King Claude: The Orchestration Moat in Operation

How Anthropic came to rule the first agentic cycle and what it will take to keep the throne.

TL; DR

The king. Anthropic was worth $61.5 billion at Series E in March 2025. It is closing approximately $50 billion of primary capital at a post-money valuation of roughly $900 billion in May 2026. The Wall Street Journal reports that Anthropic is on track for its first profitable quarter in Q2 2026, with $559 million in operating profit on $10.9 billion in revenue, implying a 5.1% operating margin. The SpaceX S-1, filed May 20, 2026, disclosed that Anthropic could pay xAI up to $40 billion through May 2029 for the full 300 megawatts of capacity at the Colossus I data center and has an agreement for capacity at Colossus II. By every operational and financial measure, Anthropic is king of the first agentic cycle.

The thesis. The trillion-dollar question now: can Anthropic defend the throne? Its success rests on its ability to successfully do three things simultaneously: leverage its current position at the Harness layer to win the orchestrator role, the position at the center of the agentic enterprise IT stack; maintain the overall rapid pace of adoption; and avoid three potential Single Points of Failure. I will explore each of these factors in depth using the frameworks and methodologies outlined in AGNT: The Orchestration Economics Manifesto.

How it got there. Context matters, so we must first understand the conditions that fueled Anthropic’s stunning rise to dominance. Last year, when I argued that the AI race would not be won at the model layer but at the orchestration layer, that position seemed like an outlier, and Anthropic was valued at $61.5 billion. Now, this is almost a consensus, and yet it is still often poorly understood how Anthropic built its agentic orchestration moat.

What $900 billion requires. The mark is 30x against $30 billion of annualized revenue. Against the May 22, 2026 hyperscaler comparables (Alphabet 11.1x, Microsoft 8.7x, Meta 7.2x), Anthropic looks expensive; against the only other private frontier lab at scale (OpenAI ~35x at $852 billion / ~$24 billion), Anthropic is the cheaper of the two. The bull case prices Anthropic on a trajectory to enter the mature hyperscaler cohort, which requires revenue to roughly triple to a ~$90 billion annualized run rate and for the multiple to compress to ~10x, into Alphabet-adjacent territory. The 80x YoY revenue growth disclosed for Q1 2026 leaves substantial deceleration headroom inside that envelope. Plausible. Not yet earned.

A narrative ahead of reality? For the first time in this cycle, Anthropic’s narrative may be running ahead of its valuation rather than behind it. The architecture has been validated. The execution evidence is partial. The three conditions hold today. The next eighteen months will produce the evidence on whether the moat is genuinely durable or whether the king’s throne is more contestable than the priced reality currently suggests.

During the early, intoxicating dot-com years, it was common to hear someone say that one year in internet time felt like seven years in the real world. The accelerated Agentic Era has further compressed that sense of time. Now, one month feels like seven years.

Which is why turning the clock back to just May 2025 somehow feels like reaching back to another, distant era. But as we stand on the cusp of what may be the three most consequential IPOs in the history of the technology industry, it’s essential that we understand the pivotal events of the past twelve months that shattered conventional wisdom

Put aside benchmarks and valuations for a moment. In late May 2025, the consensus was that OpenAI had become a juggernaut, dominating consumer markets, mindshare, press, and awareness. It has raised billions more. It had the splashy infrastructure announcements made from the White House. Everyone else was gasping for air and relevance.

A May 2025 report by multi-model platform Poe suggested Anthropic had lost ground to OpenAI since January 2025 in terms of model quality and market share.

“Owning that segment not only locks out rivals, but also gives a long-term advantage in terms of revenue and the ability to invest in future models,” Ben Thompson of Stratechery wrote in June 2025 of OpenAI, while noting that Anthropic’s bet on “coding is a riskier position in some respects.”

Flash forward to the present day. The Agentic World has been turned upside down.

Now, Anthropic is such a force that it can drop niche plugins and wipe out billions in market cap on stock markets. It rolls out new products that extend its functionality both horizontally and vertically at a relentless pace. The company’s latest model, Mythos, is reported to be so powerful that it has spooked businesses and governments around the world. Anthropic is growing at an unprecedented pace and outstripping its own projections, so much so that it struck a deal to lease compute from former rival xAI, essentially making it one of the biggest pieces of SpaceX’s business.

This reversal of fortunes has left even the most astute observers struggling to fully explain Anthropic’s momentum. This is natural because they are turning to old frameworks in search of answers. What they are not recognizing is that generative and agentic AI have created a Discontinuity, not just a disruption, that requires making a clean break with past ideas, playbooks, models, and frameworks.

That’s why understanding how Anthropic got here is more than just a history lesson or a walk down Agentic Memory Lane. The why is essential to decoding the nature of the Agentic Era, both what matters now and what will continue to matter in the coming months and years as the new paradigm of Orchestration Economics continues to take shape.

Almost a year ago, while the world was still obsessed with model benchmarks, I began arguing that the real race was not for the most intelligent model. It was for the layer above intelligence: the layer that decomposes goals, delegates to specialist agents, manages state, and accumulates cross-system understanding across sessions. I called it the “Orchestration Layer” or “Harness “in the first essay of the Agentic Era series and argued that the moat would accrue to whoever built it.

Anthropic established a structural position in the enterprise via coding, which I dubbed the “Coding Wedge.” From there, it used that structural position to learn how to deploy and orchestrate agents at an accelerated rate. That advantage began to compound exponentially to the point where it became visible earlier this year, and suddenly, Anthropic had been transformed into an unstoppable force.

Nonetheless, we are still early in the deployment of agentic fleets, and Anthropic has yet to establish itself in the enterprise beyond an API provider, albeit a dominant one, and to demonstrate that it can occupy the seat of the “Orchestrator,” the strategic position by which an actor receives a human intent, orchestrates a series of agentic workflows to execute it so as to produce a business outcome. Orchestration is a complex architectural construct in the enterprise and, in my view, is the foundation for building a moat and durable growth in the Agentic Era.

I want to break from my usual newsletter format this week to do two things. First, at this critical juncture, I wanted to review what I had written over the past year and assess what I had gotten right and where I had missed the mark. The new rules of Orchestration Economics are still emerging, and it’s essential that we be willing to test all assumptions and theories against the reality that develops. And second, I want to use this essay to view these ideas and frameworks from Anthropic's perspective and examine the nature of its architectural moat in depth to illuminate how these dynamics are shaping the Agentic Era.

The Context

Anthropic was valued at $61.5 billion when it raised its Series E in March 2025. The investment debate among institutional allocators at the time was whether Claude 3.7 had a measurable benchmark advantage over GPT-4o and Gemini 2.5, an argument whose answer rotated week to week within a five-point band. The investment thesis on frontier labs was straightforward: pay for the model that wins on the benchmarks.

Twelve months later, Anthropic is closing a round of approximately $50 billion at a post-money valuation of roughly $900 billion. Its success in coding became a springboard for winning the enterprise. Any notion that consumer mindshare would translate to back-office adoption has faded from memory.

