SpaceX’s $22.7 Trillion AI Black Hole: Anthropic Wrote the Playbook. Now SpaceX Must Run It at Double Speed.

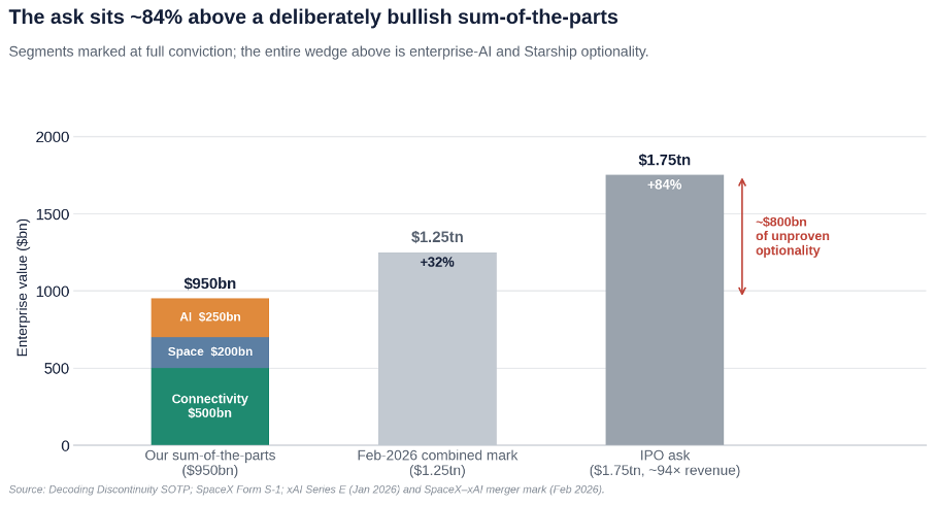

Wall Street priced SpaceX for an enterprise AI empire no bank can yet model. The valuation gap that began as an $800 billion black hole is now nearing $900 billion.

TLDR: SpaceX claims a $22.7 trillion opportunity in enterprise applications, but the post-IPO analyst models overwhelmingly underwrite compute rental rather than software, customers or switching costs. Cursor, Sand, and Grok now give SpaceX a credible mechanism to pursue that market: the coding-to-orchestration playbook that Anthropic used to enter the enterprise. But SpaceX is beginning after Claude, OpenAI, and Microsoft have already occupied the field, with no shipped general-purpose agent or demonstrated external adoption. The enterprise thesis has therefore moved from unsupported to plausible, but remains a time-sensitive option. SpaceX’s valuation ($1.8T as of July 14th) prices that option as though the playbook had already been executed.

Last week, the SpaceX valuation debate was compressed into five days. On Tuesday, July 7, the quiet period (the 25-day post-IPO window during which underwriters cannot publish research) lifted, and the lips of more than a dozen brokers were finally unsealed as they publicly initiated coverage, all but one at a buy-equivalent rating (the lone Neutral carries a $131 target). On the same day, Anthropic extended Claude Cowork, its general work agent, to mobile and web.

On Wednesday, SpaceX’s AI division released Grok 4.5, its bid for the model frontier. A day later, OpenAI unveiled ChatGPT Work, an enterprise agent powered by GPT-5.6. Then, that same afternoon, The Information reported that Cursor - the coding company SpaceX is acquiring for $60 billion - was developing a general-purpose work agent codenamed Sand and had begun testing it internally in late June. It remains unnamed, unpriced, and unlaunched. One week: the research, the model, the rivals’ agents, and the leak of SpaceX’s own, while the stock traded below its first-day close. If you want to judge the largest TAM number ever printed in a prospectus, the evidence is now on the table. Or should be.

Instead, that number remains the $800 billion black hole I wrote about before the IPO and now approaches $900 billion at the company’s current price.

The force creating that black hole was the S-1’s $22.7 trillion “enterprise applications” claim: 86% of the AI opportunity, supported by one sentence and no visible bridge from SpaceX’s actual compute, data, and model assets to enterprise workflows, customers or switching costs. Except for references to the “Macrohard” product whose work has stalled at xAI per the same The Information article.

