Fermi's $16B Question: When Regulatory Arbitrage Meets AI Bubble Dynamics

Fermi raised $683M to build nuclear power for AI data centers. Our 31-page in-depth teardown applies the Durable Moat Growth methodology to separate bubble hype from discontinuity opportunity.

On Oct 1, a little-known company named Fermi debuted on the NASDAQ at $21 per share. Its shares jumped 19% to $25 per share. Structured as a real estate investment trust, or REIT, the Texas-based company that wants to build nuclear power to deliver energy for AI data centers saw its shares close at $32.53 on the first day of trading, giving it a valuation of almost $16 billion (as of October 6, at close).

Considering the company has no revenue, no products, and no customers, it is an extraordinary event even for these AI-frenetic times.

Today, I published an exclusive 31-page teardown for Decoding Discontinuity clients that applies our Durable Growth MoatTM methodology to Fermi’s business model. The result: 1.8/5 on our Durable Growth Moat™ framework, revealing how legitimate technological tailwinds create bubble conditions even when the underlying constraint is real.

The full report is available to Institutional subscribers or as a one-time purchase. Our analysis covers the analysis of Fermi’s financial fundamentals, single point of failures and, need to believes for moat realization, and proposes a valuation framework for this one-of-a kind asset.

However, there is one red-line element of the tear down that I want to share publicly here related to our analysis: Regulatory Arbitrage.

In the case of Fermi specifically, and the American AI industry more broadly, the strategic economic roadmap for scaling their ambitions is intersecting strongly with political and regulatory issues, in large part because the very nature of this AI wave faces physical constraints such as land, power, water, and government.

In other words, forces that traditional tech players have not had to bend to their will in order to succeed for most of the digital age.

Rather than offering some technical breakthrough, Fermi offers a strategy for regulatory arbitrage that it believes will allow it to radically accelerate development and construction of nuclear power the broader AI industry needs to scale. The entire AI ecosystem badly needs this to be true.

To be clear, my intent here is not to be political. Rather, I want to highlight in a dispassionate way the risks inherent in this approach, and unpack why investors might be so eager to place bets on a company that almost every headline has labeled “risky.”

At such moments of Discontinuity as the one we are experiencing with generative and agentic AI, that distinction may not be as clear-cut as it appears on the surface.

As I explored in The AI Multiplier: Why the Market is Correct on the Bubble and Still Missing the Discontinuity, distinguishing between “AI changes everything” and “therefore this specific bet succeeds” requires rigorous fundamental analysis that markets under euphoria systematically abandon.

Powering AI’s Future

Despite the massive numbers often cited, it may still be hard to fully comprehend the real scale of what AI leaders envision they need just in the U.S. and how transformative this will be.

Electricity demand in the U.S. is projected to rise by 25% by 2030 due to the growing use of artificial intelligence, according to Goldman Sachs. Yet, the power grid is struggling to keep pace, and most of the electricity consumed will continue to be generated from fossil fuels.

In Part I of my recent mini-series on compute, I noted:

“The recent revelation that Microsoft has committed $100 billion to AI infrastructure through 2027 includes a single data center in Wisconsin, which is supposed to be the ‘world’s most powerful AI datacenter’ per Microsoft. It is one of two data centers Microsoft is building in the state that will require a projected total of 3.9 gigawatts of power, which would be enough for 4.3 million homes. In a state with 2.82 million homes, that is extraordinary. And it illustrates the capital moats emerging.”

That is indeed a staggering amount of power. But then, consider what I wrote the next day in Part 2:

“OpenAI fired a massive salvo across the entire industry’s bow on Tuesday. First came the announcement that Nvidia will invest $100 billion in OpenAI, which will deploy 10 gigawatts of compute starting next year. Meanwhile, OpenAI, Oracle, and SoftBank disclosed that development of five new U.S. AI data center sites under their Stargate joint venture is running ahead of schedule, putting the partners on track to hit their target of 7 gigawatts of new compute capacity by the end of this year.”