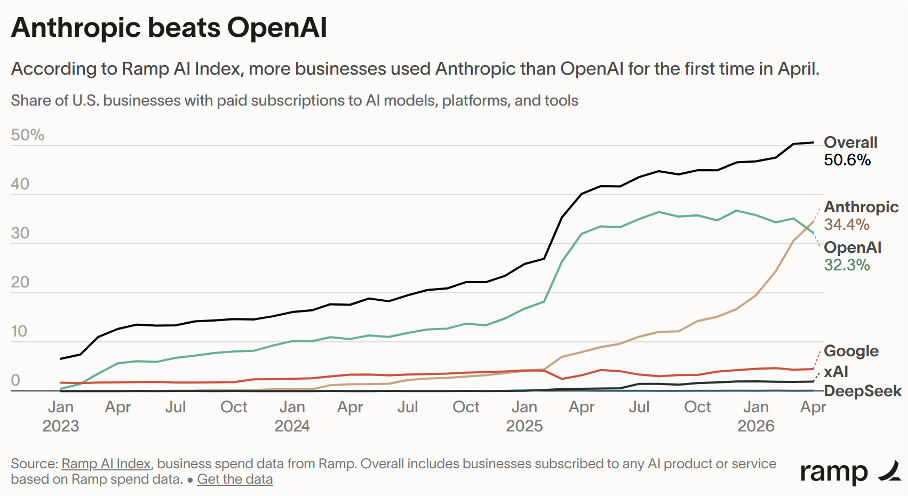

Independent enterprise trackers confirm the leadership shift. Menlo Ventures’ 2025 State of Generative AI in the Enterprise report, released in December 2025, found that Anthropic captured 40% of enterprise LLM API spend, compared with 27% for OpenAI and 21% for Google. Anthropic’s share was up from 24% the prior year, and OpenAI's was down from 50% in 2023.

The Ramp AI Index, released in May 2026, drawing on transaction data from more than 50,000 US businesses, recorded Anthropic surpassing OpenAI in business adoption for the first time: 34.4% of businesses paying for Anthropic versus 32.3% for OpenAI, with Anthropic having quadrupled its business adoption year over year while OpenAI grew 0.3%.

Facing a potential compute crunch, Anthropic made a shocking deal with xAI. According to the SpaceX prospectus filed on May 20, 2026, Anthropic will pay xAI $1.25 billion per month through May 2029 for the full 300 megawatts of Colossus 1. The architectural inversion is now in the public record: the company that built the largest speculative GPU cluster of the cycle has become the supplier to the company that solved enterprise demand.

Even now, the classic benchmarks can muddy this picture.

Consider one apparent counter-signal: Microsoft and OpenAI leading the narrower agent-orchestration-platform metric in recent enterprise surveys (Copilot Studio/Azure at 38.6%, OpenAI Assistants at 25.7%, Anthropic at 5.7% in VentureBeat’s Feb 2026 tracker). However, this sits at a different layer than the model-spend race. Microsoft’s lead is largely a distribution artifact of the M365/Azure estate; OpenAI’s standalone share is real but materially below its model-API position.

The model-and-spend layer (Menlo 40%, Ramp 34.4%) is Anthropic versus a catching-up field; the orchestration control plane is a separate, still-contested layer where Microsoft’s tenant-level distribution is the structural incumbency to beat.

That also explains Anthropic’s recent product direction: Claude Managed Agents, Agent Skills, shared Excel and PowerPoint context, and the Copilot Cowork partnership with Microsoft all point toward the same strategic objective: ownership of the orchestration layer itself. Anthropic is clearly treating orchestration as a contested frontier, one that is far from settled.

What gives us a clearer picture of Anthropic’s ascendancy is the financial information that has been publicly disclosed so far:

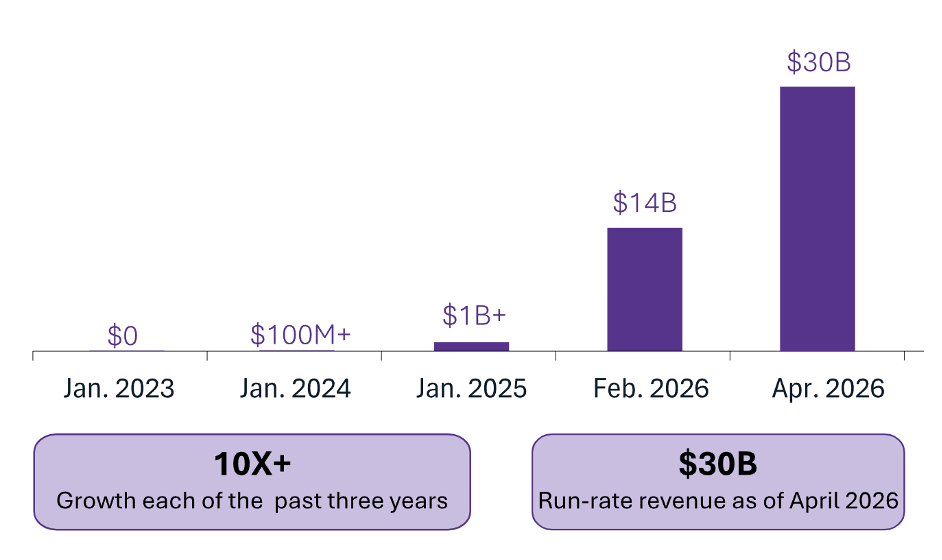

Revenue trajectory. Anthropic’s annualized run-rate grew from approximately $1 billion in late 2024 to $9 billion at the end of 2025, to $14 billion at the Series G announcement on February 12, 2026, $19 billion in March, and to approximately $30 billion in April 2026.

Anthropic’s Series G announcement framed this as approximately 10x annual revenue growth in each of the prior three years. CEO Dario Amodei told VentureBeat that Q1 2026 growth represented 80x year-over-year, exceeding the company’s own internal projection by a factor of eight. The Q1 2026 revenue, per The Wall Street Journal, was $4.8 billion, and the outlet also reported that Q2 2026 is on track for $10.9 billion in quarterly revenue and a projected $559 million in operating profit for Anthropic.

Margin direction. The Q2 2026 5.1% operating margin contrasts with OpenAI’s Q1 2026 operating margin of approximately negative 122%. Anthropic’s margin trajectory is visible in three public dimensions:

Each Sonnet release has improved inference economics measurably over its predecessor, with pricing-versus-capability gains disclosed at launch.

The hyperscaler compute deployments, most notably Google TPU for first-party workloads, produce favorable unit economics that Anthropic has attributed to architectural fit.

The progressive mix shift toward higher-margin first-party enterprise revenue relative to API-reseller volume is evident in the disclosed enterprise customer counts. API and product growth. At the Series G announcement, Anthropic disclosed that Claude Code had reached an ARR of $2.5 billion, more than double since the start of 2026, with weekly active users also doubling in the same period. Approximately 4% of all public GitHub commits worldwide are being authored by Claude Code, twice the figure of one month prior.

