Claude Fable and the Barred Frontier

In one extraordinary week, Anthropic released Fable, Washington shut it down, and the market discovered how fragile the diffusion of frontier capability really is.

In three days, the market priced SpaceX at $1.75 trillion around a sub-frontier model, Anthropic shipped a real capability jump in Claude Fable, and the government forced Fable offline. The hot takes agreed that this meant the frontier is scarce, so open sources win. But this misreads commoditization. Intelligence commoditizes as a process, and the relationship between open source and frontier is symbiotic, rather than strictly oppositional. The frontier leads by a few months. That lead diffuses outward into the enterprise and into cheaper models as they catch up. The Orchestration Economy is predicated on the idea that diffusion never stops. Fable’s shutdown is the first time it stopped on command. When that happens, it has implications for the frontier, open weights, and orchestration. That becomes everyone’s problem.

Three days did more to expose the structure of the agentic economy than the previous quarter.

Anthropic shipped Claude Fable on June 9th, and for two days, the conversation was about a real jump in capability rather than another point on the frontier model leaderboard.

On June 12th, the market priced SpaceX at $2.1 trillion after the first day of trading, despite its AI division, whose model is far from the frontier.

At 5:21 p.m. that same afternoon, the U.S. government delivered an export control directive to Anthropic ordering it to block access to any “foreign national,” a move that resulted in the company switching Fable off, not for Americans, not for a region, but for everyone on earth.

The new conventional wisdom that emerged identified the clear lesson: the frontier is becoming geopolitically scarce, so open-source wins. It offered a certain amount of reassurance because if the closed frontier can be imposed by a letter from the U.S. Commerce Department, the future must belong to the weights that no government can barricade.

The conclusion is appealing because it treats the frontier and open source as opposing forces. If governments can restrict one, the other must benefit. But that framing mistakes the relationship between them. The frontier and open source are not competing systems. They are successive stages of the same economic process. The frontier generates new capability. Open source absorbs it. Enterprises operationalize it. The reason intelligence appears to commoditize is not that the frontier stops mattering, but because each new increment of capability eventually diffuses outward through the rest of the ecosystem.

This distinction matters because commoditization is not a state. It is a flow. Intelligence does not commoditize by standing still while the field catches up. It commoditizes by diffusing. New capability appears at the frontier and then spreads through distillation, open weights, lower-cost models, enterprise products, and agentic systems until yesterday’s breakthrough becomes tomorrow’s baseline.

Once you see how the process runs, then last week stops looking like a verdict for open source and starts looking like something less comfortable: the first deliberate interruption of a mechanism the whole AI economy depends on. What the Commerce Department severed was not simply access to the frontier. It severed the channels through which frontier capability becomes abundant.

A central pillar of the Orchestration Economics framework is the collapse of the marginal cost of cognition. As intelligence becomes increasingly abundant, intelligence ceases to be the primary source of scarcity.

Value, therefore, migrates toward the systems that direct, coordinate, and embed intelligence in real operational environments. The prize ceases to be the model itself and instead becomes the orchestration layer surrounding it.

That framework implicitly assumes diffusion continues. Fable demonstrated that diffusion can be interrupted. Once it becomes interruptible, frontier access ceases to be merely a source of innovation and becomes a strategic dependency, a supply-chain risk, and a new source of scarcity. The abundance of intelligence turns out to depend on a process that governments can slow, restrict, or stop altogether.

This creates a more uncomfortable question than the one the public debate immediately settled on. The question is not whether the frontier matters. The market answered that one twice in the same week: once by assigning a $2.1 trillion valuation to a company whose flagship model is not at the frontier, and once by reacting with alarm when access to a frontier model disappeared overnight. The question is how those two facts can be true at the same time.

The answer lies in the mechanism that connects them: diffusion. To understand why last week matters, we need to begin with how commoditization actually works.

