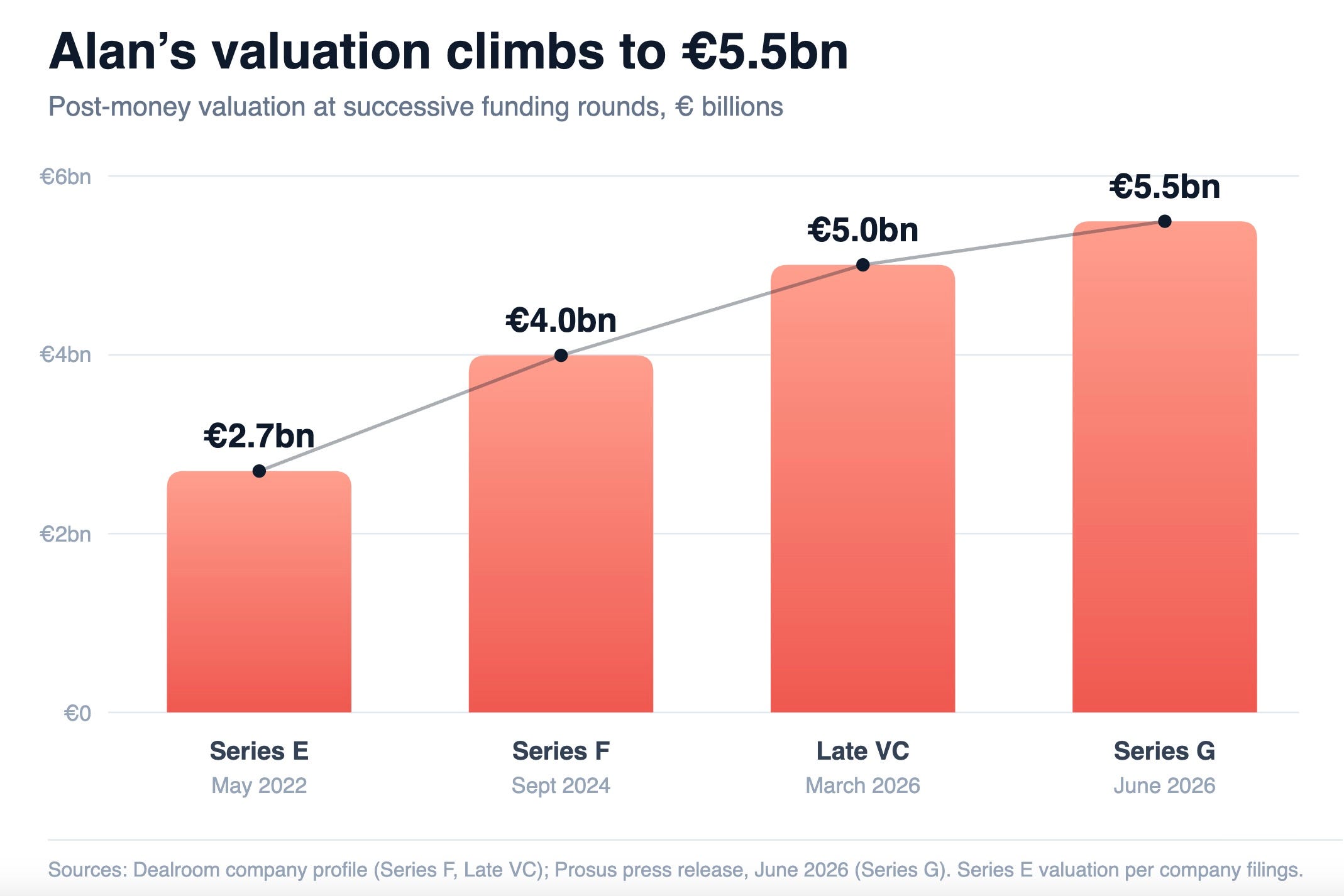

On June 25, the paper broke a story that offered a counter-narrative to a venture world that seemed interested in nothing but AI: “Prosus leads €480 million investment in French health tech startup Alan,” read the headline over a subhead noting that the “Paris-based group raises one of Europe’s largest non-AI start-up rounds this year.” The FT later swapped that subhead for the more anodyne “The deal values the 10-year-old Paris-based group at €5.5bn.”