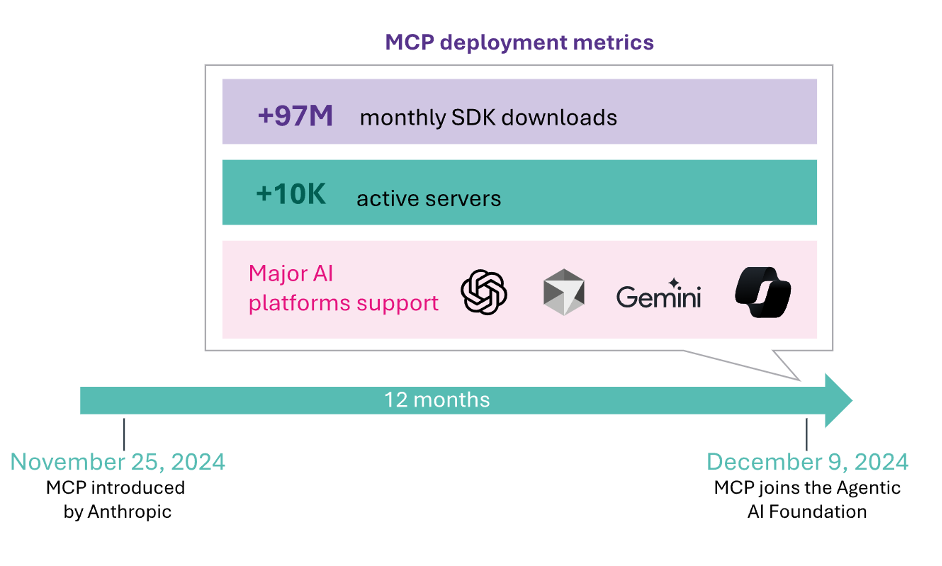

Business subscriptions to Claude Code quadrupled in two months. Enterprise use represents more than half of Claude Code's revenue. The Bedrock customer count crossed 100,000 in April 2026. Customers spending more than $1 million annually crossed 1,000, doubling in two months. Eight of the Fortune 10 and 70% of the Fortune 100 are now Claude customers. MCP downloads exceeded 97 million per month, per Anthropic’s March 2026 disclosure.

Compute commitments. The public disclosures resolve into two distinct stacks. Equity into Anthropic from compute partners of approximately $80 billion, including:

AWS up to $25 billion

Google up to $40 billion ($10 billion cash plus $30 billion milestone-contingent)

Microsoft $5 billion

NVIDIA up to $10 billion

Anthropic’s disclosed compute commitments total approximately $400 billion across the cited term lengths, plus 1 GW of reserved NVIDIA Grace Blackwell / Vera Rubin capacity not separately priced:

AWS, more than $100 billion over ten years alongside 5 gigawatts of Trainium2/Trainium3 capacity;

Google, approximately $200 billion over five years alongside 5 gigawatts of TPU capacity arriving in 2027;

Microsoft Azure, $30 billion;

Fluidstack, $50 billion for custom Texas and New York data centers;

Add to this Anthropic's participation as one of the AI lab signatories to the Department of Energy MOUs under the Genesis Mission executive order of November 24, 2025, which lists nuclear fission and fusion among its priority scientific domains. Then the SpaceX S-1 disclosure ($40 billion through May 2029).

This last item is approximately $15 billion in annualized compute payments recorded on the income statement, against $30 billion in current annualized revenue. That’s about half of the revenue committed to a single supplier, which is also Anthropic’s most direct competitor in frontier models.

These numbers describe the king’s throne and the moat he has attempted to build around it. The architectural question remains: what will be required to defend it?

Act I - May 2025: The bet on orchestration

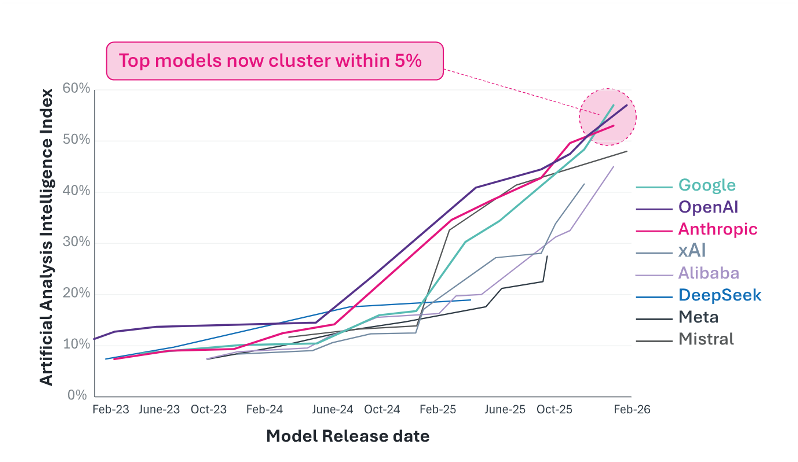

The dominant investment thesis among institutional allocators in May 2025 was that the AI race would be won at the model layer. Several labs clustered within 5 percentage points across every standardized evaluation: MMLU-Pro, GPQA-Diamond, Humanity’s Last Exam, and the latest iteration of SWE-Bench. The leaderboard rotated every six to eight weeks. No frontier lab held a sustained, measurable performance edge.

My reading of those benchmarks deviated from the consensus. The cluster was the signal. When three or four labs converge within measurement-error bands on every standardized evaluation, and when the leaderboard order rotates faster than the publication cycle of those evaluations, the most likely interpretation is not that someone is winning. It is that intelligence had commoditized.

I argued in the May 2 essay that durable value would accrue not to the lab with the highest benchmark scores but to the lab that controlled the coordination layer between commoditized intelligence and enterprise context. I listed four mechanical advantages required to build it:

connection protocols that standardize how models reach external systems;

agent frameworks that guide multi-stage reasoning;

tool-integration systems that extend model capability through specialized services;

interface design patterns that translate raw intelligence into intuitive user experiences.

The first of the four was the most important. Anthropic launched the Model Context Protocol (MCP) in November 2024. By Q2 2025, OpenAI and Google had both adopted it as a standard for connecting their models to external systems. By May 2025, the protocol war was effectively decided. But the consensus continued to frame the competition as Claude versus GPT-4o versus Gemini.

I argued that Anthropic had set the connection standard for the entire cycle and would capture value from every integration built on top. In retrospect, I was partially right and partially exposed.

Setting an open standard is not the same as monopolizing the value of that standard. Open protocols are, by definition, public utilities. TCP/IP did not enrich its authors. MCP’s universal adoption solves the connection problem at the layer above the model and below the application. But in doing so, it commoditizes the protocol layer itself. Value can leak in two directions from a commoditized protocol: downward, to whichever model performs best inside the coordination envelope; or upward, to whoever owns the distribution surface that aggregates user intent.

The protocol owner’s claim to value depends on holding either the model layer beneath or the distribution layer above. Holding the protocol alone is insufficient. In May 2025, the thesis was that Anthropic would control both. So far, that thesis has held.

At the time of publication, Anthropic was valued at $61.5 billion, while OpenAI stood at nearly $300 billion. My argument was that this gap would narrow as the market came to understand what Anthropic was actually building. This ran against both prevailing valuation assumptions and the analytical consensus underpinning them.

Act II - July 2025: The compute bottleneck

Two months later, Google revised its FY2025 capital expenditure plan mid-quarter from $75 billion to $85 billion. The disclosed reason was a $106 billion backlog in demand for cloud services. The day before, OpenAI committed to $30 billion per year in cloud infrastructure spending with Oracle, about 3x OpenAI’s then-$10 billion run rate and approximately 1.2x Oracle’s entire fiscal-2025 cloud business.

Compute had moved from a procurement question to a strategic survival question for every frontier lab.

I published Compute Access: The Single Point of Failure Redefining Strategic Advantage on July 29, 2025. The argument: the Harness is only as durable as the silicon its operator can secure. The lab that owns the coordination layer, without the compute to support its growth, surrenders the moat to whoever can. Orchestration is where value accrues. Compute is what prevents the accrual.

But it’s not just compute. A year ago, when the focus was still on model benchmarks, compute was synonymous with training frontier models and was discussed in the abstract. But this would inevitably change, as I tried to signal in a series of articles in the summer of 2025 exploring the training-versus-inference distinction: Two Tales of Compute: Decoding the Infrastructure of AI Economics and Two Tales of Compute: The Battle for AI’s Operational Future. Having access to compute would be critical. But having access to the right kind of compute would also matter.