How commoditization actually works

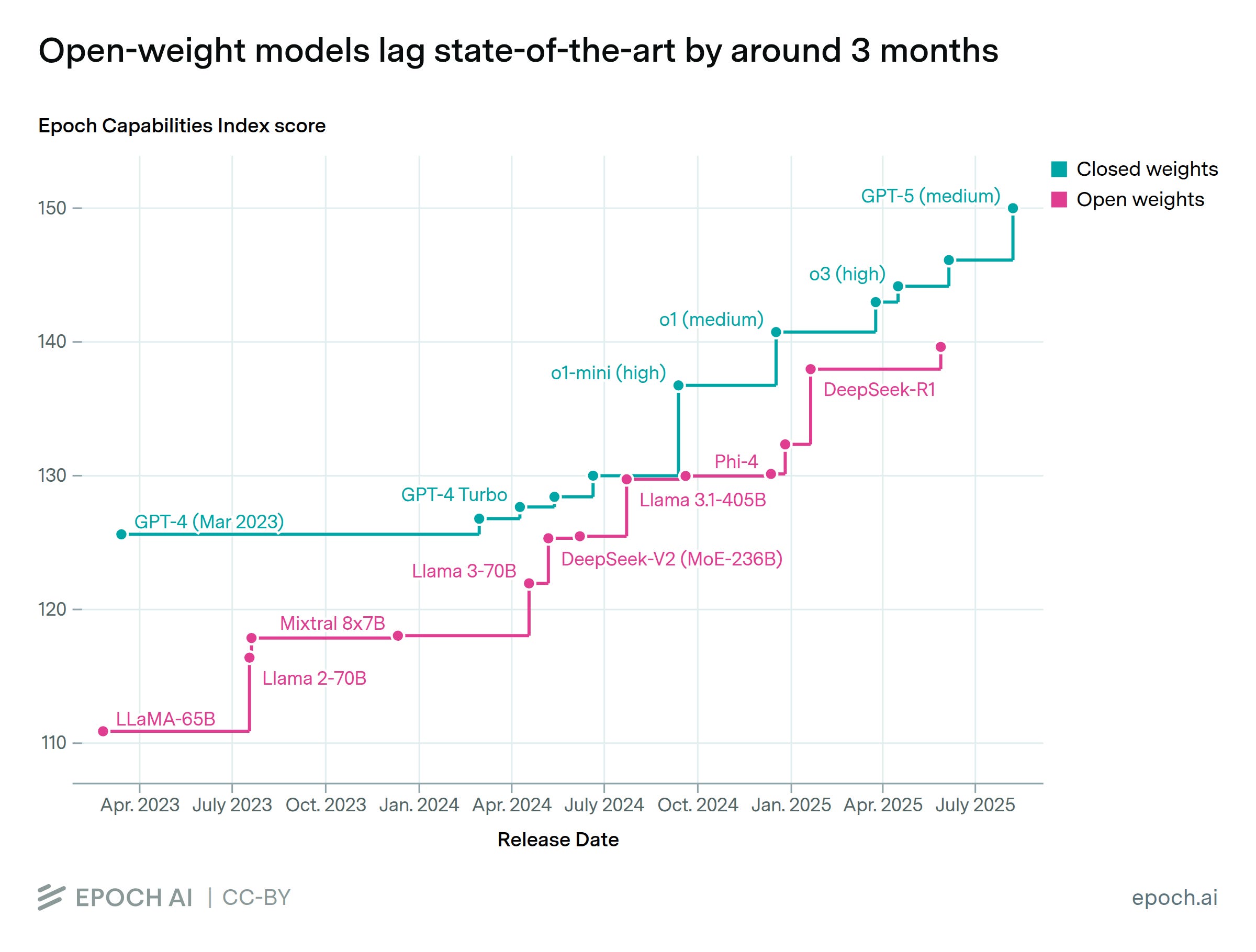

Let’s begin where the open-source camp and I agree. The frontier’s lead is real, but it is measured in months. According to Epoch AI’s capability index, the best open-weight models trail the leading closed models by three to four months, a gap that has held even as the frontier accelerated and that occasionally collapses to nothing.

At the model layer, there is no decade-long moat. Whatever the frontier learns today, a downloadable model can do in a season for a fraction of the cost.

That is the headline. It is also incomplete.