The difference between the two subheads is worth examining. But not just to question the FT’s editorial judgment.

Rather, the miscategorization is entirely understandable because it is a microcosm of the larger struggle playing out across markets as they try to price the impact of generative and agentic AI on legacy software. This is most evident in the binary debate of software versus AI. The market’s reflex may be directionally correct for some categories, but it is analytically lazy. Alan is an example of why the binary framing is wrong. It is proof that some existing companies can make the crossing to the Agentic Era.

As I wrote in Orchestration Economics when discussing the February 2026 SaaSpocalypse, this is “a confused, simplistic attempt to price a structural shift in where control, coordination, and value capture reside”. This is not the death of SaaS. It is the Software Sorting,” a re-ranking of where value will sit “when autonomous agents become the primary actors inside enterprises.”

The harder question for investors is how to tell which companies can make the crossing and which can’t. That question reaches well beyond software.

In Orchestration Economics, I reserve a specific label for a company that has secured the structural position to capture value in this new paradigm: AGNT. It is an end state, not a badge handed out for momentum. A company earns it only once it holds the orchestration position and shows the value separation that proves it.

Alan has not arrived there. But of the companies I track, it is one of the clearest emerging orchestrators: a disruptor already building the new playbook rather than an incumbent wondering whether it can.

We have misread the dawn of an era before

The “non-AI” reflex is not new. It is the latest version of a mistake that markets make at the start of every general-purpose technology: confusing a force that reorganizes an economy with a like-for-like upgrade.

When electricity reached the factory, the first generation of owners treated it as a cleaner alternative to steam engines. They pulled out the central steam plant, dropped a single large electric motor in its place, and kept the same overhead shafts and belts driving the same machines in the same order. The power source changed. The factory did not. And for three decades, the promised productivity gains barely showed up in the numbers. They arrived only when a later generation stopped swapping the engine and rebuilt the factory around the new principle: small motors on each machine and floor plans laid out around the flow of work rather than the geometry of the belts. Productivity then climbed steeply, and industrial leadership reshuffled.

The economic historian Paul David used this story precisely to explain why the computer, too, took decades to surface in the productivity statistics.

“Non-AI” is the modern “just a cleaner engine.” It looks at Alan, sees an insurer selling insurance, and files it under the old economy.

The first wave

Go back to September 2024, barely two years ago, in a timeline that already feels like another epoch. It was less than two years after the first public release of ChatGPT. Anthropic would not publish the Model Context Protocol for another month. Generative AI dominated the conversation, with the turn toward agents still over the horizon.