By Q1 2026, the compute topic dominated hyperscaler earnings calls. By Q2 2026, it had produced the structural arrangement I had not specifically predicted but had named generically: Anthropic, locked out of sufficient owned capacity by the speed of its own growth, would lease compute from a competitor’s underutilized infrastructure. The 90-day termination clause on the Colossus 1 lease is the explicit market price of the SPOF.

Dario Amodei defined the constraint he faced in the Dwarkesh podcast appearance the week of the Series G announcement in February 2026: “If our revenue comes in at $800 billion instead of $1 trillion, there’s no force on Earth, there’s no hedge on Earth, that could stop me from going bankrupt.”

Dario warned about the inverse risk of overcommitment, where compute spend outruns the revenue that funds it. But Anthropic’s binding constraint in 2026 turned out to be a symmetric failure: undersupply, with growth outpacing the company’s owned and contracted capacity.

That SPOF quickly went from hypothetical to a real price tag: $1.25 billion every month to xAI to secure the extra compute needed for the next three years. Suddenly, a huge chunk of revenue was flowing to a company that, at least in theory, had been a frontier-model competitor.

Act III - August 2025 through early 2026: The coding wedge holds

But let’s return now to the chronology of Anthropic’s rise. In August 2025, I published The 11% Paradox, introducing a concept that I dubbed “Coding Wedge.” The argument was contrarian to the dominant venture-capital framing of AI coding tools as a category bounded by Cursor, Replit, Cognition’s Devin, and GitHub Copilot, which defined a $20 to $60 billion total addressable market, depending on whether the analyst sized current product revenue or forward enterprise-developer spend.

My claim was that coding tools owned by labs were not products in that category. They were infrastructure for the labs that owned them, and the durable winners would be lab-integrated rather than category-bound.

The architectural reasoning was specific. Code is the unique medium through which agentic systems can be observed both producing and verifying output. A compiler enforces syntax; tests enforce behavior; version control enforces history. The trust geometry that agents need to operate in any high-stakes domain is reproducible at scale in coding before it is reproducible anywhere else. Whoever owns coding owns the dataset for trust calibration that the rest of the Harness will require.

The wedge thesis carries an implicit assumption. The trust calibration developed in coding does not transfer instantaneously into adjacent knowledge work. Corporate law, strategic sales, financial forecasting, and most of the categories Anthropic has named as targets for Cowork lack a deterministic compiler. There is no test suite that returns green when a legal opinion is correct. There is no version control that reconciles two divergent forecasts. The trust geometry in these domains must be constructed from softer signals, such as citation verification, audit-trail reconstruction, and human review, at structured intervals. And the calibration curve is correspondingly longer.

The coding wedge gives the lab cohort a head start on the architecture of trust at scale. It does not guarantee the architecture transfers cleanly into messy, non-deterministic environments. The Cowork legal and finance plugins are the first market test of how cleanly the transfer occurs.

My August 19 follow-up article, GPT-5’s Mixed Debut: How the Coding Wedge is Reshaping AI’s Orchestration Battle, extended the thesis. OpenAI’s heavy emphasis on coding and agentic capabilities at the GPT-5 launch validated the wedge mechanic at the second-largest frontier lab. If two labs pursued the same wedge simultaneously, the question of the moat would resolve at the orchestration layer above the wedge, rather than at the model layer below.

The Anthropic Series G announcement on February 12, 2026, aligned with the mechanics of the wedge thesis. Claude Code at a $2.5 billion run-rate. Anthropic’s framing in the announcement was, almost verbatim, the wedge argument: “The same capabilities that make Claude exceptional for coding are also unlocking other new categories of work: financial and data analysis, sales, cybersecurity, scientific discovery, and beyond.”

Coding was not a vertical. It was the entry to the Harness.

The pace of enterprise adoption exceeded what I had modeled in August 2025. I had estimated a Claude Code run-rate of approximately $1.5 billion by the end of 2026. The actual February 2026 disclosure was $2.5 billion, eight months early. I had assumed enterprise procurement cycles would compress agentic adoption to the cadence of prior SaaS deployments. They did not.

The cycle for agentic tools was resolved within a single sprint rather than within a multi-quarter pilot. Enterprise sales cycles compress under agentic adoption. The revenue trajectories of orchestration-layer winners may be steeper than any prior reference cycle suggests.

Act IV - January 2026: Cowork and the software mispricing

In January 2026, Anthropic launched Cowork. The product extended Claude Code’s engineering capabilities into broader knowledge work, including financial analysis, legal review, sales operations, and scientific research. Vertical plugins for legal and finance were shipped on January 30, 2026.

The market reaction was immediate and undifferentiated. Between January 15 and February 14, 2026, approximately $2 trillion in software market value evaporated. Bloomberg on February 3 quoted Jeffrey Favuzza of Jefferies, coining the term that would define the period: “SaaSpocalypse.” Salesforce traded down 28% from its January high. ServiceNow lost 27% by mid-February. Workday lost 33%. Jefferies estimated $285 billion in software cap evaporation over 48 hours.

Claude Cowork and the Enterprise Software Sorting, published on January 20, 2026, was my pre-event reading of what was about to happen. I argued the market would mistake the SaaS-wide repricing for undifferentiated AI disruption. The sorting would, in fact, be specific. Workflow wrappers and thin AI applications would face genuine commoditization because they sat on no irreplaceable data and provided no irreplaceable workflow context.

Systems of Record, such as Salesforce, ServiceNow, and Workday, would face the opposite condition. Their accumulated operational data, deep integration into customer business processes, and decision-making authority over execution were precisely the things Cowork plugins could not replicate without years of integration work per customer. In fact, in my earlier work, and notably in The Salesforce Paradox, published in July 2025, I had argued that the slowing top-line growth of the SoR cohort was masking a $1 trillion agentic opportunity at exactly the layer Cowork would later contest.

I developed the sort across February 2026 in the SaaSpocalypse trilogy: The $285 Billion ‘SaaSpocalypse’ Is the Wrong Panic, Decoding Anthropic’s $380 Billion Valuation, and Figma’s Orchestration Play. The sorting argument had a corollary: the priced reaction had not yet been reflected. The labs were moving up the stack toward orchestrating enterprise work. The systems of record were positioned to move down the stack toward what I called “systems of action”: orchestration platforms that coordinate agents through their existing context monopoly. The competition would be resolved at the orchestration layer.

The Cowork launch and the SaaSpocalypse repricing together opened the question I had not yet answered in public: how, exactly, the labs and the systems of record would coordinate, and what that coordination would look like once the architecture stopped being a thesis and became a shipped product.

The earnings season has begun to vindicate the sorting at the fundamentals layer. Workday’s May 21 Q1 FY27 print - revenue +13.5%, operating margin expanding from 1.8% to 13.3%, the best new-ACV Q1 in five years, management attributing the acceleration explicitly to agentic AI adoption, sent the stock up 3.7%. ServiceNow’s April 22 print beat every metric and showed Now Assist ACV tracking to $1.5 billion versus a $1 billion prior target with $1M+ customers up 130% YoY (the same-day 17% stock drop reflected the $7.75 billion Armis acquisition close and a Middle East subscription delay) in a prevailing context of “SaaSpocalypse.” Salesforce reports Q1 FY27 on May 27. This will be the third and most consequential test of whether the SoR cohort is the ground onto which agentic work actually deploys.