That 10 gigawatts would require building the equivalent of 10 nuclear power plants. Already, the U.S. Department of Energy projects that data centers will consume between 6.7% and 12% of all US electricity by 2028, up from 4.4% in 2023.

That estimate already may be woefully out of date. Alex Heath reported at his news site Sources, that according to an internal OpenAI Slack message he obtained, CEO Sam Altman told staff that over the long term, he believed the company would need about 250 gigawatts of power, or roughly one quarter of the current U.S. energy grid.

My Two Tales of Compute analysis revealed that AI infrastructure faces a trilemma: power availability, speed to deployment, and cost structure. Optimize two; achieving all three requires infrastructure innovation.

Hyperscalers are hitting power walls. Microsoft is committed to restarting Three Mile Island. Amazon paid $650M for Talen’s nuclear campus. Meta signed $14B with CoreWeave just last week. Google disclosed in 2025 that power constraints limit AI training runs. These aren’t marketing exercises: they are strategic responses to genuine bottlenecks.

Grid interconnection queues average 3-5 years nationally, extending beyond six years in constrained markets. For companies planning AI deployments in 12–18-month cycles, utility timelines represent existential constraints. Traditional datacenter REITs like Digital Realty and Equinix, despite operational excellence, cannot solve this—they lease buildings and buy grid power, not generate electricity.

So, who is going to provide that power in time?

Enter Fermi.

Back To The AI Future

The AI infrastructure build-out has produced a “temporal paradox”.