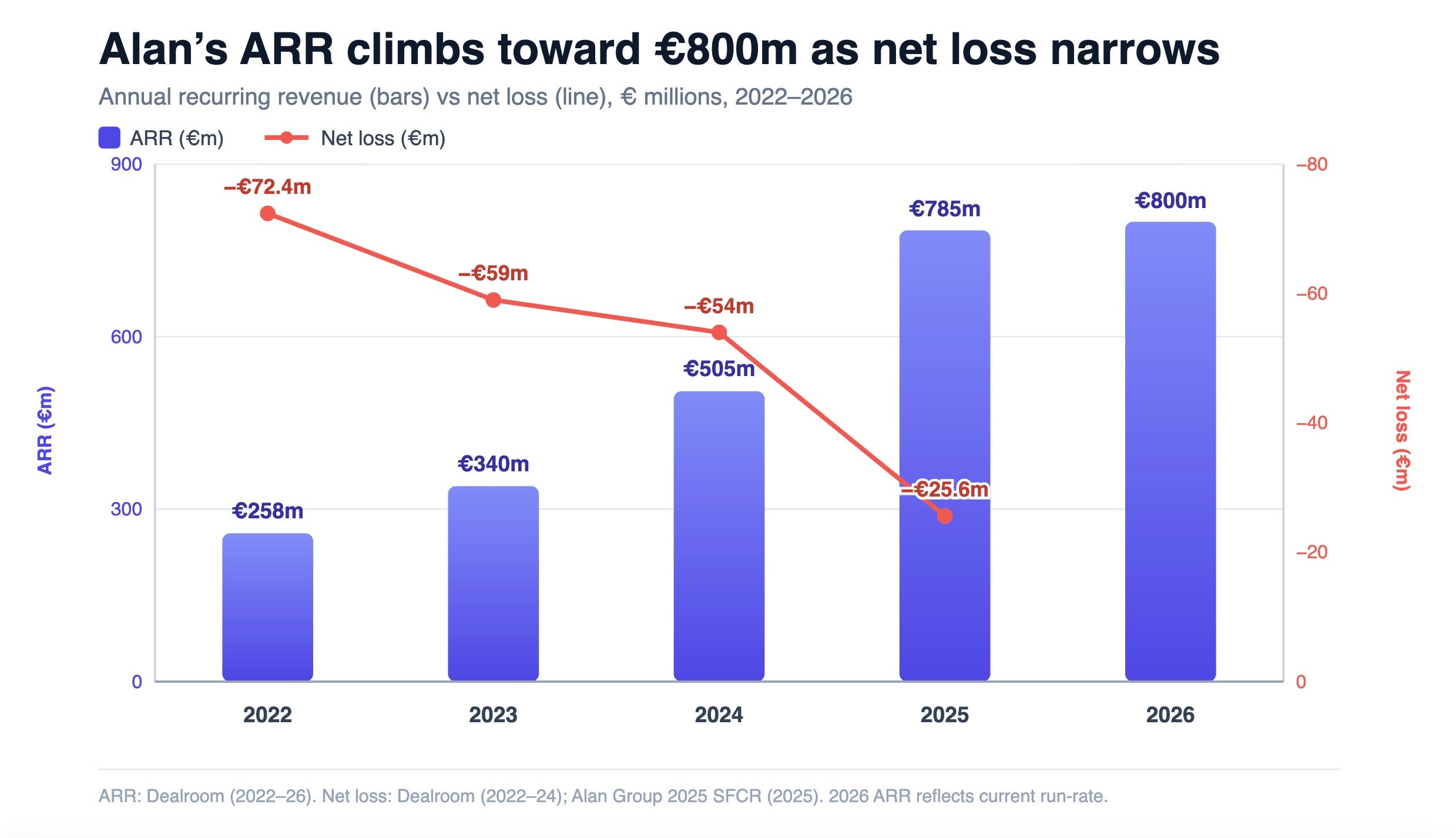

That month, Alan, already a unicorn, raised €173 million at a €4 billion valuation. It was the largest insurtech round in Europe that year, accounting for close to one in four euros invested in the sector. The mood elsewhere was unambiguous: Insurtech was a dead category, software multiples were stumbling, and the only heat in the room was generative AI.

But even then, Alan had established itself as a disruptor. It received the first new health-insurance license granted in France since 1986 and, in the decade since, has grown from nothing to 1.1 million members and roughly 37,000 corporate clients across France, Belgium, and Spain.

I argued at the time that the valuation was not, in fact, crazy. Alan’s leadership had already begun an aggressive investment in generative AI. Not a chatbot bolted onto a legacy stack to pass as cutting-edge, but AI worked into the core. “In Alan’s case,” I wrote then, “GenAI is already enabling gross margin improvement that has solidified its unit economics, put it on a path to profitability, and given it an advantage over other insurance incumbents.”

The detail mattered: Alan had integrated AI across the business, reporting a 28% cut in per-member administrative cost in 2023, with automation concentrated where insurers bleed: claims analysis and fraud. My case was that recurring revenue was the wrong lens for Alan, because it competes against incumbent insurers rather than software peers, and that the real story was margin. Gross margins are razor-thin in insurance, which is what sank so many insurtechs. It helped that Alan’s founders are also Mistral co-founders, which gives the company privileged access to sovereign European models in a domain where data residency is not optional.