Act V - Spring 2026: Claiming the throne

Three events between March 31 and May 20, 2026, transformed the orchestration thesis from a priced narrative into a priced reality. Together, they marked the coronation.

On March 31, 2026, approximately 512,000 lines of Claude Code source code became inadvertently public, a significant operational security failure at Anthropic, a privileged repository that slipped its access controls. The leaked source revealed that Claude Code’s architecture was substantially more general than its product positioning suggested: a domain-agnostic orchestration harness explicitly named in internal comments, self-rewriting memory accumulating across sessions, an unshipped autonomous daemon, and multi-agent delegation patterns behind feature flags. I read the codebase as the engineering specification for the architecture I had described as the Harness. In Early April, I analyzed that code in Anthropic Claude Code Leak: Decoding Its Blueprint for the Orchestration Graph.”

On May 19, 2026, Anthropic launched Managed Agents with self-hosted sandboxes (public beta) and MCP tunnels (research preview). The architecture revealed in the leaked code is now shipped as a product. Anthropic retained the brain in the form of the agent loop, the orchestration logic, and the model. The customer retained the body: the sandbox, the data, and the security perimeter. MCP was the protocol through which the whole arrangement was coordinated. The launch named four execution-layer partners, notably distinct from the hyperscalers: Cloudflare, Daytona, Modal, and Vercel. Each provided a different runtime profile: Cloudflare microVM isolation, Daytona stateful composable computers, Modal AI-native sandbox primitives, and Vercel VPC-peered credential management.

The architectural significance here is the question of where agents physically execute. Managed Agents is the deployment mechanism that makes MCP reach into customer perimeters. It is the apparatus that operationalizes Anthropic’s claim on the orchestrator role at enterprise scale - the brain (the agent loop and orchestration logic) held by Anthropic, the body (the sandbox, the data, the security perimeter) held by the customer, and MCP as the connective tissue. The choice of non-hyperscaler execution partners is the deliberate preservation of Anthropic’s independence from AWS, Azure, and Google Cloud, each of which is simultaneously a major commercial partner and a structural competitor at the agent-runtime layer.

However, as I warned when writing about Managed Agents, Anthropic had increased the risk of falling victim to its own success. Easier agent deployment meant usage could explode beyond already-constrained compute. From early March 2026 through April, Anthropic was visibly running ahead of its capacity, which led to persistent rate limits, recurring outages, defects in reasoning-effort defaults and caching, and the April 6-7 outage. The Ramp May 2026 advisory named “frequent outages, rate limits, and increasing dissatisfaction with results“ as the principal risk to Anthropic’s enterprise lead. Anthropic reset user-facing rate limits and posted an engineering postmortem on April 23; user dissatisfaction had crystallized into a sustained public chorus by then.

Anthropic responded with a flurry of compute deals over the next 30 days. AWS on April 20 ($25 billion equity, 5 GW Trainium), Google on April 24 ($40 billion equity, 5 GW TPU arriving 2027), and the xAI Colossus 1 lease disclosed May 20 as the bridge between today’s capacity wall and the 2027 TPU arrival. Three of the world’s four largest infrastructure operators committed compute resources to Anthropic within 30 days.

The Series G, framed as growth capital, was substantially compute financing.

The compute bottleneck had been solved. For now. Rate limits were increased. The throne is held. For now.

Act VI - How Anthropic defends the throne

As of today, Anthropic has established itself as a leading model provider for enterprise workloads and, thanks to its harness capabilities, as what we will refer to as the “technical” orchestrator: the intelligence and nervous systems that sit at the core of enterprise workflows. But that position is different from being a true orchestrator, as I defined in the Manifesto I recently released.

The architectural bet: Anthropic as Orchestrator

The architectural moat is not a configuration of the enterprise stack. It is a role - the orchestrator role - and the configurations of the enterprise stack are downstream consequences of who occupies that role.

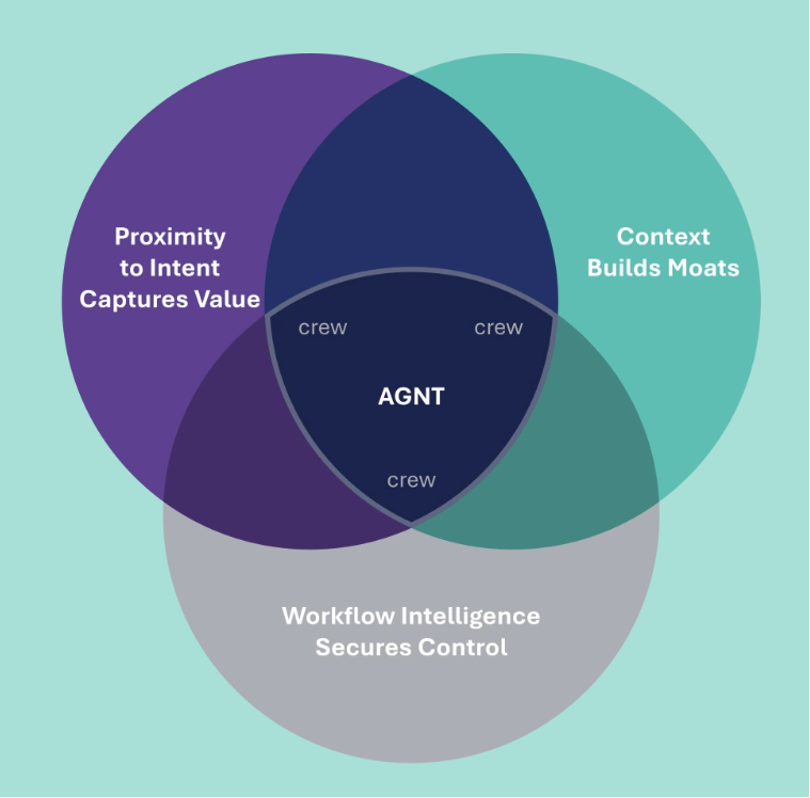

I defined the concept of the orchestrator in The Orchestration Economics Manifesto through three Laws of Value in the agentic era. The orchestrator is the entity that sits at the center of the agentic enterprise IT stack: it captures user intent at the surface where work begins, it accumulates the cross-session and cross-system context that compounds with usage, and it codifies the workflows that span across the systems of record the enterprise already runs. Each Law names a dimension along which the orchestrator role is defended. Each is a moat in its own right. Together, they describe a position that no individual model release, no individual product launch, and no individual hyperscaler arrangement can independently produce.

Holding the throne rests on Anthropic’s ability to win the orchestrator role along all three dimensions simultaneously.

The First Law applied - proximity to user intent. Whoever captures user intent captures power. Anthropic captures intent through three primary surfaces, each engineered to be a destination rather than a feature: Cowork as the broad knowledge-work destination, Claude Code as the developer destination, and Claude.ai as the consumer destination. Cowork is the most consequential of the three, because it is the surface that competes most directly for the cross-vertical enterprise door. Anthropic disclosed at the Series G that Cowork usage was outpacing internal projections, with the vast majority of usage coming from outside engineering teams. The Cowork “co-worker” mode launched in 2026 explicitly positions Claude as the surface where the day starts. The architectural intent is clear: Anthropic does not want to be a model that other surfaces call upon. It wants to be the surface that calls upon other models.