One month later, that conclusion deserves refinement, but not reversal. The Cursor acquisition, the emergence of its general-purpose agent Sand, Grok 4.5, and SpaceX’s vertically integrated compute stack now supply a credible valuation mechanism. The black hole is no longer entirely empty. It has become an option.

Yet the banks that initiated coverage have not underwritten that option as an applications business. They have mostly underwritten capacity, while allowing the applications narrative to carry the multiple, while effectively dodging this issue.

One can now see SpaceX/xAI assembling parts of the mechanism that Anthropic already demonstrated with resounding success: enter the enterprise through coding (the “Coding Wedge”), where output can be verified; expand into general work; then occupy the orchestration layer where a company’s context and workflows compound around the agent. SpaceX now has real ingredients for a version of that playbook and a cost structure Anthropic does not.

What it does not have is Anthropic’s head start, a shipped general-purpose enterprise agent, external adoption or an uncontested field in frontier capabilities. Nor would winning the orchestration layer make the filing’s $22.7 trillion revenue pool real at face value. The same automation that expands the addressable work also lowers its price as I develop it later.

The Enterprise Applications business of SpaceX has moved from an unsupported assertion to a credible but time-limited option, while the valuation prices the playbook as though it had already been run. In this article, I want to explore what Wall Street actually modeled, whether SpaceX can execute the Anthropic path, and what remains when the option is separated from the infrastructure business.

The banks priced the small bucket and sold the large one

The ratings tell one story: all but one initiation at a buy-equivalent, with targets running from $131 at the lone Neutral to $800 (!) at the most exuberant. The models beneath them tell another, and it is the same story at every bank that published one.

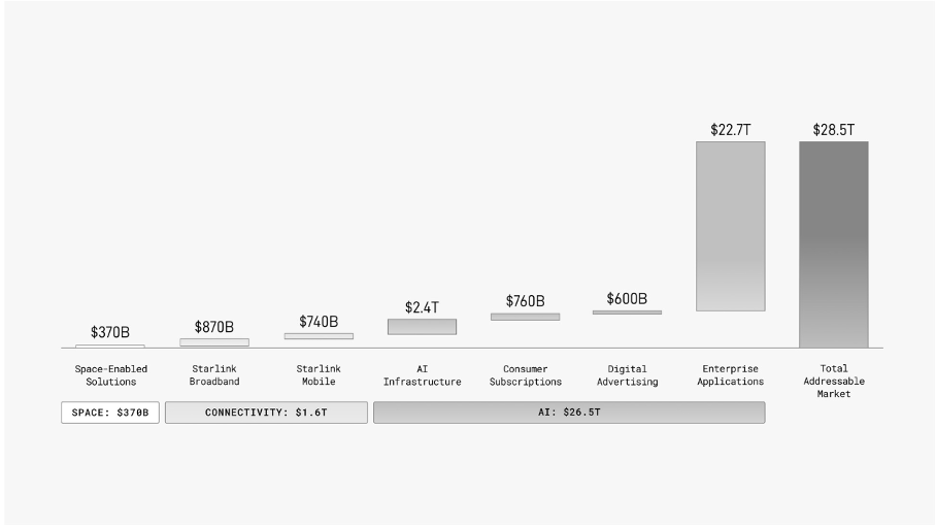

Across the initiations, the projected AI revenue is overwhelmingly compute monetization - capacity built and sold or rented to third parties. Enterprise software and agents, the business that is supposed to justify the $22.7 trillion, survive as a residual: on the order of a tenth of the modeled AI revenue, standing in for 86% of the stated opportunity in the S-1, inside segments projected at the margins of a data-center landlord rather than a software empire.

The tell is not the estimates. It is the unit of account. The street’s frameworks for SpaceX’s AI segment are built in dollars of revenue per gigawatt of capacity: anchor the addressable market to global cloud infrastructure spending - a figure more than an order of magnitude smaller than management’s $22.7 trillion - sort every use of a gigawatt into workload categories, and apply a blended capacity yield, on the logic that SpaceX will steer its compute toward whichever use pays best in a given quarter. In that arithmetic, an enterprise application is not a business with customers, seats, and switching costs. It is a higher-yielding use of a gigawatt - a premium tenant for the same capacity.

