SpaceX IPO: Why Enterprise AI is an $800B Black Hole in the $1.75 Trillion Story

The prospectus prices xAI for an enterprise market it has no visible path to capture beyond vague references to 'Macrohard.' It also undersells the consumer franchise that is actually its strength.

TL;DR: Today, we are publishing our “A Durable Growth Moat™ Assessment of the AI Segment of SpaceX - ‘AI’” for Institutional clients. In addition, we will be sending the executive summary to paid subscribers. While the SpaceX public offering represents a potentially historic IPO and has been widely scrutinized, our agentic frameworks offer a different analysis of the company’s structural position in the Agentic Era.

Let me start with a confession: there are many things about Elon Musk that I deeply admire.

The car industry scoffed at electric vehicles until Tesla turned them into a market. Reusable rockets were a fantasy until they were not. A satellite constellation large enough to blanket the planet was a slide deck until it had ten million subscribers. He builds physical things the rest of us had filed under “impossible”, and he builds them faster than anyone alive. When the SpaceX training cluster nicknamed Colossus came online in 122 days and its successor in 91 days, those were extraordinary feats of engineering.

A core pillar of my work is the thesis that generative and agentic AI have moved beyond disruption into Discontinuity, a clean break from the strategic, economic, and financial benchmarks that have governed the technology industry for decades. As I have argued in my work on Orchestration Economics, such moments present a fundamental human challenge: our brains are not wired for Discontinuity. Navigating it requires an act of abstraction: the ability to see how the pieces might eventually align, and what could be unleashed.

Musk’s mind seems singularly wired for exactly that. He can imagine things others cannot, and how to get them built. I am well aware of the criticisms of him, personal and professional. But in my role as a researcher and investor, it is my duty to look at the asset dispassionately. That same ability to navigate Discontinuity is precisely what I wrote about in my analysis of his Tesla pay package. So I brought the same mix of admiration and analytical rigor to the SpaceX S-1, one of the most audacious public offerings in history.

The company is a complex beast comprised of three parts. I am not here to give a granular read on the space business. As others have noted, it is a relatively small but intriguing operation that SpaceX insists will one day be far larger. I happen to believe that data centers in space, despite the technical difficulties, are a real possibility. Launch and Dragon are roughly break-even today, and Starship is still swallowing capital, but the option is real and large: a dominant, vertically integrated launch monopoly that also happens to be the on-ramp to orbital infrastructure carries serious optionality. You will have to take the company’s word for much of that. It is not my specialty.

The second part needs little from me. Starlink is a genuinely great business. It is the only GAAP-profitable segment of SpaceX; it grew roughly 50 percent last year to about $11.4bn; it serves more than ten million subscribers across more than 160 countries; and it throws off real operating cash. It has the signature of a compounder: recurring revenue, a widening moat, and a falling marginal cost per added subscriber. If you want to underwrite SpaceX, this is the anchor.

What I want to focus on is the other third: AI. A buyer of SPCX is underwriting a Starlink cash-flow compounder, a space option, and an AI bet, all at a single multiple of about 94 times revenue that Starlink cannot support alone. That AI thesis is the source of both the premium and the risk. And it is shouldering a far larger part of the valuation than most people realize, in a way that has almost entirely escaped notice.