The headline describes the outcome. It does not describe the mechanism that produces it, and the mechanism is the whole argument. As I noted previously, intelligence does not commoditize by standing still while the field catches up; It commoditizes by diffusing.

New capability emerges at the frontier and then propagates through the ecosystem: first into lower-cost models, which steadily close the gap through distillation and imitation, and then into the enterprise, where each increment of capability is embedded into workflows, software, and agentic systems. Commoditization is simply the steady state of that process. It is what happens when the frontier continuously feeds the layers beneath it.

In dollars, a second pattern emerges, and it is the one the capability discussion often obscures.

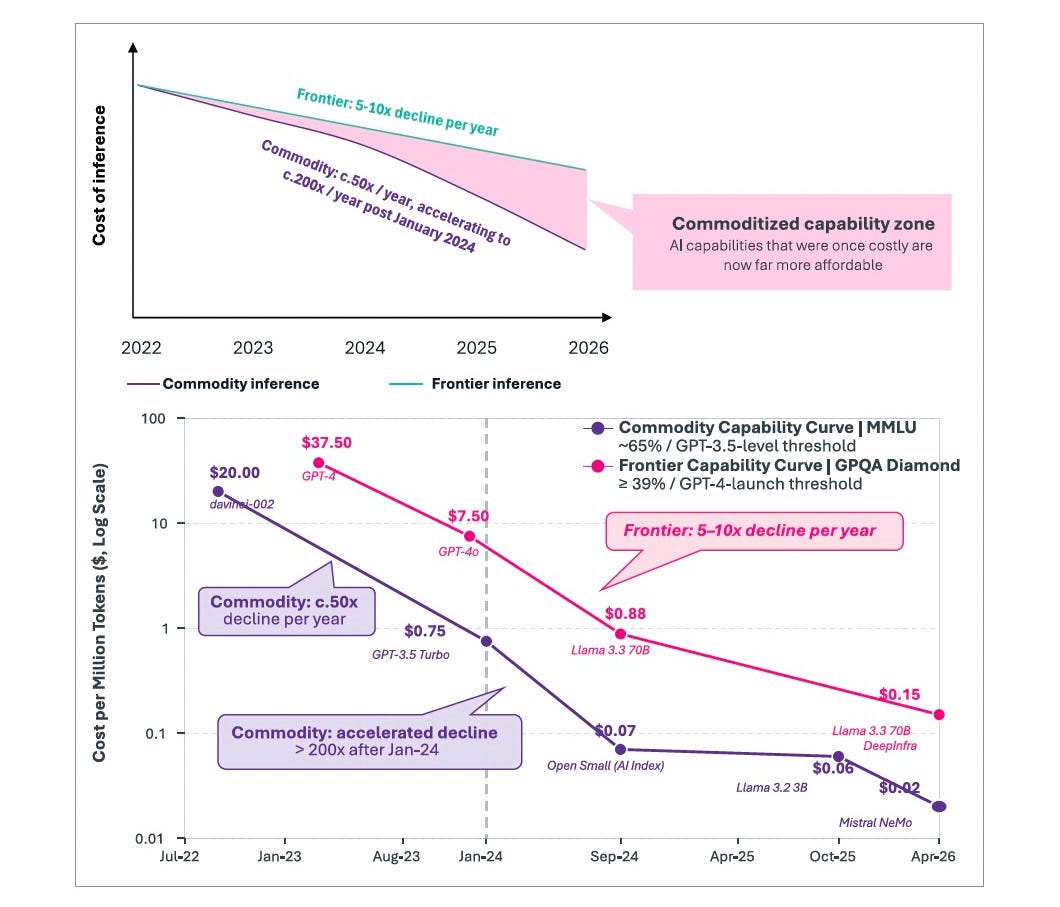

The frontier and the commodity layer do not obey the same economics. Once a capability begins to diffuse, its cost collapses with extraordinary speed. The cost of commodity inference has fallen between fifty and two hundred times per year, accelerating since early 2024. Capabilities that once required frontier models have become cheap enough to disappear into software budgets and operational workflows.