Nobody has ever valued Salesforce in dollars per gigawatt. The choice of denominator tells us everything: what the street can underwrite is capacity, flexed toward whichever meter runs hottest. What it cannot underwrite - what no initiation even attempts - is an applications franchise.

The frameworks are candid about one more thing. Today’s hosting economics reflect scarcity, not steady state: the flagship compute deals are structured, by Musk’s own public description, with mutual cancellation on 90 days’ notice, at rates the street broadly expects to normalize lower as supply arrives.

In every credible model, then, the revenue comes from the small bucket: infrastructure, 9% of the company's stated opportunity by its own arithmetic. The narrative and the multiple come from the large one. A dozen reports in one week, and not one names the seam.

So, the question the sell side declined to answer falls to us: is there a credible path from a compute business to the $22.7 trillion? There is. We know it because someone has already walked it.

Anthropic wrote the playbook, and it currently ends at a trillion dollars

Let’s first clarify what this market actually represents because the S-1 never does.

The $22.7 trillion is not enterprise software spending. That market is well below $2 trillion a year. It is, in effect, the wage bill for the knowledge work agents might perform. The customer is buying an outcome, not just an application: a ticket resolved, a ledger reconciled, a report filed, a feature shipped. The vendor captures a share of the labor cost it replaces. That is the only plausible mechanism by which an AI company can address a market measured in tens of trillions. It is also why the decisive battleground lies in the orchestration layer between AI labs and software incumbents. The agent that controls the workflow map can translate intent into a verified result without requiring a human to coordinate every step.

xAI does not need the best model to become important in the enterprise. If customers are buying completed work rather than model access, the decisive variables are reliability, cost, and control of the surface where intent is expressed.

Anthropic demonstrated the path. It entered through coding, where outputs can be verified automatically, and then expanded the same agentic loop into broader knowledge work. As its agents connected to more systems and completed more tasks, they accumulated a map of how each enterprise operates: where information resides, how workflows flow, and which actions succeed. Individual systems of record see only their own transactions; the orchestrator sees the connections between them. Models commoditize. That operational context compounds.

The market has rewarded that position with a valuation approaching $1 trillion. This is the only credible mechanism by which the $22.7 trillion claim becomes more than rhetoric. And it is the playbook SpaceX is now assembling the pieces to run.

SpaceX’s version: a genuine triple advantage

Here, the bulls deserve their due: the underlying pieces are real, and the way they fit together is strategically coherent.

The first is the intent surface, and its reach extends well beyond coding. Cursor, with roughly $4 billion in annual recurring revenue, has become one of the primary environments for creating software. But its more consequential evolution - and the explicit purpose of Sand - is to capture business intent itself: a product manager, analyst, or operations lead states what they need in plain language and receives finished work in return, without routing the request through a developer or purchasing a dedicated application.

The $22.7 trillion is addressable not from a developer terminal but from the desk of every knowledge worker whose intent converts directly into output. Cowork and ChatGPT: Work starts with chat and moves toward work. Cursor starts from the deepest form of work, building the software itself, and reaches toward everyone.

And unlike a challenger assembling context from scratch, Sand inherits a running start. Cursor is already entangled inside thousands of engineering organizations, codebases indexed, workflows learned, and security reviews passed. The expansion motion is land-and-expand within the accounts SpaceX already holds: from the engineering floor to the desks around it.

The second piece is price, and it comes from the cost structure, not a promotional discount.