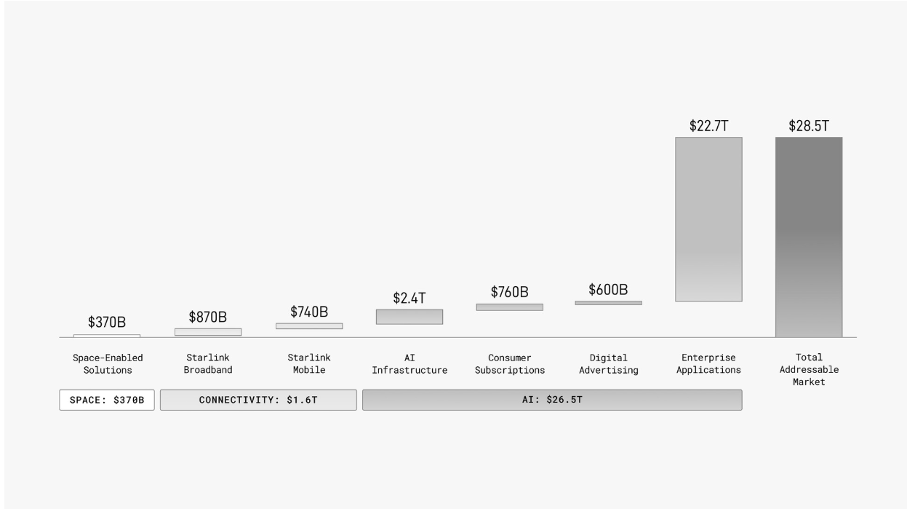

The S-1 sizes the AI opportunity at a $26.5tn total addressable market, of which $22.7tn – fully 86 percent – is labeled “enterprise applications.” It is not merely that this framing lifts the valuation above Starlink’s fundamentals. It assumes that SpaceX, xAI, or whatever the entity comes to be called, will effectively own the market for enterprise applications.

That would be an astonishing claim for any company. For this one, it is incongruous.

Just two months ago, Musk publicly declared that xAI “was not built right the first time around, and is being rebuilt from the foundations up.” The AI segment has no notable enterprise adoption. It has a potential enterprise product whose current status is murky, at best. And the prospectus makes no attempt to explain how the company will achieve this colossal victory.

In effect, the enterprise story is a giant black hole at the center of the prospectus.

What makes the magical thinking even stranger is that, while reaching for the enterprise prize it has not earned, SpaceX is underselling two assets it actually has: the consumer side of its AI business and its option to acquire Cursor. These might only partially fill the valuation chasm. But it is telling that the company did not even make the case.

By now, the world understands that this IPO is as much a referendum on Musk as a market judgment. Even so, with OpenAI’s listing approaching and Anthropic’s prospectus filed, it is worth trying to put some rational analysis back into the discourse.

The lens

My approach at Decoding Discontinuity is built on a simple premise: the old economic paradigm has been gutted, and a new one, Orchestration Economics, is only just taking shape. Because we do not yet know its full form, the analysis cannot rely on traditional metrics such as this year’s cash flow or the price-to-earnings ratio.

What matters more, for a frontier business, is its structural position in a value chain that is still forming. When you invest today, you are buying that position because it determines whether the business sits at the node where value is eventually captured. Capture is not guaranteed, which is precisely why the position is best understood as an option.

I set out the full thesis in my Manifesto. In an agentic economy, the value of abundant intelligence does not accrue to whoever owns the most compute, or even to whoever trains the best model. It is governed by three laws: value flows to whoever sits closest to intent – closest to where the work begins, where the context lives, and where the workflow is controlled.

I made this case at length last week in King Claude: The Orchestration Moat in Operation, my study of Anthropic, which has emerged as the king of the first agentic cycle. In my framework, Anthropic is an orchestrator, not because it owns the most GPUs – it rents them, including, as it happens, from the very company we are discussing – but because it earned a position inside the enterprise. It entered through a Coding Wedge, accumulated proximity to how real companies do real work, and only then, seriously, worried about compute. That sequence turned the LLM race upside down, carrying Anthropic from a perceived also-ran behind OpenAI to a dominant force that outran its own projections.

There is an irony here: Anthropic may have been helped, in the short term, by xAI’s own struggle to convert the Colossus build-out into a comparable advantage. But the point that matters is that Anthropic secured its structural position almost a year ago. The leverage only became visible later, as the benefits compounded. That is why understanding where SpaceX and xAI stand in the AI race requires more than model benchmarks. They understate how far behind xAI has fallen. Structurally, xAI is effectively starting over.

What the S-1 actually argues

Take xAI’s theory one step at a time, as the prospectus presents it.

Step one: we will control compute, the binding bottleneck of the agentic economy.

Step two: we will control data through X.

Step three: combine the two, and we capture the output.

That output is defined as an AI market of $26.5tn, of which $22.7tn – 86 percent – is “enterprise applications.”

Two inputs and an asserted output. So what connects them? I went looking for the mechanism, the actual bridge from “we own the compute and the data” to “we capture the enterprise”. To my surprise, I could not find it in the document.