The Second Law applied - context depth from being the orchestrator. The orchestrator that routes intent across systems accumulates context that no individual system can replicate. The systems of record hold deep domain context and are called upon by the orchestrator when the relevant domain is addressed. The orchestrator holds the meta-context: the routing memory, the cross-system relationships, the patterns of how enterprise work actually moves across SoR boundaries. The leaked Claude Code source revealed exactly this object: a self-rewriting memory system that accumulates operational understanding across sessions and persists structured context between unrelated conversations. MCP is the protocol that enables the orchestration graph to access any SoR endpoint as a callable resource. Managed Agents is the deployment apparatus that makes the graph operable inside customer perimeters. The Second Law moat is the meta-context that compounds with every routed intent.

The orchestrator that learns and codifies enterprise workflows produces a moat that compounds independently of any single SoR and independent of any single model. Multi-agent delegation revealed in the leaked source, the agent loops that span across MCP endpoints, the sandboxed execution patterns now shipped through Managed Agents, these encode the workflow. Once an enterprise has standardized its agentic workflows against Cowork and the orchestration graph, switching costs are real even when the model layer is theoretically swappable. The Advisor strategy preserves multi-model flexibility at the inference layer: Claude Opus orchestrates, Sonnet and Haiku execute, and in principle, non-Anthropic models can be routed to for specific tasks. But the workflow encoding itself does not move. The customer can change which model serves a task. The customer cannot easily change the orchestrator without rebuilding the workflow scaffolding.

These three Laws together are the moat. They do not require Anthropic to win the model layer outright. They require Anthropic to be the orchestrator that the enterprise has chosen to organize its agentic work around. The $900 billion valuation prices Anthropic as the lab most likely to win that role. Whether the role is won decisively, or shared, or lost is the work of the next eighteen months and the substance of the four challenger threats addressed below.

Challenger 1 - OpenAI

OpenAI is competing for the orchestrator role from a different starting position than Anthropic. The First Law advantage is consumer scale: ChatGPT at 900 million weekly active users is the largest single AI surface in existence, and the surface where consumer intent already originates. Codex, at 2 million weekly users, up roughly 5x in three months, is the developer destination OpenAI is building as the entry to the enterprise stack. This is the same wedge mechanic Anthropic is running with Claude Code, executed from a different starting position. Andrej Karpathy, who would later join Anthropic in May 2026, acknowledged the “duopoly” publicly before his move in a tweet:

“Where does this leave us? LLM agent capabilities (Claude & Codex especially) have crossed some kind of threshold of coherence around December 2025 and caused a phase shift in software engineering and closely related. The intelligence part suddenly feels quite a bit ahead of all the rest of it - integrations (tools, knowledge), the necessity for new organizational workflows, processes, diffusion more generally. 2026 is going to be a high-energy year as the industry metabolizes the new capability.”

The Second Law play is operationalized through ChatGPT Enterprise, ChatGPT Atlas browser, and Operator (the browsing agent), each of which is engineered to accumulate enterprise-specific context as the surface is used. The Third Law play is the agentic workflow apparatus inside ChatGPT, including Apps, Tasks, and Codex extensions, encoded against OpenAI’s runtime.

The distribution channel is Microsoft. ChatGPT Enterprise is sold through Azure, Codex is integrated into Visual Studio Code and GitHub, and Microsoft 365 Copilot increasingly routes inference to OpenAI as the default lab. The path requires consumer scale to translate into enterprise distribution faster than Anthropic’s enterprise position generalizes outward toward consumers. The path is plausible; the question is execution velocity, which the eventual S-1 disclosures will materially clarify.

Challenger 2 - Google

Google’s challenge is the most structurally complete because Google holds existing assets along all three Laws simultaneously. The First Law advantage is three billion Workspace users - the largest installed productivity surface in existence and, in many enterprises, already the door where the day begins for documents, email, and calendar. The May 2026 Google I/O announcements were the inflection point at which Google’s distribution moats began converting into agentic execution at scale: Search Live, AI Mode commerce, Agent Mode, Try It On, Personal Context, and the Gemini integration across Workspace together represent the largest single agentic product launch any lab has shipped to date, measured by installed-user surface, feature breadth, and rollout speed.

The Second Law play is the document, search, and productivity context already accumulated in Workspace and queried at scale through Gemini and Vertex. The Third Law play is the parallel coordination standards Google has shipped: A2A and the Agent Payments Protocol, and the Vertex AI Agent Builder as the runtime against which Google ecosystem workflows are encoded. Gemini 3.1 Pro performs within striking distance of Claude Opus 4.7 on the metrics that matter for enterprise deployment. The structural question is whether A2A bifurcates the protocol layer (MCP-dominant outside Google, A2A-dominant inside) or displaces MCP entirely (A2A as the new default coordination standard). My base case is bifurcation, which is consistent with Anthropic continuing to win the cross-vertical orchestrator role in the majority of the cohort. Displacement would invalidate that case. Google has the distribution to attempt it. Whether it has the enterprise sales motion velocity to displace MCP within 18 months remains an open question.

Challenger 3 - xAI plus Cursor

The xAI-plus-Cursor configuration is the only visible challenge that operates outside the lab cohort’s three-way race. The First Law play is Cursor’s captured developer destination: the IDE integration, the CLI, and the agent orchestration running locally on developer machines. This is increasingly where professional developers initiate intent for any agentic work, not only coding. The Second Law play is the codebase context that Cursor accumulates within the developer’s workflow; this context is narrow but deep, confined to code yet exceptional within that domain. The Third Law play is the workflow encoding within Cursor’s IDE and agent patterns, which captures coding-specific workflows without requiring routing through Anthropic.

The compute side is xAI’s. Cursor was named as a Colossus tenant alongside Anthropic in the SpaceX prospectus, which means compute access is not the binding constraint. The model side is Composer, launched in November 2025 specifically to escape the Claude tax that had compressed Cursor’s gross margin to approximately −23% in January 2026, before Composer’s deployment and cheaper-model routing pushed the metric back to slight positive territory by April. The April 2026 publication of Cursor’s warp-decode kernel work, extracting 58% of B200’s peak memory bandwidth on the decode regime that bounds agentic inference, demonstrated engineering depth at the frontier of model deployment economics. We will deep-dive into xAI x Cursor’s play in next week’s SpaceX S-1 teardown.

The wildcard question is whether Cursor’s CLI generalizes beyond coding. If the CLI becomes the way professional knowledge workers initiate intent for agentic work in adjacent domains such as technical product management, financial modeling, quantitative research, and data engineering, then the configuration reconstitutes a complete agentic stack entirely outside the lab cohort. The pattern, if proven, replicates. The configuration does not need to win the lab race. It needs to capture intent at a single non-coding surface convincingly enough to demonstrate that orchestrator positions can be reconstituted from outside the established cohort.

Challenger 4 - The systems of record

The systems of record are not passive endpoints called upon by the lab orchestrators. They are actively building their own front doors and competing for the orchestrator role inside their verticals.

Take the case of Salesforce. The First Law plays a role in Slack’s existing position as the surface where teamwork happens, particularly inside companies that have built their operational culture around it. The Second Law plays in Salesforce’s accumulated revenue context, made addressable through Slack’s interface, and extended in the context of the Informatica acquisition. The Third Law play is Salesforce’s encoding of how the business actually runs, including opportunity stages, approval chains, deal-desk logic, validation rules, and discount authority for a CRM workflow, and operating as the verification ground truth that every agent in the workflow, including a lab-built one, has to reference to be operationally correct.