That was early. The company used the round to accelerate, and it had already placed itself at the vanguard of the agentic crossing, in the part of the economy I describe as Wave One in Orchestration Economics: insurance, with claims adjudication against codified coverage rules, deep historical loss data, and a high routine-to-judgment ratio, alongside banking, corporate services, and customer support, where autonomous resolution has already been demonstrated at scale within weeks of deployment.

That performance is reflected in the numbers. ARR reached €804 million in early 2026, up from €340 million two years before, growth of 48% and then 53% in consecutive years. Management is guiding past €1 billion this year. Meanwhile, its valuation has climbed from €2.7 billion in 2022 to €5.5 billion today. Unusually for a company growing this fast, it is also moving toward profit: France turned EBITDA-positive in 2025, and group losses roughly halved.

That combination is the analytically interesting part. High-growth challengers usually buy growth at a loss. Profitable insurers usually do not grow at this rate. Alan is doing both, and its own accounts credit AI for the margin side thanks to automation concentrated in claims and fraud, where insurers tend to bleed.

Alan is already a challenger, restructuring around AI. It is not acting like an incumbent debating whether to embrace AI or simply defending its existing position.

The anatomy of the crossing

With almost two more years of operating history, Alan is a clear test case for the frameworks of Orchestration Economics.

The core thesis of Orchestration Economics is that as the marginal cost of cognition collapses and machines become actors, the ultimate value-capture position is to be the orchestrator. The shift underneath everything is in the unit of production. It is no longer the human labor hour but the orchestrated workflow. A new layer has inserted itself between people and the tools they used to operate directly. Its outer ring is reorganized around intelligence, delivering outcomes from operational context that no one else owns. Whoever holds this outer-ring position captures the surplus value created.

Every existing company, therefore, carries two value curves: the fundamentals curve and the orchestration curve. The mistake markets keep making is assuming almost no one can reach the orchestration curve and therefore pricing this option at zero.

When I assess a company, two questions do most of the work.

First, does it own the operational context in its domain? This is the proprietary record of decisions and outcomes a business accumulates by living in it. If not, it may be a replaceable layer sitting atop someone else.

Second, can it turn that context into the layer that tells agents what to do, rather than remaining the place where outcomes are merely recorded and looked up?

The answers distinguish between companies facing existential risk and those facing a value-capture negotiation. Underneath are the Three Laws of Agentic Value that I developed:

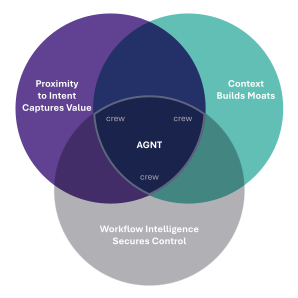

First Law: Proximity to Intent Determines Value Capture. The entity closest to the moment a human expresses a goal captures routing authority, relationship ownership, and the economics of the phase transition. Everything downstream is an API call.

Second Law: Context Builds Moats. Competitive advantage belongs to whoever accumulates the richest operational context and embeds it in their orchestration layer.

Third Law: Workflow Intelligence Secures Control. The accumulated choreography of how work gets coordinated creates switching costs that grow with every interaction.

The blunt test for any business is whether, in the new graph of automated work, it commands the orchestration of work or is merely called by it. Captain or crew. A company can have world-class engineering and still be the crew on someone else’s ship.

Let’s evaluate Alan against the Three Laws.

First Law - proximity to intent

For a French employee, the moment of health intent - I’m unwell, what’s covered, book me someone - increasingly forms inside the Alan app rather than in a phone queue or a broker’s office.

According to Alan’s figures, roughly three in ten members are active each week and one in ten every day. The in-app clinic, staffed by salaried clinicians seven days a week, leads many users to skip an in-person visit. A partnership with football superstar Kylian Mbappé and gamified prevention programs has also helped make the app the first-place health-intent surface.

Alan’s first-quarter 2026 letter to shareholders reported that 81% of members now choose Mo, its health companion, even when they arrive looking for a doctor. There is an important caveat: France mandates employer-provided coverage; 95% of Alan’s book is about collective contracts, and the employer owns the first touch and can switch at renewal. But for the recurring, daily reality of health, the part that compounds, Alan increasingly owns the front door.