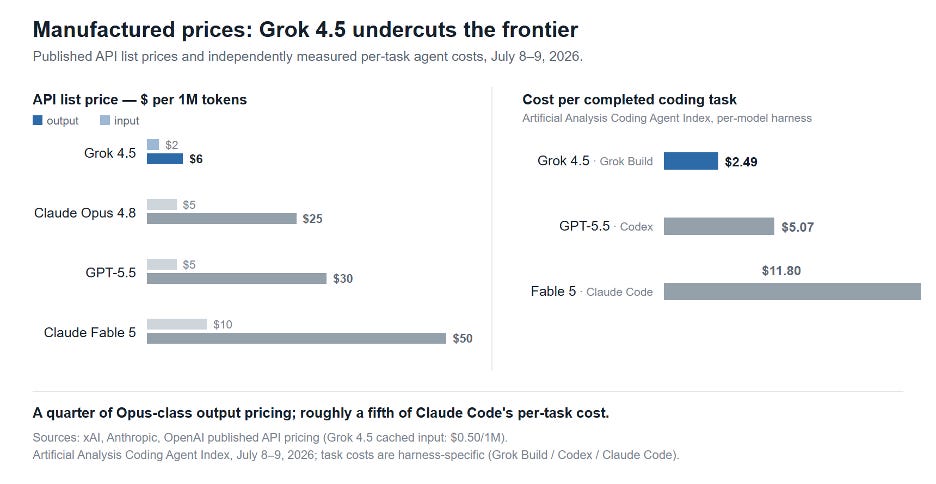

Grok 4.5 lists at $2 per million input tokens and $6 per million output tokens, compared to $5 and $25 for Claude Opus 4.8, and $10 and $50 for Claude Fable 5. On independent coding-agent evaluations, it completes tasks at roughly $2.49 apiece, compared to $11.80 for Claude Code.

The source of that gap is structural but requires nuance because Google already runs a vertical stack from self-designed TPUs through Gemini to applications, and Amazon designs its own Trainium silicon. What SpaceX is assembling is integration one layer deeper and one layer higher than either: Terafab would make it the only AI company that owns the fabrication itself rather than the chip design - every rival fabs at TSMC - and Starship the only one that can deploy capacity beyond the grid. For now, the depth is aspiration. Colossus runs on purchased Nvidia GPUs, and Terafab’s pilot line is scheduled for 2027. The stack that exists today runs from the data center up: Colossus, the Grok models, the Cursor harness, the agents on top - vertical above the silicon, merchant below it.

Cost advantage flows up the stack: cheap silicon makes cheap compute, which makes cheap tokens, which make cheap work. Learning flows down: Cursor’s developer sessions became Grok 4.5’s training data, and Musk himself credited that data with this generation’s leap. Rivals rent their compute. Some of them, in a detail we will return to, rent it from SpaceX.

The third piece is capability: close to the frontier, though the evidence is mixed and the launch rhetoric ran ahead of the independent results.