The same logic applies across the SoR cohort. ServiceNow is building Now Assist and its broader platform as the IT operations orchestrator, with customer-specific ITIL adaptations and CMDB structures as the irreplaceable context layer. Workday is building Workday Agent System as the workforce orchestrator, with job architecture and compensation framework as the context substrate. Atlassian is integrating Rovo across Jira and Confluence as the engineering-management orchestrator. Each is a vertical orchestrator-in-the-making - and each is monetizing the role through consumption pricing rather than per-seat licensing, precisely because the per-conversation economics capture the value of the orchestrator position.

This is the most important architectural point about the SoR challenge: they are vertical orchestrators competing against the cross-vertical orchestrator (Anthropic) for the right to define how agentic work flows within the verticals where they have accumulated decades of business logic. The competition is real, and the SoRs are actively building. Anthropic’s defense in the verticals where SoR context is irreplaceable is not to win the door - it is to remain the lab the SoR calls upon for inference even after the SoR has won the surface.

The downstream consequence

In categories where Anthropic wins the orchestrator role, the stack arranges itself as Configuration A: Cowork as the door, SoRs as MCP endpoints, agents in the Cloudflare-Daytona-Modal-Vercel execution layer, with Anthropic capturing intent, orchestration, and inference economics. In categories where an SoR wins the orchestrator role within its vertical, the stack arranges itself as Configuration B: the SoR as the door, Anthropic as the brain, and the shared nervous system underneath, with the lab capturing inference economics only. The base case is that the two configurations coexist by vertical: Configuration A in the cross-vertical knowledge-work surface, Configuration B in the verticals where the SoR context is irreplaceable. The architecture is the consequence.

The financial bet: growth endurance

The compute commitments Anthropic has signed are not, on a standalone basis, payable from the current revenue base. Approximately $400 billion of Anthropic compute commitments across disclosed term lengths (AWS, Google, Azure, Fluidstack, NVIDIA, xAI) plus the energy and dedicated-capacity arrangements still to come. These commitments are largely fixed in nominal terms - signed in advance against projected demand, locked into multi-year arrangements. They do not scale with revenue. The $1.25 billion monthly outflow, at approximately $15 billion annualized, is running against $30 billion in annualized run-rate revenue today.

The financial bet at the heart of the throne-holding story is “growth endurance,” the ability to hold the growth rate year on year. I view this as one of the most important metrics when assessing a high-growth company. The compute base does not move; the only way to drop unit cost is to grow the revenue base faster than the commitments compound. This is the analytical heart of the bull case at $900 billion. The mark is not pricing Anthropic as a present-margin company. It is pricing Anthropic as a company that converts the present compute strain into future margin through endurance - growth holding long enough for amortization to complete.

And this is even more acute, as Anthropic’s Q2 profitability also stems from capacity ramping in Q2 2026, per an agreement with xAI, rendering the cost of compute over the period non-normative.

The IT budget equilibrium is the binding constraint on growth endurance, and it is what makes the bet a bet against time. Claude's revenue today appears unconstrained by the IT envelope because it is being financed by a one-time displacement of incumbent software licenses, rather than by a stable allocation against that envelope. The Information recently reported that enterprises are actively clawing back budget from traditional software vendors to fund the AI line; SaaStr’s read is that as much as 70% of the current enterprise software slowdown is budget rotating toward Anthropic and OpenAI. The displacement pool is large but finite. Once it is drawn down, growth has to come from real envelope expansion - the slower, capex-cycle-bound side of the equilibrium - and that is the boundary the bet is racing.

Microsoft’s May 2026 internal Claude Code cancellation, per The Verge, affecting thousands of licenses across the Experiences + Devices group with a June 30, 2026, cutoff, officially attributed to “toolchain unification” but timed to Microsoft’s fiscal-year boundary, is the early signal of a major enterprise capping AI-lab exposure against a broader IT envelope. Every other Fortune 500 IT organization is six to eighteen months behind Microsoft in the recalibration process. When the cohort completes it, and it will, because IT budgets do not grow exponentially, and because humans are not just thrown away like that to be replaced by compute, growth normalizes from the displacement-driven trajectory toward an equilibrium curve with a quantum to be determined in the next months.

For the P&L to hold, the absorption of training and inference compute has to hold. For now, it is the case.

The operational bet: no SPOF binds

The third condition is that none of the three single points of failure that we detail below binds hard enough to break the architecture during the window in which the amortization completes. The three SPOFs are the substance of Act VII.

If Anthropic wins the orchestrator role, adoption-driven amortization works, and none of the three SPOFs bind, Anthropic holds the throne and stays on it, and the $900 billion mark is reached by mid-2027. If any one of the three conditions fails, the lead becomes contestable in ways the present valuation does not price.

Act VII - What overthrows the king

Anthropic faces three potential Single Points of Failure that could topple the company:

Risk 1 - Compute

The Colossus 1 lease is tactical. It addresses demand for Q2 to Q4 2026 with a 90-day termination clause. It does not address the structural problem: Anthropic’s growth trajectory implies a compute demand curve that no third-party arrangement can meet through 2027 and beyond. Per the S-1:

“We have the ability to use compute resources to support our proprietary AI applications (such as Grok 5, which is currently being trained at COLOSSUS II), while also providing access to select compute capacity to third-party customers. For example, in May 2026, we entered into Cloud Services Agreements with Anthropic PBC (“Anthropic”), an AI research and development public benefit corporation, with respect to access to compute capacity across COLOSSUS and COLOSSUS II. Pursuant to these agreements, the customer has agreed to pay us $1.25 billion per month through May 2029, with capacity ramping in May and June 2026 at a reduced fee. The agreements may be terminated by either party upon 90 days’ notice.”

Three pathways are visible for the structural solve beyond the current arrangement.

First, anchor hyperscaler lock-in by deepening existing AWS and Google commitments into multi-year capacity arrangements totaling hundreds of billions of dollars cumulatively; Anthropic’s disclosed compute commitments are already approaching $200 billion in contracted value.

Second, vertical integration into silicon is capital-intensive, with a minimum lead time of 3 years and technically risky given a fast-moving model cycle.

Third, joint ventures with power developers at a gigawatt scale, following the November 2025 Fluidstack template ($50 billion, Texas and New York). Anthropic’s inclusion in the Genesis Mission executive order on advanced nuclear fission suggests this pathway is being developed in parallel.

My base case for the twelve-month resolution is a combination of the first and third pathways, with the second preserved as a multi-year option. Within four quarters, I expect Anthropic to announce either a multi-year dedicated capacity arrangement greater than $50 billion in committed value, a gigawatt-scale joint venture with a power developer, or both. If neither materializes, the compute SPOF is structurally tighter than I currently believe, and the amortization math becomes harder.

The risk for the throne is not that Anthropic runs out of compute. The risk is that the compute it secures comes with strings that constrain the architecture: deeper hyperscaler dependence that compromises the Managed Agents’ independence, or higher inference cost pass-through that erodes the door’s economics. The compute SPOF binds operationally if any of these strings tighten faster than adoption amortizes them.

Risk 2 - The user interface

The four challenger threats developed in Act VI all express, at different scopes, the same underlying interface risk: the orchestrator role is held by whoever captures intent, and intent originates at the surface the enterprise user already inhabits. The interface SPOF is the risk that Anthropic loses the First Law contest, that Cowork does not become the surface where the enterprise day begins, that intent is captured instead at ChatGPT, at Workspace, at Cursor’s CLI, at Slack, at GitHub Copilot, at Microsoft 365 Copilot, or at any of the SoR-owned destinations now actively building their own front doors. Once the door is lost at scale, the meta-context and the workflow encoding compound around someone else’s surface and cannot be reclaimed.