Second Law - context

This is Alan’s strongest dimension, and the one a “non-AI” reading misses entirely, because it never shows up on the app’s surface.

As a single company that both insures and delivers care, Alan owns something a general-purpose model cannot assemble: pairs of decisions and their outcomes at scale. Every claim carries an outcome; every clinical conversation carries a resolution. The medical-advice chat alone handled more than 58,000 conversations between members and health professionals in the first nine months of 2024, as documented in Alan’s own clinical study.

Add reimbursement histories, coverage tables, member health profiles, and, since the March 2026 acquisition that became Alan Précision, longitudinal biomarker data under physician supervision, plus the occupational-health corpus from its Prévenir line; Alan has consented to EU-hosted, regulated health data that no horizontal AI assistant has a path to replicating.

The discipline I apply is a simple test: count only the context that survives synthesis. Interaction patterns can be generated artificially, and Alan should assume the generic layer commoditizes. Neither a real insurer’s adjudicated claims history nor a real cohort’s clinical outcomes can be generated. They have to be lived.

The moat is not what Alan stores but the rate at which its history improves the next decision, which is why its defensibility deepens as it ages.

Third Law - workflow, and why it holds

Alan directs the work rather than being sequenced into someone else’s process. It owns the full chain, including pricing, claims processing, fraud detection, care navigation, and member support as one connected loop, and has automated parts of it steadily. Document handling on incoming claims rose from half of French claims to two-thirds in 2025. Fraud detection prevented about €1 million in a single quarter. Reimbursements are processed in minutes, and roughly 40% of care conversations are now handled without a person.

The clearest agentic piece is in claims support: Alan’s Claim Agent investigates and explains members’ reimbursement questions. This is the single most complex category of support, about a fifth of all tickets. According to Alan, it fully resolves roughly a third of the ones it handles. Because Alan both prices the risk and runs the care, prevention, and automation lower its own cost base, and outcomes and margins reinforce each other instead of trading off.

Still, the Third Law is the most vulnerable of the three. The first two require assets such as relationships and operational history that cannot be manufactured. In contrast, workflow, stripped of its context, is something agents can increasingly learn. What likely makes Alan’s workflow defensible is the context of the first two Laws, which expresses itself through the third.

The Three Laws, though, settle only where a company sits. They say nothing about whether it can run that position once agents, not employees, are doing the work. In my framework, that is a separate axis, the one I call “agentic readiness.” A company can sit exactly where the Laws place it and still be crew.

The readiness axis has several components. The most critical turns on one question.

The fourth axis: who owns the verifier

That question is verification. Holding a position and being able to operate it once agents do the work are different things. The decisive component of readiness is whoever owns the mechanism that decides whether the output is correct. Models cannot reliably check themselves. As I argue in the Manifesto, their reasoning is genuine but systematically fragile, which makes external verification not a passing feature but a permanent toll. Whoever owns the verifier collects this toll.

Some domains check themselves cheaply: code passes its tests, or it does not. Some never check cleanly: judgment, taste, strategy. The valuable middle is what I call made-verifiable. This is a domain with weak natural ground truth that someone converts into reliable ground truth by owning and operating the thing that says, “yes.” A roadmap to build one does not count. A model grading its own work does not count. You have to own the verifier. Alan owns two.

The cleaner case is claims. Let’s be clear about precisely what work the agent performs. Alan’s Claim Agent does not decide claims. It answers members’ questions about them, reasoning over read-only, Alan-owned tools to investigate why a reimbursement came out as it did, and handing off to a person the moment a step fails. What makes that agent reliable is that the thing it reports on is already verified: Alan, as the insurer, owns the adjudication itself. The reimbursement is deterministic once you have the rules, and Alan is the rules. So “does this claim pay, and how much” is an event the company computes and owns outright. The agent consumes a ground truth Alan controls rather than guessing at one.