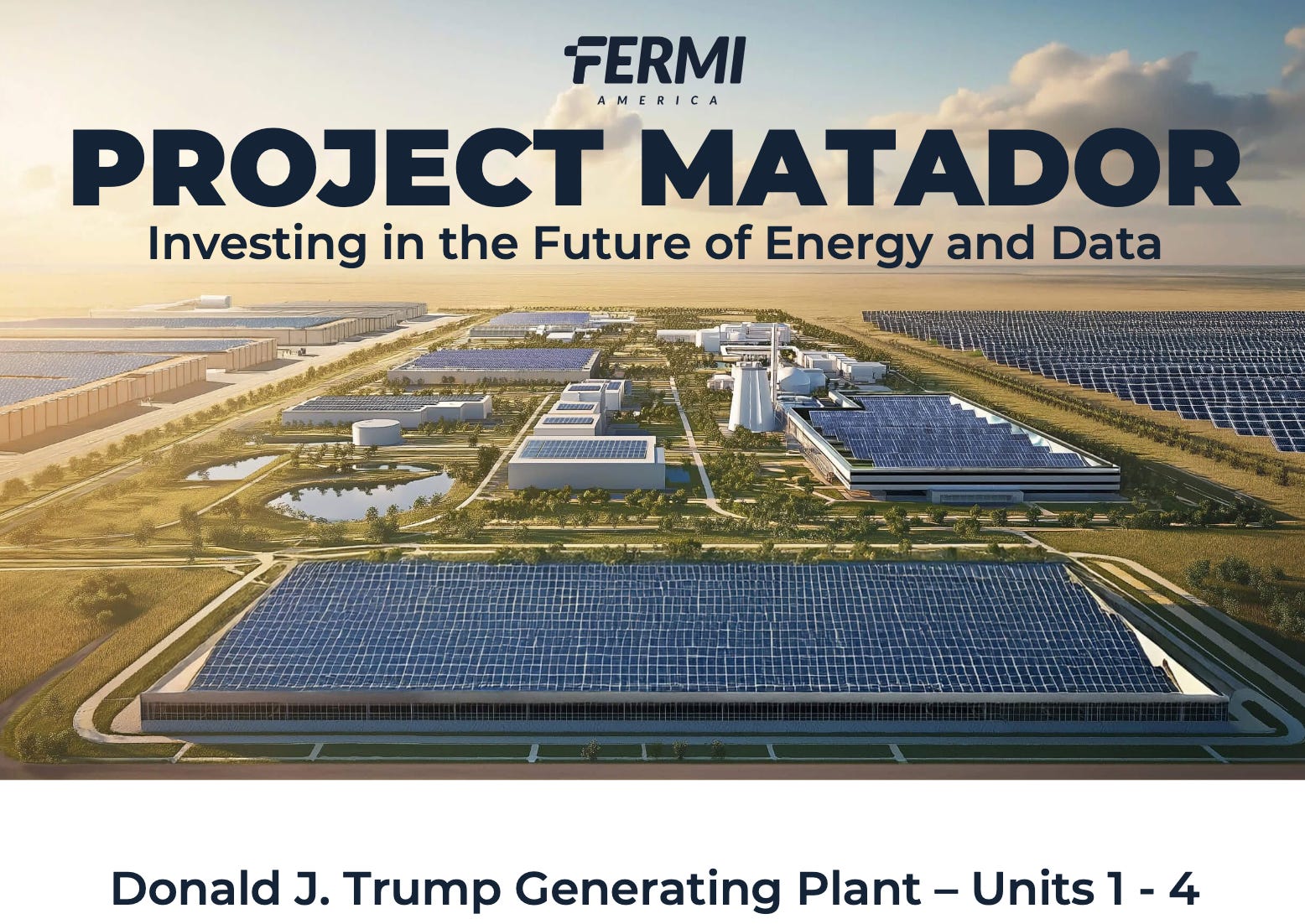

Fermi is proposing to use 1950s technology to solve 2025’s most cutting-edge problem—powering artificial intelligence at gigawatt scale. There has been a lot of innovation in the nuclear industry, including such promising technologies as small modular reactors. Fermi is not that, at least only partially (note: SMRs represent 1/3 of nuclear GW power the company projects by 2038).

Instead, Fermi is using the same basic design that powered Eisenhower-era atoms for peace for the frontier solution for training frontier models.

Formed in January 2025, the company intends to build “Project Matador,” an 11 GW integrated nuclear-gas-solar campus in Amarillo, Texas, anchored by four AP1000 reactors delivering ~4 GW of carbon-free baseload power to AI datacenters. It proposes behind-the-meter generation eliminates grid dependency with sixty-year operational life. In sum, it has an infrastructure ambition that makes even hyperscaler capex programs look modest.

It’s also a $50 billion, 15-year development program led by a team with unproven nuclear construction experience, targeting an industry that reinvents itself every 18 months, priced as though success is nearly certain rather than profoundly uncertain.

So why does this project have any credibility with investors?

First, it goes back to opportunity. There is no doubt that the demand will exist for anyone who can deliver. Rather, the question is: Can they deliver in time?

That is where things get more speculative. In this case, a tidal shift in the regulatory environment over the past year has convinced both investors and the founders of Fermi that the regulatory process that historically caused traditional nuclear projects to face huge delays and cost overruns can be dramatically compressed.

Fermi’s regulatory filing cites such measures as:

President Trump’s executive orders directing the Nuclear Regulatory Commission (NRC) to issue licensing decisions within ~18 months, which Fermi argues will compress a process that has often taken a decade or more.

The administration’s goal of getting “three new nuclear plants” to reach criticality as early as July 2026, positioning Fermi’s schedule as aligned with that policy push.

The orders also encourage siting reactors on federal lands and generally “modernizing” regulation.

In parallel, the NRC is piloting an applicant-prepared environmental document with Fermi, a measure Fermi highlighted as evidence it could speed-up approval process. Indeed, the NRC has already accepted initial portions of Fermi’s combined license application (COLA) for four AP1000 units in Project Matador, which Fermi points to as momentum under the new policy environment.

Finally, (and again, with no intention to be political here), it’s important to note that one of Fermi’s founders is Rick Perry, the former governor of Texas, a one-time presidential candidate, and a former U.S. Secretary of Energy during President Trump’s first term. Though it is not explicitly stated in the prospectus, clearly investors are betting Perry’s connections with the administration will help facilitate regulatory matters.

Indeed, on the official FERC application for Project Matador, Fermi now calls the facility: “the President Donald J. Trump Advanced Energy & Intelligence Campus.”