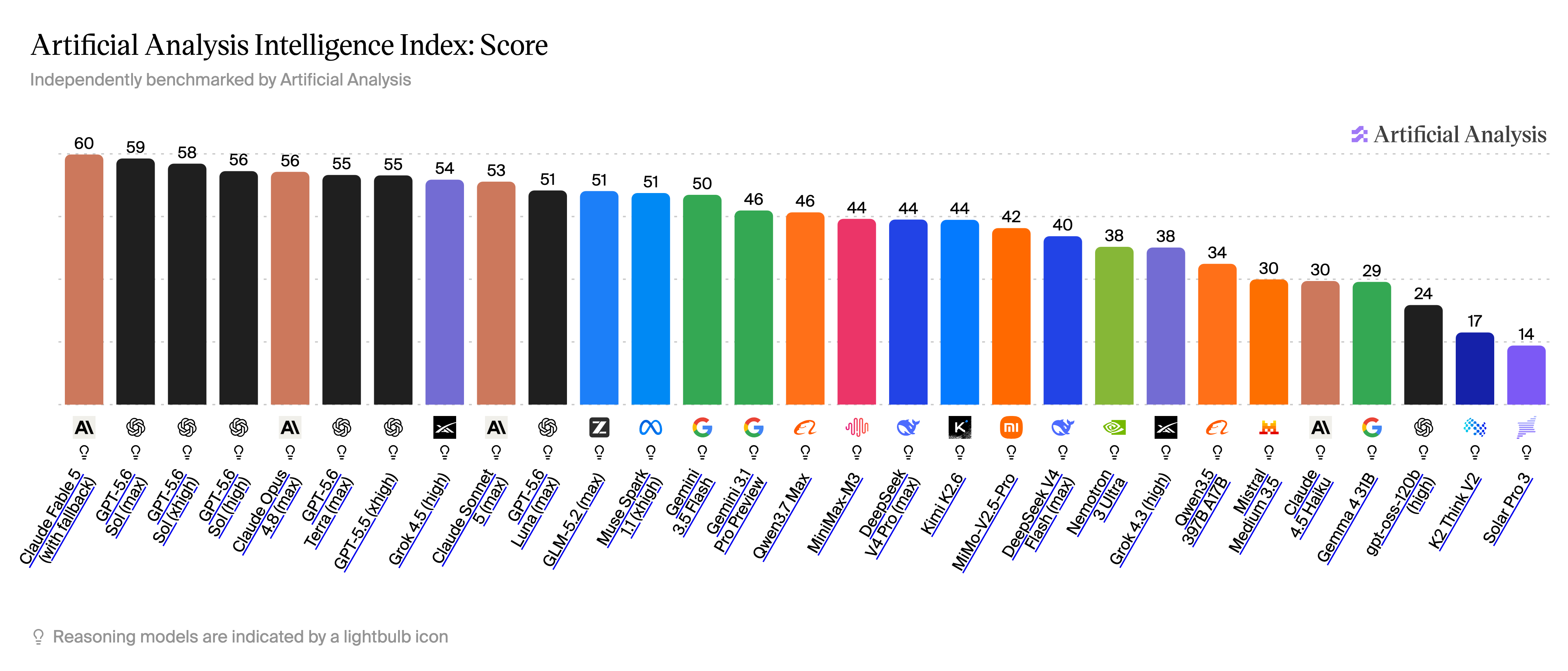

On Artificial Analysis’s independent Intelligence Index, Grok 4.5 scores 54 - behind Claude Fable 5 at 60, behind GPT-5.6 Sol, launched the day after Grok, at 59, behind Opus 4.8 at 56, and behind even OpenAI’s mid-tier Terra at 55. The more revealing comparison appears in xAI’s own launch materials: Grok 4.5 outperforms Opus 4.8 on a provider-controlled SWE-style coding harness, 62% to 56%, but falls behind on the neutral benchmark, 53 to 59. xAI disclosed both results. Its ‘Opus-class’ positioning depends almost entirely on the former.

Claude Fable 5 leads every benchmark on xAI’s own chart. Musk conceded the point himself: “Fable is definitely better than Grok 4.5, but most tasks don’t require Fable-level capability.” That is the strategic claim: almost-frontier is the commercial threshold for the routine middle of enterprise work. And on a handful of agentic-service evaluations (τ³-Banking among them), the model genuinely leads. None of the pieces is sufficient on its own. Price can be matched, capability can be rented, and an intent surface built on a weak or costly engine is little more than an empty storefront.

The $22.7 trillion thesis rests on their intersection: near-frontier work, produced at structurally lower cost and delivered at the point where enterprise intent is expressed. It is Anthropic’s playbook with a cost structure Anthropic does not have.

One caveat is worth stating before testing the thesis. Cursor reportedly failed to raise independently at a $50 billion valuation in March, as late-stage investors questioned application-layer margins, before agreeing to a $60 billion all-stock sale to SpaceX. The price is better understood as the cost of acquiring proprietary training data and an enterprise beachhead than as proof that the application layer has solved its economics.

Why starting later means running faster

Now, let’s turn our attention to the central tension. The central investment question is no longer whether the playbook works, but whether SpaceX still has time to run it.

Anthropic entered an open field. Claude Code established coding as the wedge before an incumbent agent occupied the enterprise; Cowork then expanded into general knowledge work, while the orchestration graph compounded largely unnoticed. That two-year head start mattered more than raw capability.

SpaceX begins from a very different position. Cowork is already bundled into $20-a-month plans, ChatGPT Work arrives with OpenAI’s distribution behind it, and Microsoft is urging enterprises to build and retain their own learning loops rather than surrender them to an outside lab. SpaceX is therefore racing not only two established agents, but the enterprise itself.