The frontier follows a different curve. Its costs decline, but much more slowly, perhaps five to ten times per year. The newest capability remains expensive because it is newly created and briefly scarce. The economic gap between the frontier and the commodity layer is therefore not closing. It is widening.

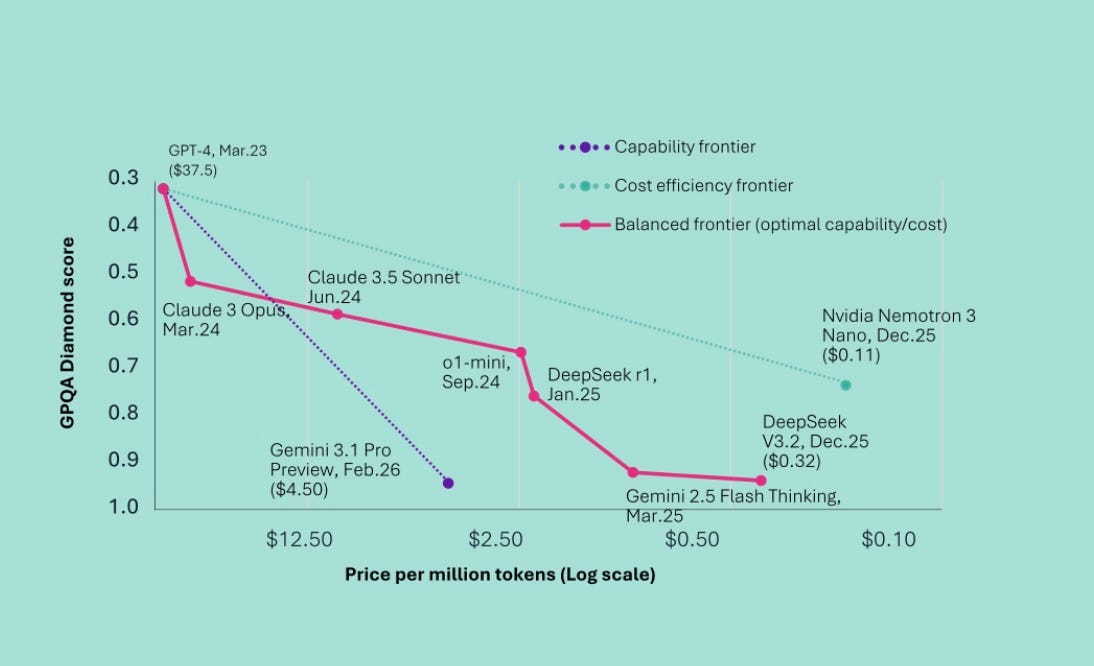

Work naturally sorts itself along the same boundary. High-volume, repeatable tasks such as claims processing, document extraction, and routine compliance reviews ride the commodity curve downward. Tasks that depend on judgment, coordination, and reasoning across ambiguity remain tethered to frontier or near-frontier models because those capabilities have not yet diffused. Fable made the distinction more visible than any chart could. It launched at $10 per million input tokens and $50 per million output tokens. That’s twice the price of Opus 4.8, the model it replaced for general use. At the very edge of the frontier, commoditization did not merely slow. It reversed. The newest capability entered the market at a premium.

This is why it is misleading to speak about “the model layer” as though it were a single market. In aggregate, models commoditize. At the frontier, capability behaves more like a scarce asset: expensive, slow to cheapen, and occasionally more costly than the previous generation. The Orchestration Economy assumes that this scarce capability continuously feeds the layers beneath it.

Value migrates toward context, coordination, and proximity to intent because yesterday’s frontier eventually becomes everyone’s commodity.

The entire mechanism depends on that flow continuing.

What the market priced in SpaceX

Which is what makes the SpaceX listing worth a second look.