What I found instead was a reference to Macrohard, the product that Musk has been talking about in somewhat vague but grandiose terms since last Fall. “Our goal is to create a company that can do anything short of manufacturing physical objects directly, but will be able to do so indirectly, much like Apple has other companies manufacture their phones,” he wrote on X in October 2025.

“Macrohard” is Musk’s riposte to “Microsoft.” (“MACROHARD, the much stronger AI equivalent of that other software company!” as Musk put it.) To emphasize his ambitions for this project, he had the name painted on the roof of the Colossus II data center so it could be seen from space.

That is the whole game. Macrohard, in theory, then carries a large portion of the SpaceX valuation. Considering that it’s unclear that it even exists is problematic to say the least.

So, to evaluate SpaceX's AI component, let me take the three steps in turn.

Step one: compute is not the moat

The entire industry is scrambling for silicon and power, and SpaceX may be the one player capable of making itself genuinely compute-unconstrained through cluster-build velocity, prospective in-house silicon, in-house energy, and, eventually, the wild card of orbital compute riding its own rockets beyond terrestrial power limits. If even two of those four vectors compound, the AI segment owns a structural cost advantage in an inference-heavy economy. That is a valuable business; I credit it, and in my scoring, the compute layer comes out modestly positive on its own merits.

But “unconstrained” is not the same as “uniquely positioned.” Being able to make compute cheaply tells you nothing about whether you capture the enterprise application sitting four layers up the stack. Compute is table stakes for the race; it is not the prize at the finish line.

There is no sharper illustration than the Anthropic deal. As the filing discloses, the single largest AI contract on the books is the rental of the flagship cluster – to a direct frontier-model competitor – at $1.25bn a month, terminable on 90 days’ notice, and explicitly framed as monetizing “unused compute capacity”. Sit with that. The clearest revenue the AI segment can point to is the sale of its scarcest asset to the company that has already won the position SpaceX says it will win. The orchestration laggard is being paid by the orchestration leader. The value chain is telling you which way it runs.

Step two: the model is a follower

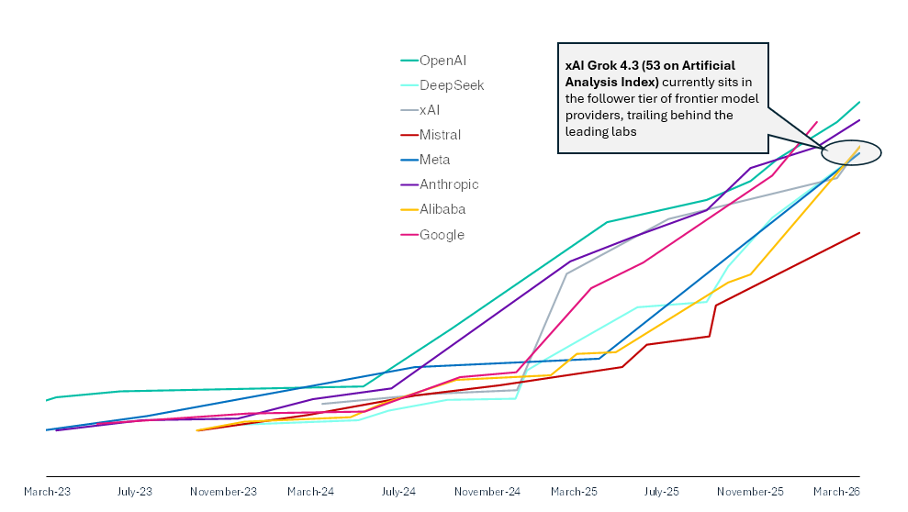

The second input is the model, and here the news is respectable rather than decisive. On the independent Artificial Analysis Intelligence Index, Grok 4.3 scores 53, a serious model, comfortably above the median. But the frontier sits at 57-61, held by Claude Opus 4.8, GPT-5.5, Claude Opus 4.7, and Gemini 3.1 Pro.

Grok is a capable fast-follower, and in places it shines: on agentic tool-calling, it is excellent, posting 98 percent on the τ²-Bench customer-support benchmark and a large jump on real-world agentic tasks. The harness is well-built; the plumbing is ready.