Entanglement moats are granted, not seized, and they compound with deployment. Each week Sand remains unlaunched is another week in which rival agents accumulate context, history, and switching costs among the customers that SpaceX’s valuation assumes it will eventually win.

The week’s product news made the entanglement literal. Cursor’s own 3.11 release shipped side chats and searchable agent history: agent threads that persist, can be recalled and re-invoked, and index thousands of past transcripts locally - switching costs accruing to whoever owns the transcript layer. The moat is being productized in real time, at the exact layer this race is for.

The delay may be rational. Cursor still needs to be integrated into SpaceX’s product line, connected more deeply to Grok, and hardened for enterprise use. But that is the cruelty of the clock: the acquisition that creates the strategic advantage is consuming the one resource the playbook cannot recover - time. The next three to six months may determine whether Sand emerges as a credible general-purpose agent or remains confined to Cursor’s coding roots.

Trust is the other constraint. A vendor that holds the operating map of an enterprise becomes either the stickiest asset in software or an unacceptable liability. Grok 4.5’s measured hallucination rate rose to 54 % even as accuracy improved, while Cursor’s agent stack has already suffered publicly disclosed prompt-injection escapes. Its engineering beachhead is real, but the executives who grant access to email, spreadsheets, and core workflows sit elsewhere in the organization. Outside the Musk ecosystem, publicly disclosed enterprise adoption remains negligible. A captive customer is evidence of control, not demand.

So, either the wedge remains open, in which case speed, cost advantage, and an enterprise-grade Sand launched within quarters are decisive; or the window has already narrowed around incumbents bundled into products customers trust. What the valuation cannot reasonably assume is that a playbook requiring two uncontested years will yield on demand to a late entrant with an unshipped agent.

Where the search ends: the small bucket

Which returns the analysis to where the revenue always was, and to the part of SpaceX that deserves respect. The physical achievement is impressive: Colossus was built at a cadence no rival has demonstrated; the Terafab program could be on a path to TSMC-scale equipment spending by the end of the decade; and Starship, if the catch cadence holds, changes the deployment cost of compute in a way no terrestrial operator can answer.

Starship plus the compute-deployment cost advantage is the bull case that survives scrutiny: physical infrastructure at the bottom of the stack, not AI applications.

But value it for what it structurally is, because the structure contains a circularity that needs to be priced in. The anchor tenants are Anthropic, at roughly $1.25 billion per month, and Google, at roughly $920 million per month: the companies that own the application layer, which SpaceX’s own filing claims as its market.

SpaceX’s AI P&L is, as of today, a derivative of its competitors’ application-layer success.

If the labs’ application economics disappoint, scarcity is the first thing to deflate, on 90-day cancellable paper, at rates even the bulls assume are roughly halved. The earliest hard test of this valuation is therefore the first renewal on that 90-day paper, not anything orbital and not an agent launch.

That, in the end, is the verdict on the black hole, one month on.

Strip away the narrative, and what remains is one of the defining infrastructure businesses of the era: a vertically integrated compute utility with a physical cost advantage, circular tenancy, and rents likely to normalize over time. By SpaceX’s own arithmetic, that business addresses a $2.4 trillion opportunity, which represents just 9% of the story being sold.

Above it sits an option on Anthropic’s playbook: entered late, compressed into a shorter timetable, and pursued with a fourth-place model and an agent that has yet to ship into a market the original player already occupies. The option has real value. The stack is credible, the three-part advantage is tangible, and the catalysts are visible: earnings, the Cursor closing, a Sand launch decision, Grok 5, Composer 3.0, and the first major enterprise customer beyond the Musk ecosystem.

But an option priced as certainty is not an investment thesis.

DISCLAIMER: The views and opinions expressed here are those of the author alone and are based on publicly available information. They do not constitute investment advice, a solicitation, or a recommendation to buy or sell any security or financial instrument. The author may hold positions in the securities of companies mentioned. Past performance is not indicative of future results. Readers should conduct their own independent due diligence and consult a qualified financial advisor before making any investment decision.