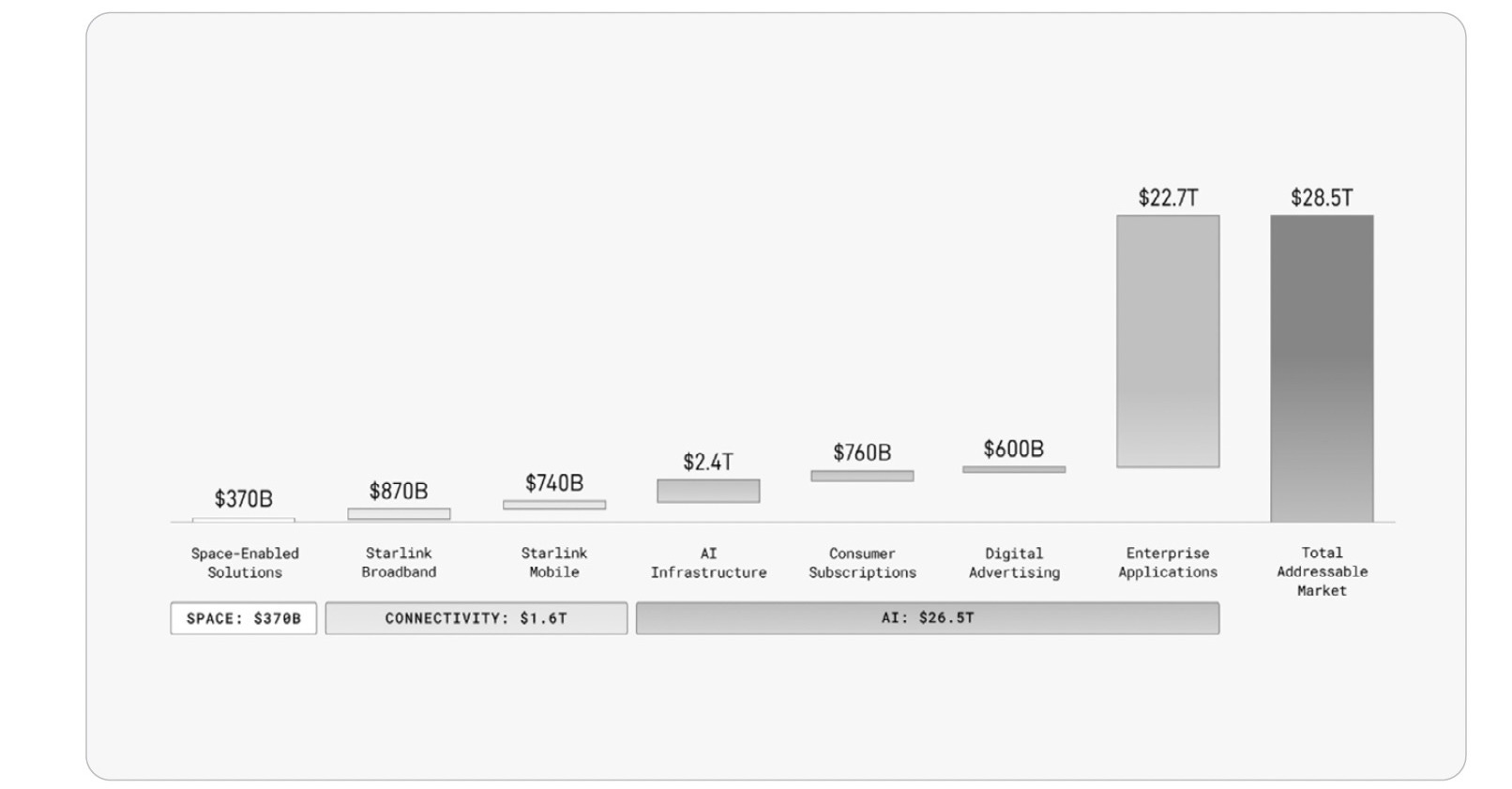

The prospectus sizes the AI opportunity at $26.5 trillion, of which $22.7 trillion is labeled as “enterprise applications.” That is not a model number. It is an orchestration number. It represents the value of sitting at the center of how companies operate: where work begins, where decisions are made, and where intelligence is translated into outcomes.