The harder case is clinical. Whether medical guidance is correct is not naturally verifiable, so Alan manufactured the verification. It employs clinicians who review and sign off on every companion conversation within about fifteen minutes. In a controlled study Alan published, clinicians rated the assisted conversations highly and flagged no safety concerns under physician oversight, with patients answering faster than when asked by a doctor alone. This is exactly the gap the production-agent study identified in insurance, where correctness normally surfaces only later, as a loss or a contested payout. Alan is a rare case who engineered the signal rather than waiting for it.

That single design choice does three jobs at once. It is the reliability mechanism that lets a patient-facing health tool exist at all. It is the regulatory shield that keeps the companion on the safe side of Europe’s medical-device and AI rules. And it is a moat that synthetic data cannot copy because you can fake a conversation but not a signature or a book of liabilities. A general assistant can answer a health question and describe how a claim might be paid. It cannot sign off on the answer, and it cannot own the adjudication on which its description depends, because it holds neither the clinician nor the liabilities. The gap between answering and standing behind the answer rests on infrastructure: a single multi-country stack that is being rebuilt to enter markets faster, an internal coding tool that lets non-engineers ship to production, and l, a fleet of internal assistants used weekly by most of the staff.

The irony of the “non-AI” label is that, by these measures, Alan is more technology-leveraged than most companies sold as “native AI.” Many of the latter are just thin wrappers whose reliability is rented from a model provider and whose function a larger platform can replicate in an afternoon.

Two years on from my 2024 assessment, Alan has used these tools to expand its mission and strategy from insurance to “prevention insurance.” And my forecast is now visible in the income statement: France reached operating profitability last year, losses roughly halved as a share of revenue, recurring revenue passed €800 million across 1.1 million members, and sales productivity per representative rose by half. The structural point beneath the numbers is that Alan owns and automates its workflows rather than selling labor that automation has commoditized. The businesses this transition destroys are those whose revenue comes from labor that software now performs cheaply. Alan’s revenue is from insurance. The labor software now does cheaply is its own cost base, so every increment of capability lands as margin it keeps.

One shouldn’t mistake Alan’s success for invincibility.

For instance, the very thing that protects Alan, a verifier embedded in a regulated, clinician-gated domain, is a damped moat, and damping is a wasting asset. Regulation slows the imitators today. It will slow them less as Europe’s rules clarify and as open European models, Mistral among them, close the capability gap.

Beyond that, while Alan’s position is strong, it is also bounded. Three things could displace it:

The first is the front door. If members begin reaching care through general assistants, or if Prosus routes Alan beneath its own consumer layer rather than feeding it, Alan slides toward being a back-end utility, and the intent argument weakens.

The second is the verifier boundary. The case rests on that fifteen-minute clinical sign-off and the owned claims adjudication, and weakening the human gate in pursuit of autonomy, or tripping a medical-device reclassification, would move the moat and the reliability story together in the wrong direction.

The third, and the binding one, is capital rather than technology. Alan is a licensed underwriter, not a broker, so it must hold regulatory capital against the risk it carries: under the EU’s Solvency II regime, every new member and every euro of premium add to the reserves it has to keep, and growth therefore consumes capital rather than throwing it off. Its solvency coverage has fallen as the book has grown, from more than seven times the required minimum at the end of 2022 to roughly three and a half times by 2025, the normal signature of a scaling insurer drawing down its cushion. That, not a product release, governs how fast it can cross: each new country needs a fresh capital base, which is why Alan has raised round after round. The €480m from Prosus replenishes the buffer, which is why the deal matters more to the balance sheet than to the headline.

That said, it’s important to keep in mind the larger agentic picture. Most companies will not cross. Of the few hundred large incumbents genuinely exposed to the transition, my read is that roughly twice as many face value compression as emerge as durable orchestrators. The asymmetry is that destruction is priced in days and creation in years: the casualties re-rate fast, and the crossers re-rate slowly, because they look like the businesses they are disrupting.

.Alan looks like an insurer. That is why it was mislabeled and why the label is worth correcting.

I provided advisory support to the Prosus team during the Alan funding round discussed in this piece. The analysis above is my independent perspective and does not constitute investment advice.