Two things still keep it from being a moat. First, the model layer is commoditizing. Grok’s genuinely unique data asset is the X firehose: some 350mn posts a day, fed into the model in real time. But that buys freshness and relevance for a consumer; it does not buy a training edge that lifts the model above the field, nor a context advantage that compounds inside an enterprise. The data makes Grok a better companion for “what is happening right now”. It does not make Grok a better system of record for Salesforce's sales pipeline model.

Second, and the market has not fully priced this, there is the pressure from below. The most interesting models of the past year in coding and orchestration are neither Western nor closed. They cost a fraction of the incumbents, as little as one-thirtieth on some workloads; they are free to run; and they attack precisely the agentic-coding domain that is meant to be the AI segment’s wedge. When good-enough intelligence is open and nearly free, the premium on owning a closed mid-frontier model does not flow up to the model owner. It flows to whoever holds the orchestration layer. Which brings us to the only question that matters.

Step three: the orchestration test

Let’s come back to Macrohard. Ideally, this would be the product I would put to the test to determine the company’s true structural position. However, as I noted, there appears to be nothing to evaluate.

A recent description of the project came from Musk on March 11:

“Macrohard or Digital Optimus is a joint xAI-Tesla project, coming as part of Tesla’s investment agreement with xAI. Grok is the master conductor/navigator with deep understanding of the world to direct digital Optimus, which is processing and actioning the past 5 secs of real-time computer screen video and keyboard/mouse actions. Grok is like a much more advanced and sophisticated version of turn-by-turn navigation software. You can think of it as Digital Optimus AI being System 1 (instinctive part of the mind) and Grok being System 2. (thinking part of the mind). This will run very competitively on the super low cost Tesla AI4 ($650) paired with relatively frugal use of the much more expensive xAI Nvidia hardware. And it will be the only real-time smart AI system. This is a big deal. In principle, it is capable of emulating the function of entire companies. That is why the program is called MACROHARD, a funny reference to Microsoft. No other company can yet do this.”

Of course, the next day, Musk publicly declared that xAI had been built all wrong and would need to be completely rebuilt. In the S-1, the disclosures on Macrohard seem far from promising.

The prospectus describes it as an “AI platform designed to be capable of fully emulating digital workflows and augmenting human operation of computers using sophisticated autonomous agents. We believe Macrohard will have the potential to fundamentally transform how companies are structured and operate, thereby allowing dramatic increases in human productivity.” However, the prospectus also notes that the project, which is a collaboration with Musk’s Tesla, is in the “very early stages, as a result of which we and Tesla have not finalized a variety of details relating to our collaboration, including, but not limited to, financial terms, intellectual property rights, and the ultimate term of our collaboration.”

So, all we can do is evaluate what actually exists.

I built the Architectural Resilience Assessment Framework (ARAF™) to take the next step beyond the three laws: to turn structural analysis into a score, and a score into an investment signal. At a high level, ARAF weighs two opposing forces across several dimensions – Opportunity and Risk. For SpaceX, it says the following.

The AI segment scores as a positioned agentic asset. It owns its model, which makes it structurally immune to the consolidation risk that hollows out application-layer “wrappers”; it captures intent at genuine consumer scale; and it holds a data asset no competitor can replicate. That is a real starting point, an interesting one.

But positioned is not strong. In my reading, the orchestration position is good, not strong, because the intent it captures is consumer rather than enterprise. Grok is not the surface where professional work begins; it is not embedded where the work happens, as the enterprise products that are winning are. One asset could change that: Cursor. But it is rented, not owned, and, for now, confined to code. I will come back to it, because it is the single most important thing in the entire AI story.