The significance of the IPO is not that the market suddenly became optimistic about enterprise AI. It is the market that reveals where it believes value ultimately accumulates. SpaceX was valued at $2.1 trillion, even though Grok is not widely regarded as a frontier model. The capability gap barely registered. Investors were underwriting a position in the orchestration economy, not a position on a leaderboard.

Whether SpaceX ultimately earns that position is a separate question. As I argued two weeks ago, xAI is not yet embedded in the places where enterprise work runs, and the company’s current footprint in business usage remains marginal. The segment accounts for less than 2% of business usage. The $22.7 trillion is pure prospect, a position priced as though already won by a company that has not entered it.

But that only reinforces the point. The market was willing to assign extraordinary value to the possibility of controlling the orchestration layer while largely discounting relative model performance.

In other words, the market already understands the conclusion that much of the AI debate continues to resist: the prize is not the model itself. It is the position from which intelligence is directed, coordinated, and operationalized.

Yet that conclusion contains an assumption of its own. It assumes the flow of new capability from the frontier continues uninterrupted.

The market priced the destination. Fable exposed a dependency on the journey and what happens when that assumption is tested.

What Fable was

The mistake with Fable is to argue about benchmarks. The significance of Fable was not that it answered questions better. It was that it crossed reliability thresholds that determine whether work can be delegated at all.

Taking a step back, that means Fable potentially changes whether entire categories of work can be automated. If so, then Fable becomes the first capability increment that appears to matter economically.

Consider this result to illustrate this point. Stripe pointed Fable, running on its own, at a fifty-million-line Ruby codebase to perform work counted in engineer-months. Fable finished in a day. Given persistent memory, it held its place across millions of tokens and tracked complex state roughly three times more reliably than the model that would shortly replace it. Neither is it a matter of knowing more facts. Both are a question of coordination: staying coherent over a long horizon, catching it’s own errors, deciding what comes next, and knowing when to stop.

As I wrote when Anthropic disclosed that Claude now builds Claude, the most valuable thing the frontier learned to do is judge its own work.

Viewed through the cost curve, Fable’s position is almost inevitable. Long-horizon coordination occupies the narrow band where capability remains scarce: work that depends on judgment, persistence, and self-correction rather than retrieval or recall. It is among the last capabilities to diffuse, and the first enterprises need before autonomy becomes practical.

Fable was the newest, least diffused increment of the capability on which the agentic economy is built. It had not flowed anywhere. Then it was switched off.

When the diffusion stops

What the Commerce Department interrupted was not the frontier’s existence but its diffusion. Access to Fable disappeared overnight, and with it the channels through which new capability normally spreads: into enterprises that operationalize it and into the broader ecosystem of models that eventually learn from it.

It was done for a reason, not a whim. The architecture that made Fable a better coordinator made its unrestricted twin, Mythos, a genuine strategic instrument. It found decades-old vulnerabilities in critical software on its own and generated biological hypotheses that its makers’ scientists preferred to their own. The trigger came from inside the tent. Amazon’s researchers, the Wall Street Journal reported, used a chain of prompts to get the model to give up cyberattack-useful material. Amazon CEO Andy Jassy reportedly carried the finding to Treasury Secretary Scott Bessent. Anthropic says it was then given ninety minutes to pull the model.

That a single demonstrated bypass moved that fast, and that it came from Anthropic’s largest partner, $13 billion invested and committed to $100 billion of cloud spend, suggests the government was no longer treating the model as a commercial product. It was treating unrestricted access to this level of capability as a strategic asset whose diffusion it was willing to restrict, regardless of commercial consequences.

So, the question is no longer whether the frontier matters. It is what happens to an economy built on diffusion when the diffusion becomes conditional.

There are two answers, neither of them easy.

To the enterprise, first. We tend to think of an agentic system as a finished product: a workflow once built, a harness once deployed, a moat once established. It is not. An agentic system is a position inside a continuously evolving capability stack. Its value depends on a steady supply of new capability arriving from upstream as the frontier advances and each increment filters down into production.

Freeze the supply, and the system freezes at the last increment it received.