Evaluating The Discontinuity

The challenge then remains for investors: how to move beyond a gut decision and analyze such a business at such an embryonic stage?

In the case of the Durable Moat Growth score, the aggregate SPOF component score is 3.5/5. This reflects material execution risks characteristic of first-of-a-kind infrastructure development at unprecedented scale, balanced by mitigating factors.

There are several key factors that figure into that score:

The NRC pilot program participation may compress regulatory timelines, though Fermi remains the first civilian nuclear development adjacent to an active weapons facility, creating novel regulatory considerations.

Tennessee Valley Authority’s 6 GW SMR program announced in September 2025 provides regulatory momentum supporting compressed timelines relative to Vogtle. TVA’s BWRX-300 construction permit application targets 2032 commercial operation, representing a seven-year development timeline versus Vogtle’s thirteen years.

However, the national permitting and licensing is just a piece of the regulatory puzzle. There will be state boards (though Texas is considered to be quite favorable to such projects). Local boards. Water commissions that are increasingly sensitive to local backlash. In the case of Fermi, it could still face difficult challenges depending on how the IRS rules about various financial aspects of its business.

Then there is the financing. The IPO was a success, but to raise the larger debt needed to finance construction, Fermi will need to move through each phase of approval and demonstrate it achieves milestones to establish credibility with lenders and investors for each successive round. Of course, interest rates will always remain a wild card.

The 3.5/5 score reflects material execution challenges balanced by regulatory momentum and standardized design benefits.

If Fermi threads the needle and delivers, the returns could be huge. If it stumbles...

Consider the example of Georgia Power’s Vogtle Units 3 and 4, the only AP1000 reactors completed in the United States. They ultimately cost $35B against $14B budgets due to seven-year delays.

Should Fermi face similar delays, it could face $36B financing requirement beyond projections.

Fermi pursues a precarious sequence: raise capital at extraordinary valuation, execute unprecedented private nuclear development, and rely on sustained hyperscaler demand and capital market access throughout a 15-year buildout. This approach works only until it doesn’t—and when $50 billion infrastructure programs fail, consequences cascade through supply chains, capital markets, and regulatory frameworks in ways pure software failures never replicate. Stranded physical assets, creditor losses, and regulatory scrutiny create industry-wide contagion that no venture writedown produces.

The Constraint Is Real

Still, the energy bottleneck Fermi addresses exists.

The market recognizes this constraint’s value. Crusoe Energy achieved a reported $10B private valuation with proven operational capacity, deploying gas turbines in 18-24 months to serve AI workloads. The company demonstrates commercial viability for energy-integrated infrastructure.

Fermi positions itself as Crusoe’s nuclear evolution: longer development timeline, vastly higher capital intensity, but potentially superior economics through fuel diversification, carbon-free generation, and 60-year operational life versus 25-year gas turbines.

What makes Fermi instructive for understanding bubble dynamics is that the company’s challenges aren’t hypothetical bear-case scenarios. They’re base case realities anyone seriously analyzing nuclear infrastructure deployment must confront.

Can Fermi simultaneously represent a strategically sound response to AI’s power constraints AND a poor risk-adjusted investment at current valuation?

Yes. And understanding this distinction separates bubble participants from bubble survivors.

The lesson for institutional allocators isn’t “avoid AI infrastructure” but rather “demand evidence of milestone achievement commensurate with valuation.”

Successful execution at appropriate valuation creates wealth; successful execution at inflated valuation merely preserves capital. The gap between current market cap and probability-weighted fundamentals represents speculative premium investors are paying for option value on nuclear differentiation.

Yet, none of this justifies a $17.1B valuation for a nine-month-old company with zero customers and a 1.8/5 Durable Growth Moat™ score.

Identifying discontinuities creates wealth. Overpaying for exposure to those discontinuities destroys it. At its current valuation, Fermi tests whether markets can distinguish between the two. Because sometimes the best response to an exceptional idea is patience for an exceptional entry point.

The market will soon reveal whether investors can make this distinction. For now, Fermi stands as a $17.1B bet that regulatory arbitrage can overcome infrastructure physics.