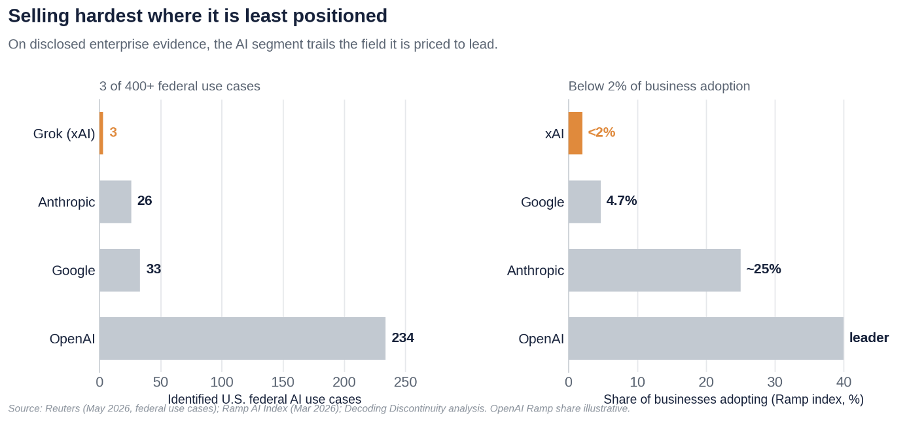

The workflow layer – where the $22.7tn lives – is the thinnest. To capture “enterprise applications” at scale is to contest the systems of record: Salesforce, ServiceNow, Workday, and SAP. These are not mere databases; they are the encoded business logic of how a company runs: the approval chains, the validation rules, and the configuration history. These form the ground truth against which any agent must be verified as correct. The $22.7tn is not greenfield. Even the orchestration leader does not replace these systems; it orchestrates around them. The AI segment holds neither that cross-vertical role nor that context, and its enterprise standing is further weighed down by an unresolved set of safety and regulatory questions – data-protection inquiries, litigation, and doubts over its standing in government procurement – that bear directly on the regulated accounts where mission-critical work would otherwise accrue.

The proof is in the adoption data. Independent trackers put the segment below 2% of business usage. Grok appears in just three of more than 400 identified federal use cases. Anthropic’s enterprise share is around 40 percent. The reality is plain: xAI is a consumer-and-data position trying to pass itself off as an enterprise play.

The case for optimism

SpaceX does not make a clear bull case for its AI, so I will. There are two genuine upsides, though even together they would not fill the gap to the enterprise number the company has imagined.

The first returns to structural position, Anthropic, and the coding wedge. The coding wedge is the proven route into the enterprise, and Cursor is that wedge in its purest form: the environment where millions of developers express professional intent every working day. Now add the part that the market keeps underrating. The future of enterprise AI is model-agnostic. No serious company will stake its operations on a single model; what it wants is an orchestration layer that routes each task to the best-suited model and abstracts the model away. Value migrates to that layer – to the interface, not the engine. And that is exactly the move that neutralizes the AI segment’s biggest weakness: own the model-agnostic interface, and you no longer need Grok to be the best model anywhere. You hold the orchestration position whichever model wins the week.

This is why Cursor is potentially the hinge of the whole story. xAI holds an option to acquire it. Exercise that option and you could – could – assemble three things no rival can put in one place: the proven, model-agnostic coding wedge into the enterprise; a real-time data engine to feed it; and effectively unlimited, low-cost compute to run it. That is the only credible bridge I can draw from “we own the inputs” to “we capture the enterprise”. It is the single biggest option in the filing, and the one I would tell any prospective investor to study hardest.

And yet it is thick with uncertainty. The option is unexercised and code-only today, and it carries a tension the bull must look at squarely: a model-agnostic interface owned by a model-maker invites a conflict of interest. Why would Anthropic or OpenAI leave their models routable inside a platform that a direct competitor controls? Neutrality is the asset; ownership threatens it. So the unlock is real but conditional. Only if the segment exercises Cursor, generalizes it beyond code, and keeps it credibly open – while feeding it data and compute no one else has – does the enterprise prize stop being a slogan and start becoming a position.

The second upside is X’s consumer strength. ARAF rates the AI segment as good but not strong, largely thanks to Grok’s consumer-intent capture, its data moat, and the immunity conferred by owning its own model. In fact, the same analysis suggests the filing may underweight the value of consumer engagement, an asset no competitor can replicate. The real-time X corpus and a Grok surface of roughly 117 million monthly users create a genuine, unique-data-backed franchise, with digital advertising as upside still to be demonstrated.