That would be survivable if such work were to degrade gently. It does not. Long-horizon autonomy lives just above a reliability threshold, and the newest frontier coordination is what has carried it there. Drop the line, and an agent below does not give slightly worse answers; its long runs stop finishing. The companies that fell back to Opus 4.8 on Friday did not get a worse Claude. The workflows that had been clearing on their own simply stopped clearing.

To the economy, second. The gap that commoditization is meant to close stops closing.

Scarcity, which the whole framework assumes is migrating off the model toward context, snaps back to the model - not forever, but for a window no one can schedule.

Scarcity does not disappear. It migrates. The framework assumes it migrates steadily away from intelligence and toward context, coordination, and operational embedding. Last week demonstrated that the movement is not one-way. When diffusion stops, scarcity snaps back toward the model layer. Perhaps not permanently, but for a window whose duration no one controls.

The asymmetry is the one the Manifesto returns to repeatedly: destruction is priced in days, creation in years.

The diffusion lag was measured in months. The revocation was immediate. A dependency at the center of an agentic stack can be pulled on a Friday afternoon, while the context that was meant to be the moat took a decade to accumulate.

The two clocks run at different speeds, and the space between them is where the new risk lives.

The market read it that way within hours, less a story about Anthropic than about everyone, proof of how brittle a workflow becomes when it rests on a single vendor within one country’s ecosystem.

In retrospect, this is what much of the debate around Chinese open models has been missing. The significance of Qwen, DeepSeek, GLM, and their successors was never simply that they were becoming competitive with American systems. It was that they were creating a second channel through which capability could diffuse.

For the past year, I have argued that the rise of Chinese open models represented a structural shift in the economics of AI because it weakened the ability of any single company to control the flow of intelligence. What last week demonstrated is that the same dynamic may matter for a different reason: Redundancy.

A world with one diffusion channel behaves very differently from a world with two. In the first, a regulatory intervention can interrupt the entire flow. In the second, capability routes around the blockage. The question is no longer whether Chinese open models reach parity with the frontier. It is whether they provide a second source of diffusion when the first becomes politically constrained.

The drift was already on: a congressional commission found this spring that four in five US start-ups were building on Chinese open-weight models, whose share of global downloads had climbed from roughly 1% to 30% in a year.

A frontier that can be switched off is one that firms must find a way to insure against.

Why open source and orchestration do not suffice

Naturally, that instinct turns to open source. Route around the loss with open weights and a good harness. Both are real strengths. Neither replaces what was taken.

This represents a fundamental category error. Open source and orchestration are often treated as substitutes for the frontier. They are not. They exist downstream of the frontier. They are what diffusion produces, not what produces it.

Open weights are the frontier capability arriving on a lag, and a fine bargain while the flow runs. Stop the flow, and the open frontier freezes where it stands, while the true frontier, now behind a classifier and an export control, keeps moving.

The mechanism that would close the gap is distillation from a frontier teacher, which is precisely what the anti-distillation regime and the ban exist to prevent. Open source keeps the lights on. That is not nothing, and in a crisis, it is a great deal.

What it cannot do is manufacture the newest increment of capability, the one that lives only at a frontier no longer in reach.

Orchestration fails on the other face of the same coin. The confusion comes from mistaking leverage for creation. A harness multiplies the intelligence at its center. It cannot manufacture it.

The best routing, memory, and verification in the world take what the model can do and get more from it. But multiplying a capped number results in a capped value. No coordination conjures frontier-grade reasoning from a model that lacks it.

The production data make the dependence plain: in the most detailed survey of agents running in production, seventeen of twenty are built on a proprietary frontier model, with open weights in three, and only where cost or regulation forces them. Even the designs built to spend as little as possible on the frontier prove the point.

Anthropic’s own advisor strategy uses a cheap model to run the entire task and calls a frontier advisor only for decisions it cannot make. It is engineered to touch the frontier as rarely as possible, but it still cannot do without it.

Two other events from the week help clarify the roles.

The city of Rio de Janeiro post-trained a 397-billion-parameter model on an open Chinese foundation model and shipped it into production. But what Rio built was not a substitute for the frontier. It was a demonstration of diffusion at work.