Risk 3 - The frontier

The thesis treats orchestration as the durable moat and the model layer as commoditized to the point of competitive irrelevance. The strongest argument against the thesis is that the model layer is not commoditized, that being the captain of the agentic chain requires being the smartest brain in the chain, and that a meaningful Claude-versus-GPT-versus-Gemini gap in the wrong direction would unwind the orchestration position regardless of architectural depth.

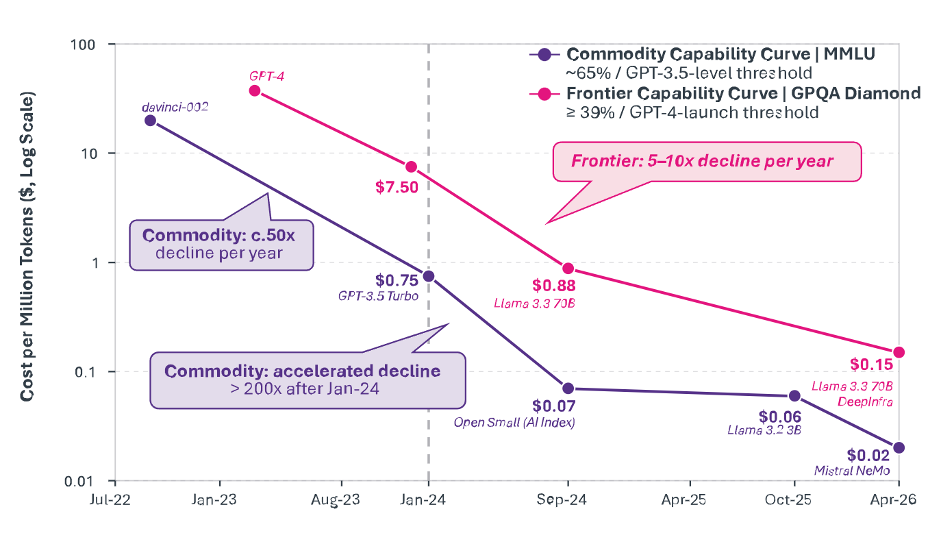

The data on this question is mixed. Per Epoch AI, frontier capability cost has been declining at approximately 5 to 10x per year across the GPQA-Diamond benchmark since GPT-4 launch. Commodity capability cost - the price of GPT-3.5-equivalent intelligence - has declined at 50 to 200x per year, with the divergence accelerating since January 2024. The empirical pattern is two curves: frontier capability is slowly commoditizing, while everything below the frontier is commoditizing rapidly.

The thesis depends on Anthropic remaining at or near the frontier. If Anthropic falls one model generation behind Google or OpenAI on the next frontier release - Claude 5 versus GPT-6 versus Gemini 4 - the orchestration position may not survive enterprise procurement decisions that route inference to whichever frontier model wins the benchmark cycle.

The defense runs in two parts. First, the orchestration architecture I described in Act V - domain-agnostic harness, self-rewriting memory, multi-agent delegation, Managed Agents deployment - compounds independently of marginal model quality. An enterprise that has standardized on Cowork against its accumulated context does not switch to a six-percentage-point GPQA-better competitor without a substantially larger capability gap than the cycle has historically produced.

Second, the Karpathy hire on May 19, 2026, is the recursive-research bet. His mandate, per Nick Joseph, is to build a team focused on using Claude to accelerate Claude’s pre-training research itself. The bet operationalizes Jack Clark’s May 4, 2026, Import AI thesis that recursive self-improvement carries roughly a 60% probability of occurring by the end of 2028. If the bet pays, if “use Claude to accelerate Claude’s pre-training research” produces measurable capability uplift through 2026 and 2027, Anthropic does not need to win every benchmark cycle. It needs to consistently remain at the frontier, while orchestration compounds the lock-in.

The threshold at which the frontier SPOF binds: if any of GPT-6, Gemini 4, or a third frontier release between now and the end of 2027 opens a sustained six-month capability gap over Claude on enterprise-relevant benchmarks, the throne becomes contestable. I read the probability of this as moderate, but not high

One operational tightening here is worth naming explicitly. Orchestration adoption is downstream of inference adoption. Anthropic’s enterprise foothold in agent orchestration is built on customers who first chose Claude for inference and subsequently migrated from third-party frameworks to Anthropic’s native tooling—Cowork, Managed Agents, and the orchestration graph. If the model-layer lead erodes and customers begin routing inference to a frontier-better competitor, the orchestration relationship unwinds faster than a standalone SPOF analysis would suggest. The model lead is not parallel to the orchestration lead. It is the foundation. The frontier risk is therefore operationally tighter than it appears in isolation.

What this means

Anthropic was once treated as a pretender to the throne. The orchestration moat has been validated. The architecture is in multiple shipped product forms. The protocol is the de facto coordination standard. The enterprise revenue mix is dominant. The first profitable quarter is imminent. The valuation prices the lead. By nearly every public measure, the throne has already been claimed.

The trillion-dollar question is whether Anthropic can stay on the throne. Three conditions must hold simultaneously: it must own orchestration at the center of the enterprise agent stack, scale fast enough for adoption to amortize infrastructure before growth normalizes, and avoid losing any of the three critical bottlenecks - compute, interface, or frontier capability - before the cycle completes.

The story of the next eighteen months is whether all three continue to hold simultaneously against the three-lab competition for the orchestrator role that Act VI named: OpenAI’s consumer-to-enterprise translation through ChatGPT and Codex, Google’s Workspace-Vertex-Gemini distribution play following the May 2026 I/O announcements, and the xAI-Cursor wildcard from outside the lab cohort.

One final risk worth naming plainly: Anthropic has traded its scrappy underdog position for frontrunner status. That has brought ever more intense public scrutiny and criticism. But for the first time in this cycle, Anthropic’s narrative may be running ahead of its valuation rather than behind it.

From May 2025 through Q1 2026, every announcement, every disclosure, every shipped product confirmed the thesis at a pace that exceeded the framework's projections. The valuation chased the execution. The Series E at $61.5 billion, the Series F at $183 billion, and the Series G at $380 billion each priced what had already been built and ratified what was about to be built.

The $900 billion mark is different. It prices a level of dominance that is partially earned and partially aspirational. Winning the orchestrator role is what Anthropic is building, not what it has already won. The mark is defensible. It is not generous. The orchestration moat is real. The king is on the throne. But the conquest is not complete.

The next eighteen months will produce evidence on whether the throne holds, or whether, for the first time in this cycle, the priced narrative has overrun what the execution can deliver. That is the trillion-dollar question.

The framework continues at orchestration-economics.com.

The views and opinions expressed in this Website are those of the author alone and are based on publicly available information. The expressed views and opinions do not constitute investment advice, a solicitation, or a recommendation to buy or sell any security or financial instrument.

The author may hold positions in the securities of companies mentioned. Certain companies referenced may be current or former clients of, or counterparties to, the author or affiliated entities; such relationships will be disclosed where applicable.

Past performance is not indicative of future results. To the fullest extent permitted by applicable law, the author does not accept any liability for any loss or damage arising from reliance on this content. Readers should conduct their own independent due diligence and consult a qualified financial advisor before making any investment decision.

The author maintains no current position in Anthropic, SpaceX, or any private entity discussed.