Instead, the company is selling hardest exactly where it is least positioned – enterprise – and underselling where its assets actually translate – consumer. That mismatch is the surprise. There can be more than one winner at multiple layers of the stack: Anthropic can own the enterprise orchestration layer, while the AI segment holds a formidable consumer-and-infrastructure position. These are different strengths. Projecting a vast enterprise figure with no evidence behind it is, to put it gently, a curious choice.

The price

Even granting all the optionality I am happy to grant, the numbers ask for more than the assets support. Build the company from its parts.

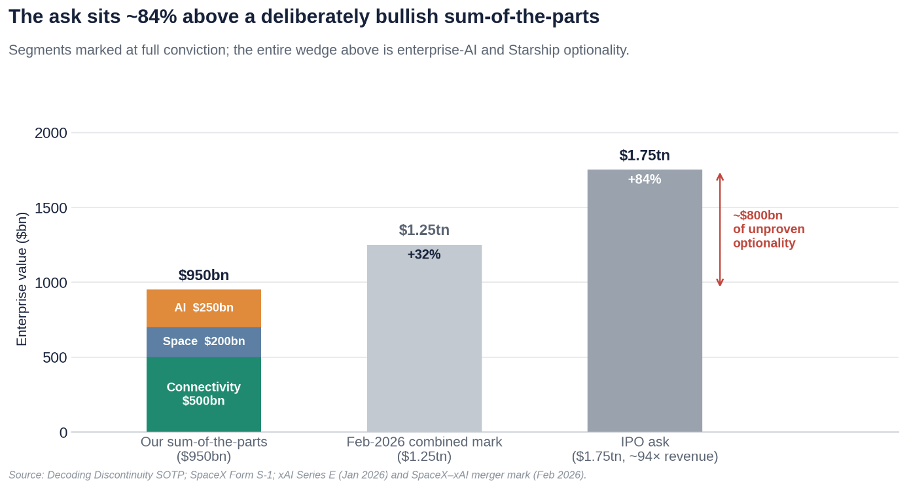

Starlink is the verified anchor and roughly half the defensible value: I mark it at about $500bn. Add Space as a dominance premium for the launch monopoly, with Starship as honest optionality, at about $200bn. Value the AI segment at about $250bn: I take xAI’s last private round at roughly $230bn, already a rich mark, comfortably above Anthropic and OpenAI on a revenue basis, as the worth of the lab itself, and add its neocloud compute-rental business at about $20bn.

Do that with a generous hand, and you reach a fundamental base of roughly $950bn. The combined private market is about $1.25tn. The IPO ask is about $1.75tn – some 94 times trailing revenue, the largest offering in history, with Goldman Sachs as lead underwriter and a listing under SPCX on 12 June.

My practical guidance is therefore simple. Underwrite SPCX on Starlink, which you can verify. Value the AI segment on what is real today – its consumer, data, and compute businesses – not the enterprise prize it has not earned. And model the $22.7tn at zero: not because it is impossible, but because nothing in the filing yet earns a positive number. That will change only when specific, watchable thresholds are crossed: a Grok that decisively leads; a Cursor that is owned and generalizing beyond code; named enterprise deployments integrated with the systems of record; adoption that climbs off the floor. Cross these thresholds and I will happily re-rate.

Until then, the IPO is asking you to pre-pay for a vision the company cannot yet articulate. Many will do exactly that. The absence of an enterprise rationale ought to be a red flag. But, like any black hole, the one at the center of this prospectus will likely exert a gravitational pull that draws investors in regardless.

The views and opinions expressed in this Website are those of the author alone and are based on publicly available information. The expressed views and opinions do not constitute investment advice, a solicitation, or a recommendation to buy or sell any security or financial instrument.

The author may hold positions in the securities of companies mentioned. Certain companies referenced may be current or former clients of, or counterparties to, the author or affiliated entities; such relationships will be disclosed where applicable.

Past performance is not indicative of future results. To the fullest extent permitted by applicable law, the author does not accept any liability for any loss or damage arising from reliance on this content. Readers should conduct their own independent due diligence and consult a qualified financial advisor before making any investment decision.

The author maintains no current position in Anthropic, SpaceX, or any private entity discussed.