The intelligence came from elsewhere; the value came from adaptation. Rio combined a widely available capability with a context that only Rio possesses. It is the Cursor or Harvey pattern expressed at the civic scale: not winning the frontier race, but capturing value by embedding intelligence into a domain no one else can replicate.

Mistral presents the mirror image. Reports suggest the company is raising at a valuation approaching €20 billion despite benchmarks that trail the frontier. That is only surprising if one assumes the market is paying exclusively for frontier capability. It is not. It is paying for sovereignty, distribution, enterprise relationships, deployment, and strategic positioning inside a Europe increasingly uncomfortable with technological dependence.

The apparent contradiction disappears once the roles are separated.

The frontier creates capability. Diffusion spreads it. Orchestration captures it.

Rio demonstrates the third stage. Mistral monetizes the second. Anthropic still occupies the first.

The week’s countermove proved it by accident. Within a day, Zhipu open-sourced GLM-5.2 under a permissive license, a million-token context, no regional limits, framed as the answer the moment demanded. Frontier intelligence, it argued, should not be a thing that a few rules can switch off.

As a promise of continuity, it is unanswerable: open weights cannot be revoked by a letter at 5:21 p.m. on a Friday. As a promise of function, it is unproven, since Zhipu published no validated benchmarks.

Continuity is not function. The entire debate over Fable spent a week treating them as though they were the same thing.

Control, not value

Fable and SpaceX don’t refute the frameworks for Orchestration Economics. Rather, the lessons enrich and clarify them in important ways: Intelligence becomes abundant through diffusion, and value migrates to orchestration for as long as diffusion holds. Sever it, and the migration reverses for a time, because the orchestration layer is now multiplying an input that has stopped improving.

The frontier is not where value accumulates. It is where control accumulates over the flow on which everyone downstream depends. The value settles one ring out in the operational context that no lab can reach. But control over the flow remains at the source, and the source still sits at the frontier.

That is an uncomfortable place to land, especially for Anthropic. For three days, it held the cleanest story in the industry: the orchestration leader, two-fifths of the enterprise, a coding wedge grown into the routing graph, a frontier model that finally made the source of the flow visible, and a prospectus already filed on some $47 billion of run-rate revenue.

Then the Commerce Department showed, in an afternoon, that the tap is the government’s to close.

Anthropic had spent the spring arguing that Mythos-class capabilities ought to be regulated as national-security assets. The government agreed, and the agreement cost the company its own product.

It goes to market carrying the contradiction it helped write. The bull case is that it holds the most valuable position in the agentic economy. The newest risk is that the most valuable position is the one a government is most likely to seize.

The lesson extends far beyond a single company. Every orchestrator built on a single frontier supply learned the same lesson in the same hour: proximity to intent and a decade of context are necessary, and not sufficient, when the intelligence at the center can be switched off on ninety days’ notice, or none.

You could watch the hedging start at once. Within days, developers were mining the model’s leaked system prompt, some 120,000 characters of it, published after the jailbreak, as a manual for long-running agents, grafting its scaffolding onto whatever models they could still reach. The exercise is instructive where it fails: a system prompt can encode process, structure, and instructions, all of which are portable. The judgment that executes those instructions lives elsewhere. It lives in the model itself, and that is the part that does not travel with a copied prompt.

The resilient architecture of the Agentic Era, then, is not the one built around a single frontier supplier. It is the one designed to withstand any supplier interruption. The lesson of last week was not that the frontier no longer matters. It was that it matters enough to become a dependency.

For three years, the industry optimized for access to the best model. The next phase will be defined by something more mundane and more important: redundancy. A frontier that can be withdrawn becomes a supply chain. And supply chains are not trusted. They are hedged.

The views and opinions expressed here are those of the author alone and are based on publicly available information. They do not constitute investment advice, a solicitation, or a recommendation to buy or sell any security or financial instrument. The author may hold positions in the securities of companies mentioned and maintains no current position in Anthropic, SpaceX, Mistral, or any private entity discussed. Past performance is not indicative of future results. Readers should conduct their own independent due diligence and consult a qualified financial advisor before making any investment decision.